The Playbook: How to Position for the Largest Productivity Shock in U.S. Economic History

This is Part Three of a three-part series on agentic AI and the U.S. economy. Part One laid out the macro thesis and scenario framework — why mainstream forecasts are structurally wrong and what the services-first math actually produces. Part Two examined the 1923–29 Roaring Twenties analog and what history tells us about how this ends. This is the investment playbook.

I. The Trade in One Paragraph

Agentic AI is compressing 40–55% of cognitive services labor costs over a 5–7 year window, redirecting $3–5 trillion of services labor compensation into capital returns, and creating a productivity acceleration comparable to the 1923–29 electrification boom, applied to a services base 2.3 times larger as a share of GDP. Real GDP re-rates higher. Services prices deflate 18–28%. Labor's share of GDP drops from 56% toward 45–49%. Capital captures most of the gains.

The investment opportunity is to own the pipes, the data fortresses, the physical-asset moats, and the credentialed gatekeepers of the AI economy, while underweighting or shorting the staffing firms, commercial real estate services, ad agency holdcos, for-profit education incumbents, and undifferentiated SaaS sitting on the wrong side of that reallocation.

One constraint from the historical record before we get into positions: the 1920s productivity boom didn't end because electrification stopped working. It ended because the financial and distributional structure built on top of it became too fragile to absorb a confidence shock. That argues for building this portfolio with roughly 30% in physical-asset services, regulated rails, healthcare, and power, not 100% in semis and software. The complete trade owns both the primary wave and the fragility hedge. Anything less is the 1927 portfolio.

II. The Seven-Area Framework — Winners and Losers

The market has already done some of the work. NVDA, AVGO, and PLTR have been bid to multiples that price in a significant portion of the AI upside. Meanwhile, the staffing firms, CRE services names, and for-profit education stocks have sold off, but in several cases not enough to account for the structural revenue impairment heading their way.

The framework below organizes the investable universe into seven winning areas and six losing areas. The narrative behind each matters as much as the names.

On the winning side, the logic differs by category and it is worth being precise.

AI infrastructure such as compute, networking, and power, wins because capex flows here regardless of which application layer ultimately dominates. NVDA's GPU monopoly, AVGO's custom silicon, ANET's data-center networking, ASML's EUV lithography monopoly, and the power infrastructure names — VRT, ETN, GEV, CEG, VST — are the physical substrate of the build-out. Application preferences change. The infrastructure underneath them doesn't.

The hyperscaler clouds — MSFT, GOOGL, AMZN — win because they own agent runtime and distribution. Whatever agentic application an enterprise deploys, it almost certainly runs on Azure, Google Cloud, or AWS. The hyperscalers are the landlords of the AI economy, collecting rent regardless of which tenant's application succeeds.

Data fortresses are the highest-conviction value call in the framework. RELX, Wolters Kluwer, Thomson Reuters, SPGI, MCO, ICE, and INTU own the proprietary, structured, legally validated data that makes agents useful inside regulated verticals. A legal agent that cannot access Lexis or Westlaw is not a legal agent that BigLaw will pay for. A financial agent that cannot access S&P's data infrastructure is not an agent that a risk committee will approve. These companies were sold down on AI-disintermediation fears and the market got the thesis precisely backwards. They are not being substituted. They are becoming the substrate.

Physical-asset business services and rail — WM, RSG, ROL, CTAS, CSX — win because AI enhances their back-office economics without threatening their core asset. Waste collection, pest control, uniform services, and similar businesses have route density, physical infrastructure, and customer relationships that no agent stack can replicate. AI compresses their overhead and improves their dispatch and routing — margin expansion without displacement risk. CSX belongs in this category for a related but distinct reason: rail is the physical logistics backbone of the goods economy, and agentic AI applied to freight scheduling, route optimization, and predictive maintenance compounds the operating leverage of a network business that already has enormous fixed-cost advantages. The AI transition that displaces white-collar services workers simultaneously accelerates the physical goods flows that rail carries — and CSX captures that tailwind while remaining structurally immune to the substitution risk that defines the losing side of this trade.

