Vivos Therapeutics (NASDAQ: VVOS) A Two-Pillar MAJOR BUY

The Lowest-Cost Chronic-Disease Aggregation Platform Meets a Structurally Engineered Short Squeeze

★ MAJOR BUY RECOMMENDATION ★

Status: Pre-Catalyst (Nasdaq compliance deadline: June 30, 2026)

Executive Summary

We rate Vivos Therapeutics (NASDAQ: VVOS) a MAJOR BUY on the strength of two independent and coequal pillars, each of which would justify a long position on its own and which together create an exceptionally asymmetric risk/reward profile.

Pillar I — The Hypoxia Patient-Aggregation Platform. Vivos is misclassified by the market as a small-cap sleep-apnea device company. In reality, it is the only publicly traded company in the United States systematically using sleep-apnea-induced chronic intermittent hypoxia as the single lowest-cost entry point for aggregating the entire chronic-disease patient population — patients who share a 30% to greater-than-50% comorbidity relationship across virtually every major chronic-disease category, all originating from the same root pathology of oxidative and nitrosative stress. This makes Vivos's patient base the most valuable customer agglomeration in US healthcare for pharma and nutraceutical companies.

Pillar II — The Structural Short Squeeze. An estimated 40 million share naked short overhang, accumulated through successive reverse splits and predatory shorting, must be closed against a fixed and shrinking common float. The Streeterville standstill removes a known seller, and a truly perpetual, non-convertible preferred — with no put — cures the Nasdaq stockholders' equity deficiency while sealing off the only escape valve, synthetic supply, through which short sellers could otherwise cover.

These pillars are mutually reinforcing. The market's recognition of the hypoxia patient-aggregation value is the demand catalyst that ignites the squeeze, and the squeeze amplifies the re-rating the platform thesis independently justifies. We expect the decisive actions to be executed before June 30, 2026.

Pillar I — The Lowest-Cost Chronic-Disease Patient Aggregation Platform

1.1 The Reframing

Vivos is publicly classified as an obstructive-sleep-apnea device company. That classification is fundamentally incomplete and dramatically understates the strategic value of the asset. Vivos has recognized that sleep-apnea-induced hypoxia is the single lowest-cost entry point for identifying and aggregating the entire chronic-disease patient population.

1.2 The Root-Cause Cascade

Chronic intermittent hypoxia is among the first physical manifestations of a deeper imbalance — an overwhelmed human antioxidant system producing chronic oxidative and nitrosative stress. This same root pathology drives the comorbidity cluster that runs across cardiovascular disease, kidney disease, metabolic disease, and the broader chronic-disease burden that accounts for the overwhelming majority of the roughly $5 trillion the US spends on healthcare. Patients identified through hypoxia share a 30% to greater-than-50% comorbidity relationship across virtually every major chronic-disease category.

1.3 Why This Is the Most Valuable Patient Cohort to Pharma and Nutraceuticals

The hypoxia-positive population is precisely the cohort that every pharma and nutraceutical company most wants to reach: patients who are upstream of multiple chronic diseases, carry dense comorbidities, and represent recurring, multi-category therapeutic demand. The same value that made this cohort attractive to GLP-1 / obesity franchises extends to pharma companies of every stripe across every crossover chronic disease — cardiometabolic, renal, inflammatory, and beyond. Aggregating these patients at the lowest possible cost of identification is the highest-leverage position in US healthcare.

