The End of the $25,000 Day-Trading Rule Could Reshape Retail's Role in the Stock Market

For more than two decades, one rule quietly separated smaller retail traders from the kind of active trading access available to larger accounts.

That barrier is now coming down.

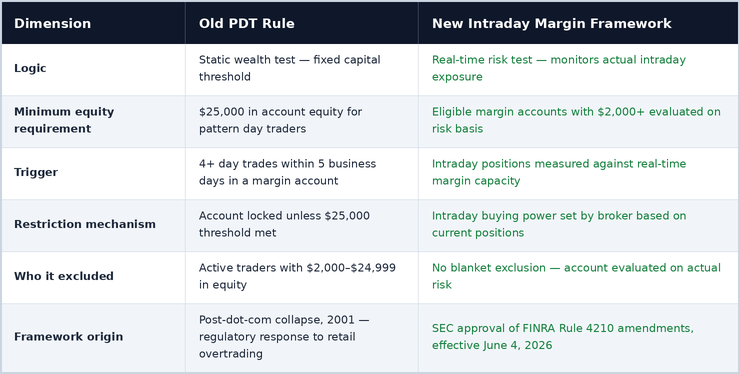

The SEC's approval of FINRA's new intraday margin framework will eliminate the old Pattern Day Trader rule, including the long-standing requirement that frequent day traders maintain at least $25,000 in account equity. In its place, brokerage firms will move toward a risk-based system that monitors intraday exposure, margin requirements, and account deficits in real time.

The change may sound technical. It is not.

It marks another step in the long-running transformation of U.S. equity markets from a broker-controlled system into a faster, cheaper, more open, and increasingly data-driven marketplace shaped by retail investors, brokerage platforms, market makers, algorithmic trading desks, and quantitative funds. And it arrives at exactly the moment the market is becoming more mobile, more options-driven, more ETF-driven, more algorithmic, and increasingly prepared for tokenized securities and 24-hour trading.

From Static Wealth Test to Real-Time Risk Test

The old PDT rule was created after the dot-com collapse, when regulators were concerned that inexperienced traders were taking excessive risks in volatile internet stocks. Under that framework, investors who made four or more day trades within five business days in a margin account could be designated Pattern Day Traders and required to keep at least $25,000 in equity. An investor with $10,000 or $15,000 could trade, but only within tight limits. Cross the line too often, and the account could be restricted.

The new framework changes the logic entirely.

Charles Schwab has explained that under the new rules, eligible margin accounts with more than $2,000 may gain access to intraday margin buying power set by individual brokerages based on current positions and maintenance margin requirements. The framework goes live June 4, 2026, with a phase-in period ending October 20, 2027.

Retail Is No Longer a Sideshow

The rule change arrives after one of the largest expansions of individual-investor participation in modern financial history.

During the 2020 and 2021 trading boom, U.S. brokerage platforms added tens of millions of new accounts across Robinhood, Webull, Fidelity, Charles Schwab, TD Ameritrade, E*TRADE, Interactive Brokers, SoFi Invest, Public.com, M1 Finance, Merrill Edge, Vanguard, and other online platforms. Estimates of new U.S. retail brokerage accounts during the pandemic-era boom range from roughly 30 million to nearly 40 million. More important than the precise number is the scale: a new generation of investors entered the market through mobile-first, low-cost, app-based infrastructure.

Those investors did not disappear. Reuters, citing J.P. Morgan data, reported that retail trading accounted for roughly 20% to 25% of total U.S. equity market activity in 2025 and reached a peak near 35% in April 2025. That is not a rounding error. It is a permanent market-structure force.

Retail investors now influence single stocks, ETFs, options activity, high-beta technology shares, small caps, and crypto-linked equities. Their flows are watched by brokers, market makers, hedge funds, exchanges, and public companies because retail has become one of the market's most important marginal participants.

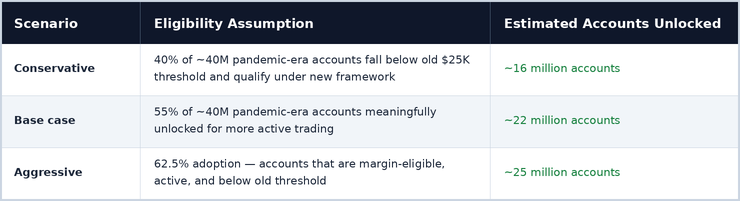

The 40 Million Account Math

The most important quantitative point is the potential unlocked account base.