Regulated payments, exchanges, and major investment banks — V, MA, ICE, CME, NDAQ, GS, MS — win for compounding reasons. The payment and exchange rails cannot be disintermediated: every AI-generated transaction, every tokenized asset, every algorithmic trade still clears through this infrastructure, and volume growth in an AI-accelerated economy is unambiguously positive for these names. Goldman Sachs and Morgan Stanley belong in this category for a reason that goes beyond the infrastructure argument. They are among the largest beneficiaries of the agentic AI transition by any measure — AI compresses their back-office and research costs dramatically while bull-market trading revenues surge on the back of the productivity boom. Add agentic AI trading as an entirely new revenue layer on top of that, and GS and MS are not merely participants in the AI economy. They are among its biggest winners, and the market has not fully priced that dual tailwind.

Embodied healthcare and robotics — ISRG, LLY, NVO, SYM, KSCP — win because physical delivery of care is the category that AI augments most dramatically without replacing the physical component. Surgical robotics, GLP-1 biologics, and autonomous logistics are all AI-accelerated but not AI-substituted. The human or the robot still has to show up.

Vertical AI software with proprietary data, mobility, and consumer tech — NOW, CRM, ORCL, PLTR, INTU, UBER, AAPL — wins where the underlying asset compounds in value as AI capability grows. For the software names, the key word is proprietary. Generic SaaS without a data advantage loses. Vertical software where the AI is trained on years of customer-specific process data — ServiceNow's workflow intelligence, Palantir's ontology, Oracle's ERP data depth — builds a switching cost that gets higher, not lower, as agents become more capable. Uber belongs in this category because agentic AI optimizes fleet economics, dynamic pricing, and driver-rider matching in real time — compressing costs and expanding margins while urban mobility demand accelerates alongside the broader productivity boom. Apple belongs here because AI-native app proliferation drives both device upgrade cycles and App Store revenue. Every new agentic application that reaches consumers at scale runs on Apple hardware and through Apple's distribution infrastructure. Services revenue compounds on the world's largest installed base, and that compounding gets faster, not slower, as the AI app ecosystem matures.

On the losing side, the mechanism is equally specific.

Staffing and BPO — MAN, RHI, KFY, ADP in part — lose because their product is the cognitive labor that is being displaced. Resume screening, candidate assessment, scheduling, onboarding administration, as these are precisely the tasks that agentic workflows are eliminating fastest. The staffing industry's revenue is correlated with white-collar headcount. White-collar headcount is the variable our scenarios show falling most sharply.

Commercial real estate services — CBRE, JLL, CWK — lose because their tenants are the displaced services workers. Law firms, consulting firms, financial services back offices, and corporate middle management layers are the demand base for Class A office space. As those headcount pools compress, the demand for office square footage compresses with them. The CRE services firms are exposed to both transaction volume declining and lease renewal rates deteriorating simultaneously.

Ad agency holdcos — WPP, IPG, OMC — are being squeezed from both sides. AI tools are commoditizing the creative and copy output they have charged premium rates to produce, while their largest clients are increasingly moving spend directly to platform APIs rather than through agency intermediaries. The agency model's structural position is eroding faster than their earnings guidance reflects.

For-profit education — CHGG, GHC, STRA, LAUR — face a credential ROI problem that is not cyclical. When the credentialed knowledge worker is the category being displaced, the ROI calculation on a $150,000 professional degree changes fundamentally. These businesses are exposed to both enrollment pressure and product-value pressure simultaneously.

Legacy thin-data SaaS — DOCU, TWLO, and the undifferentiated HR-tech names — face margin compression as enterprise customers renegotiate pricing in a world where agent workflows reduce the human workflows that drove SaaS seat counts. If the seats aren't occupied by humans, the per-seat pricing model collapses.

III. Where the Market Has and Hasn't Adjusted — The Three Value Pockets

The consensus trades in this thesis are fully priced or beyond. NVDA trades at multiples that require near-perfect execution of the most bullish scenario. AVGO and PLTR are in similar territory. C3.ai and the recently-SPAC'd "AI agent" platforms are showing margin breakage as enterprise customers renegotiate contracts that were signed before they understood the real cost-to-value ratio of early agentic deployments.