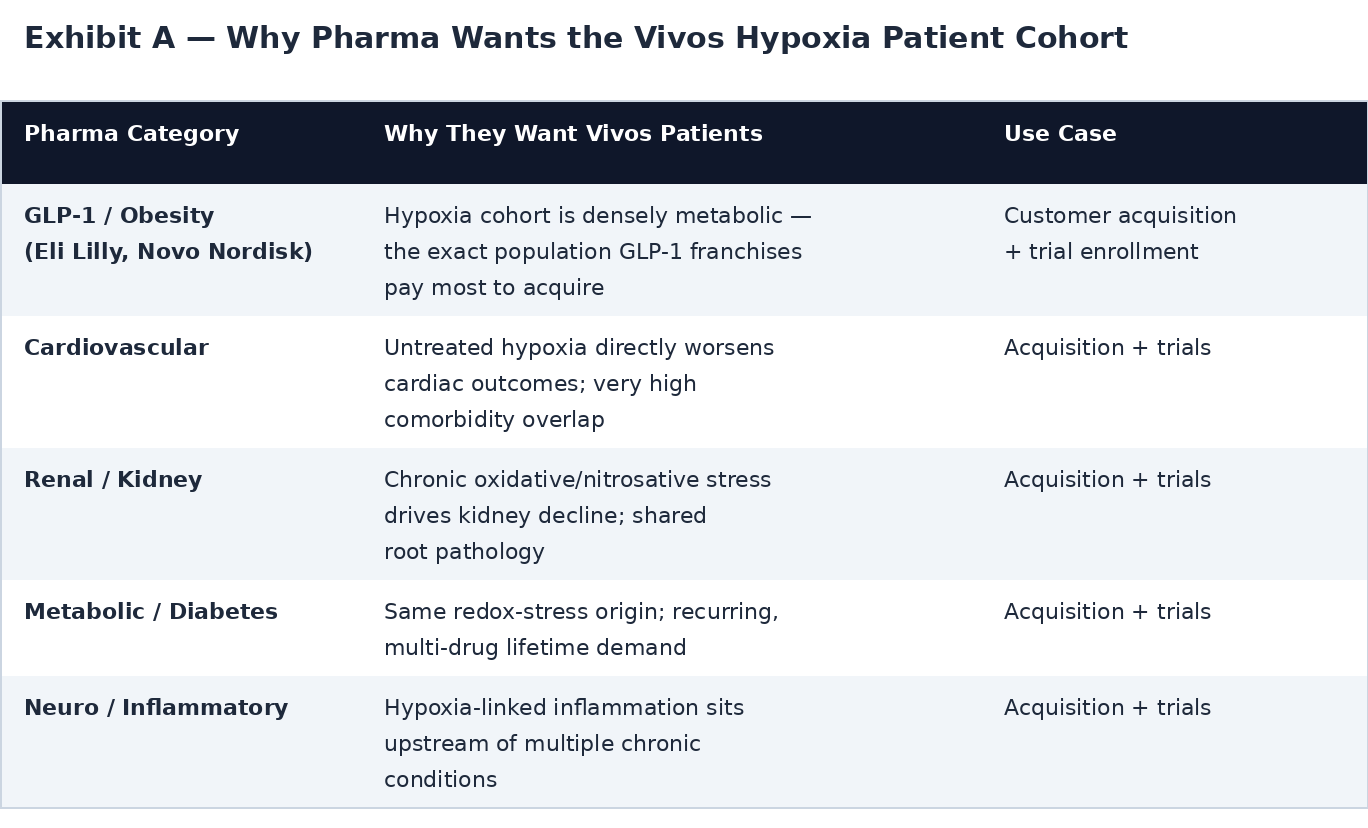

1.4 Exhibit A — Why Pharma Wants the Vivos Hypoxia Patient Cohort

Each category below shares the 30% to greater-than-50% comorbidity overlap with the hypoxia-positive population, because all trace to the same root pathology of chronic oxidative and nitrosative stress. The same patient is therefore independently valuable to multiple pharma franchises at once — for both customer acquisition and clinical-trial enrollment.