Not every account will qualify. Not every investor will apply for margin. Not every user wants to day trade. Some accounts are too small, some are cash accounts, some are inactive. But that is not the central point. The central point is that millions of accounts below the old $25,000 threshold may now be evaluated based on actual account risk rather than excluded by a fixed capital requirement. The active-trading addressable market could expand by tens of millions of accounts.

The Long Arc of Market Democratization

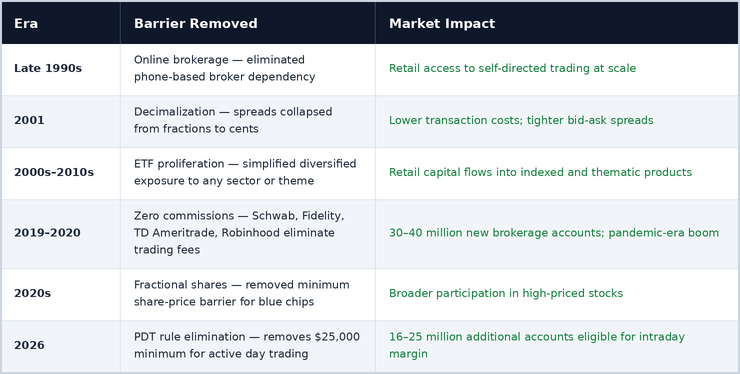

The elimination of the PDT rule does not stand alone. It is the latest step in a multi-decade sequence of barrier removals, each of which expanded participation and, eventually, reshaped market structure.

The pattern in each case was the same: a friction point was removed, access expanded, volume followed, and the market eventually repriced to reflect a larger and more active participant base. The PDT rule change follows the same logic, targeting the exact cohort that has already demonstrated high engagement — smaller, app-based, mobile-first, self-directed retail traders.

The Quant Layer: Wall Street May Already Be Repricing

A second, less-discussed consequence may be even more important than the access expansion itself: the rule change becomes a new variable inside Wall Street's trading models.

Modern trading desks and quantitative funds do not wait for a theme to become obvious before adjusting their systems. They track liquidity, volume, retail order flow, options demand, ETF flows, intraday volatility, social sentiment, broker activity, margin usage, and market microstructure signals. When a regulation changes the potential behavior of millions of accounts, that becomes a model input.

It would be naive to assume proprietary trading desks and quant funds are waiting for the rule to take effect before adapting. The more sophisticated firms are likely already tweaking algorithms, stress tests, liquidity models, and retail-flow assumptions to account for a larger pool of active accounts below the former $25,000 threshold. They can anticipate which symbols, sectors, ETFs, and options chains may see higher intraday participation once brokers implement the new framework. They can adjust market-making models, reposition around expected flow, and build strategies around a market where small-account activity is less constrained.

Once a rule change becomes embedded in trading models, it does not merely change investor access. It changes how professional liquidity providers, market makers, and quant funds position around that access. That is when the feedback loop begins.

The Macro Tailwind Behind the Access Event

The PDT rule change does not arrive in isolation. It arrives at a moment when U.S. monetary conditions are the most constructive for equity appreciation since 1927, which we highlighter here. This includes M2 at all-time highs, a money multiplier expanding at its fastest pace in fifteen years, AI-driven productivity absorbing monetary expansion as real output rather than consumer inflation, and an estimated $45 trillion in foreign capital being disintermediated out of Japanese, European, and Chinese banking systems toward U.S. dollar assets via stablecoin rails codified by the GENIUS Act.

When 16 to 25 million newly active retail accounts enter a market with that macro backdrop simultaneously, the feedback loop between access and performance could be more powerful than either factor would produce alone. Lower barriers. More liquidity. Into one of the most constructive monetary setups in a generation.

The timing is not coincidental. It is the kind of structural convergence that rewrites valuation cycles.

ETFs and Options Magnify the Impact

The rule change is more powerful today than it would have been a generation ago because ETFs and options have become massive transmission mechanisms for retail capital.

Retail investors no longer need to pick individual stocks to express a view. They can buy broad indexes, sectors, themes, leveraged products, inverse products, covered-call funds, single-stock ETFs, and crypto-linked exposures in seconds. A wave of retail participation can quickly become a wave of market-wide or sector-specific flows. Options add another layer — during risk-on periods, heavy call buying can influence dealer hedging and amplify momentum in underlying stocks.