The interesting money, the trades with the highest expected alpha-to-risk ratio at current prices, sits in three specific pockets the market has mispriced.

Pocket A — Over-punished data fortresses. RELX, Wolters Kluwer, Thomson Reuters, and SPGI fell as much as 50% from peak on AI-disintermediation fears in 2024 and early 2025. The sell-off thesis was that AI would make their data redundant by synthesizing information from open-web sources. That thesis was wrong, and the market is beginning to recognize it. Regulated verticals — legal, financial, scientific, regulatory — require sourced, auditable, legally defensible data. Open-web synthesis does not meet that standard. These companies own the structured data that makes agents credible inside regulated workflows. They are not being replaced. They are being integrated. At current valuations, they are the highest-conviction value call in the AI investment universe.

Pocket B — Quality compounders dragged down with the SaaS basket. The 2024–2025 SaaS de-rating was indiscriminate. Companies with genuine AI-accretive business models were sold alongside the genuinely impaired ones because they shared an asset class label. ANET trades approximately 25% below Morningstar fair value despite data-center networking demand that is structurally accelerating. GOOGL trades at approximately 7% below fair value despite owning one of the two or three most defensible AI infrastructure positions in the world. INTU and ROP trade at discounts to growth comps despite data moats that are, if anything, more valuable in an AI-native world. The franchise quality is intact. The valuation is the opportunity.

Pocket C — Cheap-multiple infrastructure small and mid caps. The AI infrastructure build-out extends well below the large-cap names that dominate analyst coverage. INOD, CRDO, ALAB, MRVL, and MU are the silicon and data plumbing of the build-out — the components that go into the systems that NVDA's GPUs run on, that ANET's switches connect, that the hyperscalers' data centers are built with. RMNI at approximately 7x forward earnings represents the kind of valuation anomaly that only exists because the name is too small and too unglamorous to attract the capital flows chasing the headline AI theme.

What is not cheap and should be sized down or avoided entirely: NVDA above 35x forward earnings, AVGO above 30x, PLTR above 25x revenue, and any name that describes itself as an "AI agent platform" without a clear path to recurring revenue at scale. The history of every productivity revolution is that the second-derivative beneficiaries outperform the obvious first-derivative ones over a five-year window. The picks-and-shovels trade, applied to the data and regulated-moat layer rather than the compute layer, is where the alpha lives from here.

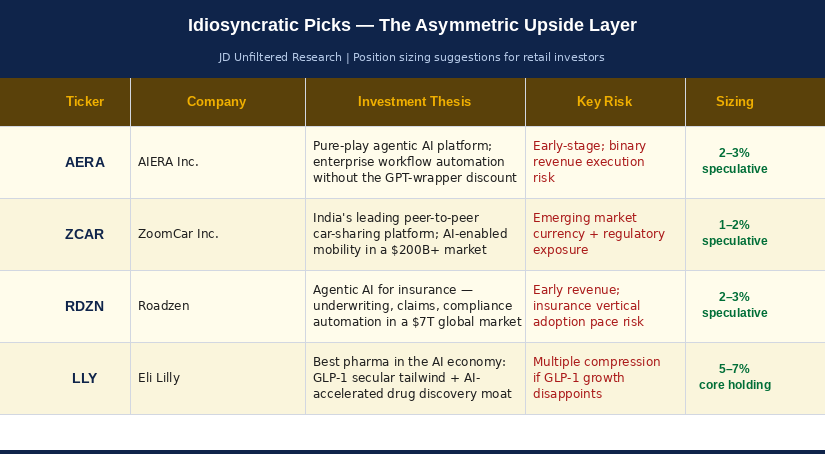

IV. The Idiosyncratic Plays — Asymmetric Upside for the Conviction Sleeve

Every institutional playbook has a speculative kicker sleeve. Every retail investor with conviction in a thesis wants the name that captures the upside if the central scenario plays out more aggressively than the model suggests. The four names below serve that function — each with a specific thesis, a specific risk, and a suggested position size that reflects the asymmetry of the payoff.