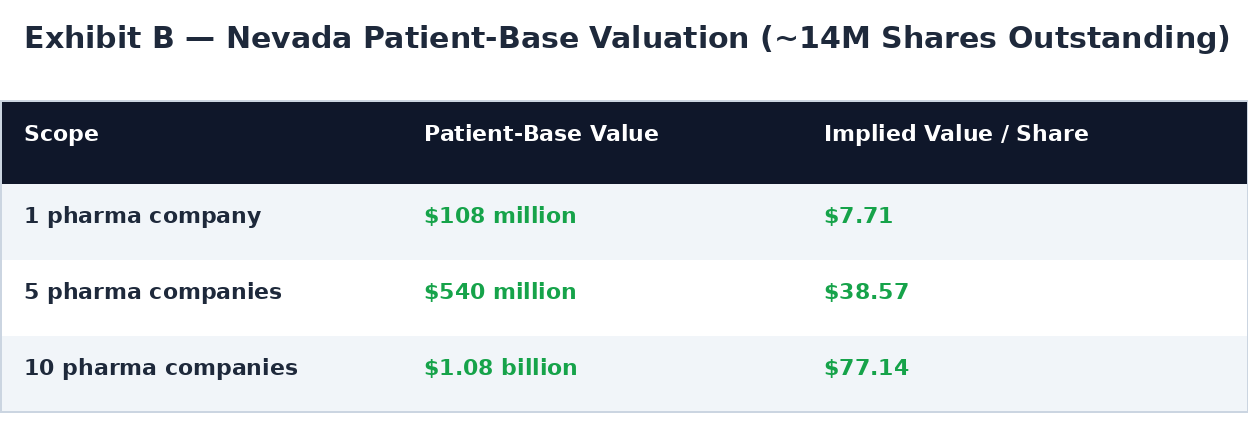

1.5 Exhibit B — Nevada Patient-Base Valuation and Implied Value Per Share

Valuing the 36,000 annual Nevada patients at $3,000 each — a value applicable to both customer acquisition and clinical-trial use — produces $108 million of value per pharma company. Dividing by the approximately 14 million common shares outstanding gives the implied per-share value the patient base alone supports. Because the comorbidity overlap makes the same patient valuable to many franchises simultaneously, these values are additive across companies rather than mutually exclusive.

This is the strategic crux: at just the Nevada patient base — before any national expansion through the asset-light clinic model — the cohort's value to pharma supports an implied $7.71 to $77.14 per share, against a current VVOS share price that is a small fraction of even the single-pharma figure.

1.6 The Asset-Light Aggregation Model

Vivos is already executing this strategy through partnerships with other chronic-disease clinics whose patient outcomes suffer because the underlying hypoxia goes untreated:

- Sleep centers first — the natural beachhead, where the test-treat-test workflow is proven.

- Cardiovascular centers second — Vivos installs its sleep physicians to test the cardiac-disease patients for hypoxia and splits the incremental testing revenue 80% to Vivos and 20% to the partner clinic.

This is an asset-light way to conquer chronic-disease aggregation: Vivos does not buy the clinics; it embeds its diagnostic protocol inside existing chronic-disease patient flows and monetizes the previously undiagnosed hypoxia. Each new disease-clinic vertical compounds the size and value of the aggregated patient base — and multiplies the per-patient pharma value shown in Exhibit B well beyond the Nevada base.

1.7 The Earnings Turnaround

The integration of the Nevada sleep centers moves Vivos from a cost-absorption phase into an earnings-contribution phase, while the asset-light partnership model scales the patient base without proportional capital outlay. The market is still pricing VVOS on its trailing distressed profile rather than on the forward platform economics this model unlocks — leaving it, on this thesis, among the most undervalued companies on the Nasdaq.

Pillar II — The Structural Short Squeeze

2.1 The Short Overhang

We estimate approximately 40 million shares are naked short. This figure derives from seasoned institutional analysis of the Company's trading behavior, settlement patterns, and the structural footprints left by repeated reverse splits. The overhang is, in our assessment, predatory rather than organic — built through:

- Reverse-split harvesting — successive splits reset share counts and obscure the true scale of accumulated short positions behind a moving denominator.