This is why the elimination of the PDT rule cannot be judged only by how many people day trade individual stocks. The modern retail market is connected to ETFs, options, margin, algorithmic hedging, market making, and sector momentum. A rule change that expands active access reverberates through the entire trading ecosystem.

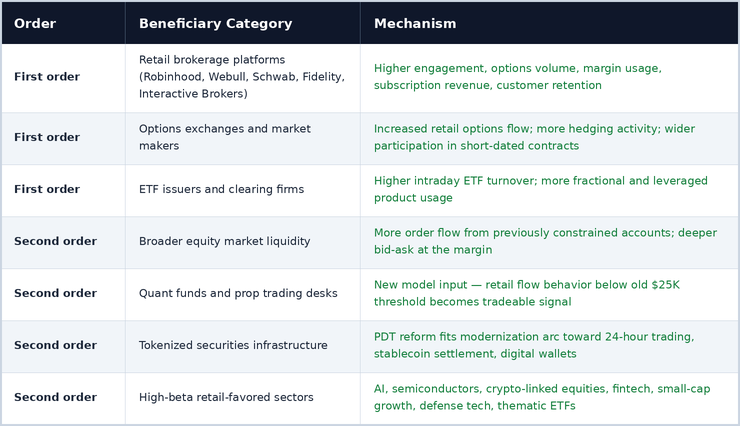

Who Benefits

The first-order beneficiaries are brokerage platforms and market infrastructure companies. But the second-order effects may matter more — and they spread considerably wider.

Shares of Robinhood and Webull reacted positively after the SEC approved the rule change. The broader implication is that if retail activity rises across these platforms, the equity market receives more liquidity, more order flow, more momentum participation, and more speculative capital — the inputs that help drive valuation cycles.

The Tokenization Connection

The elimination of the PDT rule also fits into a larger transition toward faster, more open, and more technology-driven market infrastructure.

The old market structure was built around fixed trading hours, broker-imposed account thresholds, delayed settlement, legacy clearing rails, and static margin rules. The emerging structure is moving toward real-time risk management, 24-hour trading, fractional shares, tokenized securities, digital wallets, stablecoin settlement, and programmable corporate actions.

If tokenized stocks, tokenized ETFs, and blockchain-based securities are eventually built within a compliant structure that preserves real shareholder rights, custody protections, voting rights, dividend rights, and regulatory oversight, the market could move toward a much larger global participation model. The PDT rule change is one more sign that regulation is slowly catching up to a real-time market.

The Risk Side

A credible thesis must acknowledge the risks.

The elimination of the PDT rule will almost certainly increase risk for some investors. Easier day-trading access can lead to overtrading, leverage, emotional decision-making, options losses, margin deficits, and sharper volatility. A more open market can also become a more speculative market.

That does not weaken the structural thesis. It may confirm it. Market access and market activity have historically moved together. The challenge for regulators and brokers will be to pair broader access with real-time risk controls, customer education, transparent disclosures, and account-level protections.

The Bottom Line

The elimination of the $25,000 Pattern Day Trader rule is another milestone in the long-term democratization of U.S. equity markets.

Online brokerage lowered access barriers. Decimalization lowered spreads. ETFs simplified exposure. Zero commissions removed direct trading costs. Fractional shares lowered account-size barriers. Mobile apps increased engagement. Now, intraday margin reform removes one of the last major restrictions on smaller active traders.

If approximately 40 million new retail brokerage accounts were created during and after the pandemic-era trading boom, and even 40% to 55% of that cohort becomes meaningfully eligible for more active trading, the rule change could unlock 16 million to 22 million accounts — with an aggressive case approaching 25 million.

That is not symbolic. It is a structural expansion of the active-trading market.

The next equity bull market will still depend on earnings, interest rates, productivity, artificial intelligence, and corporate profits. But another force should not be ignored: access. When access broadens, liquidity expands. When liquidity expands, markets reprice. And when Wall Street removes friction, new capital has a long history of finding its way into equities.

This time, trading desks and quant funds may already be preparing for that shift before the rest of the market fully appreciates it.

Sources: FINRA Regulatory Notice 26-10, effective June 4, 2026; Charles Schwab; Federal Register SEC notice on FINRA Rule 4210 amendments; Reuters / J.P. Morgan retail activity data, December 2025.