AERA — AIERA Inc.: The Pure Agentic AI Play

AIERA represents the purest public-market expression of the agentic AI thesis available at current prices. Where most "AI companies" in the public markets are either infrastructure providers (NVDA, ANET) or legacy software firms adding AI features to existing products (CRM, ORCL), AIERA is building native agentic workflow infrastructure — systems designed from the ground up for multi-step autonomous task execution rather than retrofitted around a single-model assistant.

The distinction matters because the enterprise value of agentic AI, as we argued in Part One, is not in making existing workflows 25% faster. It is in replacing entire workflow layers with agent chains that run at a fraction of the human cost. A company that builds the infrastructure for that replacement, not the agents themselves, but the orchestration and governance layer that makes agent workflows enterprise-deployable, sits at the highest-value point in the stack.

The risk is execution and timing. AIERA is early-stage in its revenue ramp, and the enterprise adoption curve for true agentic infrastructure, as opposed to AI assistants branded as agents, is still in its early innings. Binary revenue outcomes are a real possibility. Size accordingly: 1–2% of portfolio as a speculative kicker, not a core position.

ZCAR — ZoomCar Inc.: The Indian Mobility Play

ZoomCar is India's leading peer-to-peer car-sharing platform, effectively the Turo of the world's most rapidly expanding middle-class consumer market. The AI connection is second-derivative but real: as we noted in Part One, India and the broader South/Southeast Asian emerging market is the single largest beneficiary of the offshore knowledge-services export opportunity that agentic AI creates. A rising Indian middle-class consumer economy, turbocharged by AI-enabled productivity gains in the country's substantial services export sector, is a powerful macro tailwind for consumer mobility platforms.

ZoomCar's specific opportunity is the transition from ownership to access in a market where per-capita car ownership is still a fraction of U.S. levels but where smartphone penetration and digital payment infrastructure have already reached scale. AI-optimized fleet matching, dynamic pricing, and predictive maintenance compress the unit economics of the peer-to-peer model in ways that make it viable at price points the Indian consumer market can support.

The risks are real: emerging market currency exposure, regulatory complexity across Indian states, and the competitive pressure from domestic and global mobility platforms all represent genuine headwinds. Size at 1–2% of portfolio as an emerging-market speculative position. The upside, if the Indian consumer mobility market develops as the macro thesis suggests, is multiples on the current price.

RDZN — Roadzen: Agentic AI for Insurance

Insurance is one of the largest, most data-intensive, and most ripe-for-disruption cognitive services verticals in the global economy. Underwriting, claims processing, fraud detection, compliance documentation, and customer service in insurance are precisely the kinds of high-volume, rule-governed, document-intensive cognitive workflows that agentic AI can compress most aggressively. The global insurance market is approximately $7 trillion annually. The cognitive labor embedded in its operations is one of the largest pools in our vertical displacement framework.

Roadzen is building the agentic AI infrastructure layer for the insurance vertical, not a single point solution for claims or underwriting, but an integrated workflow automation platform designed for the specific regulatory, auditability, and liability requirements of insurance operations. The moat is vertical specificity: insurance workflows require understanding of policy language, regulatory jurisdiction, claims adjudication standards, and liability frameworks that a generic agent cannot navigate without domain-specific training.

The setup is attractive: the insurance industry has been one of the slowest major service verticals to adopt AI, which means the displacement curve that software engineering and financial analysis are already experiencing is still early innings in insurance. First-mover advantage in vertical workflow automation compounds when the customer's own data trains the platform over time. Size at 2–3% as a speculative position with a 3–5 year horizon for the thesis to develop.

LLY — Eli Lilly: The Best Pharma in the AI Economy

Lilly is not an AI stock in the conventional sense. It does not sell AI infrastructure, it is not building agent platforms, and its revenue is not directly correlated with enterprise AI adoption in the near term. It belongs in this playbook for two reasons that compound on each other.

First, LLY is the best-positioned name in the sector that AI-accelerated drug discovery most directly benefits. Drug discovery is among the most data-intensive cognitive workflows in the global economy — target identification, compound screening, clinical trial design, patient stratification, regulatory submission. Every step is being compressed by AI tooling, and the companies with the largest existing drug pipelines, the deepest molecular biology data libraries, and the most sophisticated clinical operations infrastructure capture the most value from that compression. Lilly's pipeline depth and R&D execution record position it to benefit from AI-accelerated drug discovery faster than virtually any other major pharmaceutical company.

Second, the GLP-1 secular tailwind is independent of the AI thesis and provides a durable revenue base that makes LLY one of the few large-cap names in the market where the non-AI growth story alone justifies a significant position. Semaglutide and tirzepatide are therapeutic category creators addressing obesity, cardiovascular disease, diabetes, and a growing list of adjacent indications with clinical evidence strong enough to drive decade-long revenue growth.

The risk is multiple compression if GLP-1 competitive dynamics intensify faster than expected or if clinical trial results in adjacent indications disappoint. At current valuations, LLY requires continued execution on both the pipeline and the commercial side to justify its multiple. Size at 5–7% as a core holding rather than a speculative kicker — this is the highest-quality name in the idiosyncratic layer.

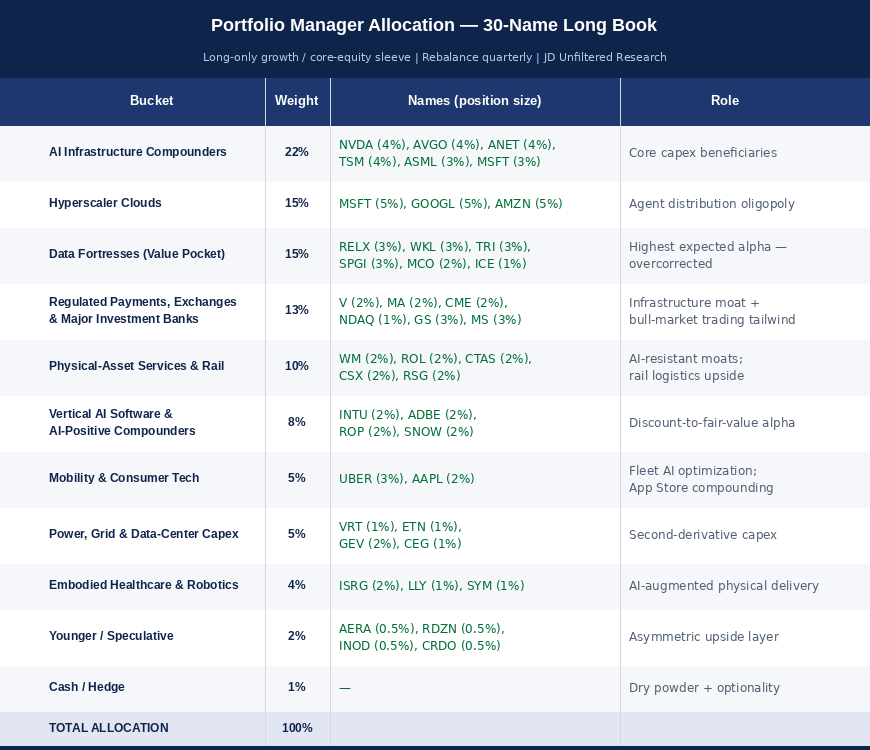

V. The Portfolio Manager Allocation

For institutional portfolio managers running a long-only growth or core-equity sleeve, the full allocation framework below captures the primary productivity wave, the second-derivative infrastructure plays, the data-fortress value pocket, the physical-asset and regulated-moat defensive layer, and the speculative kicker sleeve — in a 25-name book rebalanced quarterly.

The pair-trade overlay for long/short managers: long the data-fortress and infrastructure basket above, short an equal-dollar basket of MAN, RHI, KFY, CBRE, JLL, CWK, CHGG, GHC, and WPP. This pair captures the labor-share collapse trade directly and historically produces gross-of-fee returns regardless of whether macro plays out as Scenario A or Scenario C, because it is long the capital winners and short the labor-tied intermediaries in a world where capital captures the gains irrespective of the magnitude.

Risk parameters: 12–15% maximum single-name weight. Rebalance when any single position exceeds 18%. Target correlation to QQQ at 0.7–0.8 — this portfolio is designed to outperform the index, not hedge it. The speculative kicker sleeve should be treated as permanently at risk and sized so that its complete loss does not impair the portfolio's ability to meet benchmark.

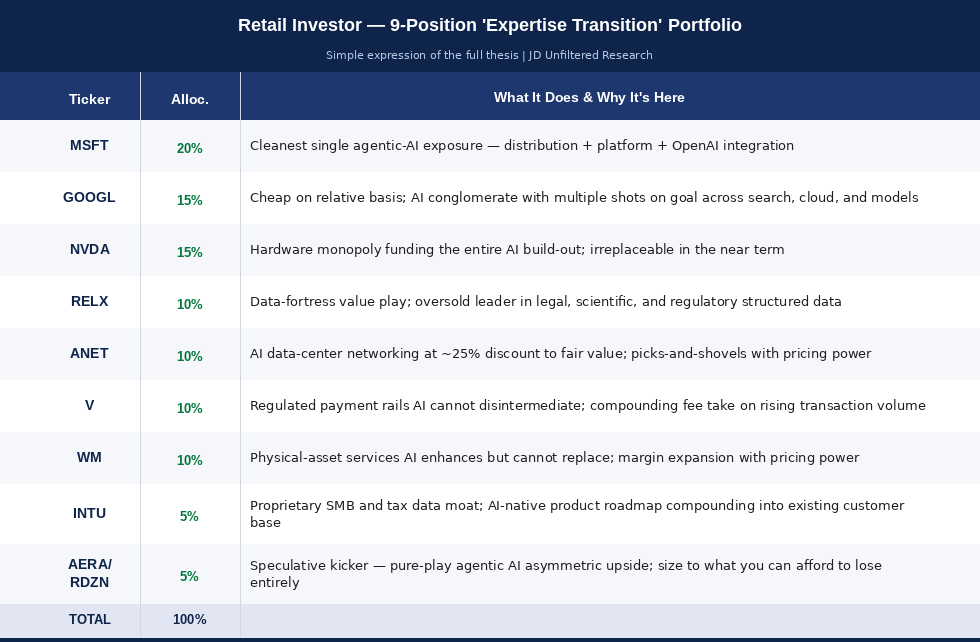

VI. The Retail Investor Playbook

For an individual investor without the time, scale, or research budget of an institutional PM, the same thesis can be expressed in a simpler portfolio that captures the majority of the institutional alpha at a fraction of the complexity.

The ETF-only version for investors who want the thesis without single-name risk: 40% QQQM for broad large-cap AI exposure at low cost, 20% IGV or SKYY for software and cloud, 15% SOXX for semiconductors, 10% XLU or VPU for utilities and AI power demand, 10% MOAT for the Morningstar wide-moat names that systematically capture the data-fortress and regulated-rail exposure, and 5% BOTZ or ROBO for robotics and embodied AI optionality.

What to avoid for retail investors, stated plainly:

Single-name concentration in PLTR, C3.ai, or any name trading above 30x sales. The history of every productivity revolution is that the consensus first-derivative plays get crowded, priced to perfection, and then de-rated when execution misses the implied growth trajectory — even slightly. Owning NVDA at 5% of portfolio is rational. Owning it at 25% is momentum speculation dressed up as thematic investing.

The ad-agency and staffing-firm "value traps" — WPP, IPG, MAN, RHI — that look statistically cheap on trailing earnings multiples but face structural revenue compression that makes those multiples misleading. A stock is only cheap if the earnings power is durable. In these names, it is not.

For-profit education and most legacy SaaS that has not fundamentally repriced its product around agent workflows. CHGG in particular has already reflected a significant portion of its impairment, but the structural problem — an industry whose product ROI math is broken by the same AI wave that is disrupting its customers — has not been fully discounted.

VII. The Five Rules of the Playbook

These are the principles that govern the allocation framework regardless of whether you are running a $500 million institutional sleeve or a $50,000 individual account. They flow directly from the macro thesis and the historical analog.

Rule One: Own the pipes, the data, and the physical assets. Rent the applications.

Applications come and go. The infrastructure and data substrate they run on compounds in value as the applications proliferate. NVDA's GPUs are the pipes. RELX's legal and scientific data is the substrate. WM's route density is the physical asset. These are the positions to size with conviction and hold through the volatility. The specific application layer that dominates in 2028 is unknowable today. The infrastructure it runs on is not.

Rule Two: Buy the over-punished data fortresses. Sell the consensus losers that haven't fully adjusted.

RELX, Wolters Kluwer, Thomson Reuters, and SPGI long. MAN, RHI, CBRE, and CHGG short or avoid. The market mispriced the AI impact in both directions — it assumed the data fortresses would be disintermediated and it has been slow to fully discount the structural revenue impairment in the labor-tied intermediaries. Both corrections are still in progress.

Rule Three: Don't pay 30x sales for anything.

The second-derivative beneficiaries outperform the obvious first-derivative ones over a five-year window — every time, in every productivity revolution the historical record documents. The electrification era's biggest long-term winners were not the electric equipment manufacturers but the companies that used cheap electricity to compress their production costs and expand their margins. The AI era's biggest five-year winners will not be NVDA but the companies that use cheap AI to compress their cognitive labor costs and reprice their competitive position. Those companies are mostly trading at single-digit earnings multiples today.

Rule Four: Position for services deflation.

Long duration assets, long utilities and power, long regulated rails, underweight cyclical services tied to white-collar headcount. Kevin Warsh is right that AI is the most significant disinflationary force in the current economy. Services price deflation of 18–28% over the thesis horizon implies a rate environment that is structurally more accommodative than the consensus expects — which is unambiguously positive for long-duration instruments, utility cash flows, and regulated asset returns.

Rule Five: Rebalance against the labor-share collapse.

This is the discipline rule. When capital share of GDP rises another 100 basis points — and it will, repeatedly, over the thesis horizon — trim the cyclically-exposed labor-tied names that have not fully repriced and add to the data-fortress and physical-asset moat names. The thesis has a direction: labor to capital. Rebalancing against that direction rather than chasing it is how the portfolio captures the full trade rather than the first leg of it.

VIII. The Horizon Is the Edge

The single most important variable in this playbook is not the stock selection. It is the time horizon.

The 1920s productivity boom rewarded patient owners of the right businesses for an entire decade. The electrification trade was not a 12-month momentum position — it was a structural repricing of the American industrial economy that took a full decade to mature. Investors who held the right businesses through the volatility of 1924, 1926, and 1928 captured the full return. Investors who traded in and out of the momentum captured a fraction of it and paid the transaction costs of their own impatience.

The agentic AI trade is structurally similar, with one important difference: the compression timeline is 5–7 years rather than 15. The full thesis — services labor displacement, margin expansion, GDP re-rating, services deflation, rate environment repricing — does not play out in a single earnings cycle or a single Fed decision. It plays out over the horizon of a presidential term, a capital expenditure cycle, and a generational shift in how cognitive work is organized and compensated.

The 1929 cautionary note from Part Two matters here too. The boom didn't end because productivity stopped — TFP kept rising into the Depression. It ended because the distributional and financial fragility of the structure built on top of the productivity gains collapsed under its own weight. The defensive composition of this portfolio — 30% in physical-asset services, regulated rails, healthcare, and power — is not timidity about the AI thesis. It is the lesson of 1929, applied.

Own the substrate of the post-expertise economy. Underweight the labor-tied service intermediaries the substrate is replacing. Size both sides of the trade with a horizon long enough to outlast the volatility of the transition. And hold with the conviction that comes from understanding not just what is happening, but why it has happened before — and how it ended.

The authors hold or may hold positions in securities discussed in this article and reserve the right to buy or sell shares at any time without notice. This article is for informational and educational purposes only and does not constitute investment advice. All investments involve risk, including the possible loss of principal. Past performance is not indicative of future results. Readers should conduct their own due diligence and consult a qualified financial advisor before making any investment decisions.