- Delisting-driven pressure — the earlier Nasdaq warning for stockholders' equity below $2.5 million provided narrative cover for driving the price lower.

- Short-then-fund predation — market makers and fast-money funds short first, depress the price, then offer capital well below their average short basis.

A naked position is not backed by a borrow. Closing it requires buy-to-cover into the lit market against real shares — there is no synthetic inventory to roll, only purchase.

2.2 The Predatory Mechanics

The playbook is circular and self-funding: short into a thin micro-cap, amplify the decline using the delisting overhang, offer dilutive capital below the short basis, and cover into the resulting dilution. It works only so long as the Company keeps issuing common at depressed prices. The moment the balance sheet is cured without issuing common, the cycle breaks and the short position is stranded.

2.3 The Catalyst Stack

- Streeterville standstill (announced Friday) — a 60-day no-sell of common, a 90-day debt-payment moratorium, and up to $4.5M of debt converted to perpetual preferred when matched by other equity sources.

- Seneca Partners private placement — true private capital that satisfies the match condition and activates the antidilutive cure. This is the linchpin.

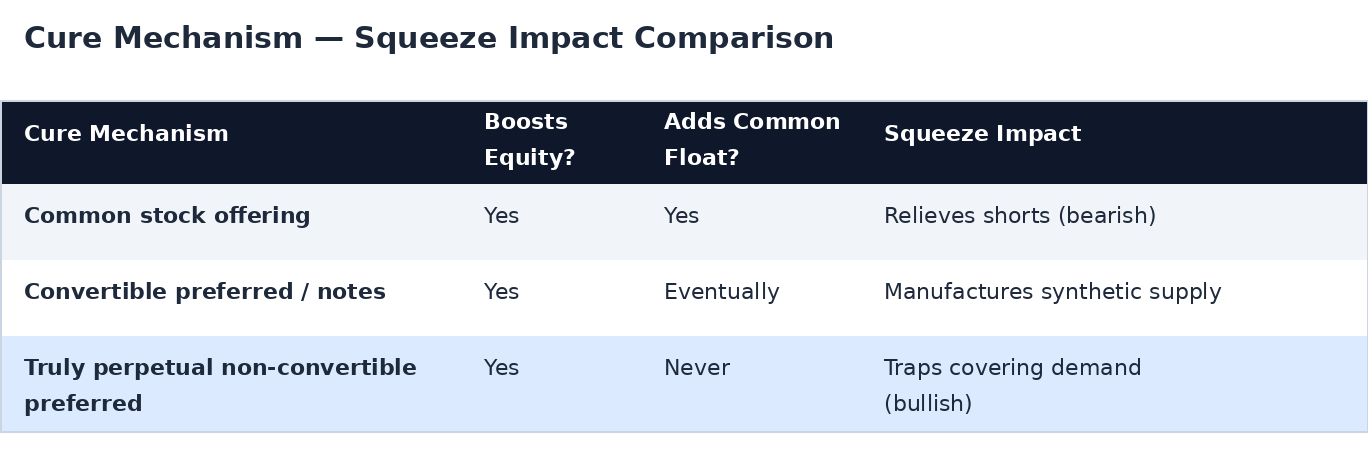

- Truly perpetual, non-convertible preferred (no put) — lifts stockholders' equity toward the $2.5M Nasdaq minimum with no maturity, no conversion into common, and no holder redemption right. It is permanent equity that can never become a common share and can never pull cash out of the Company.

- Value recognition — the hypoxia patient-aggregation platform (Pillar I) supplies the demand-side catalyst.

2.4 Why the Structure Is Antidilutive

A convertible instrument would have manufactured the exact synthetic supply that lets shorts cover without bidding up real shares. A truly perpetual, non-convertible preferred with no put eliminates that path entirely. The 40M naked overhang must be closed against a fixed common float.

2.5 The Squeeze Mechanics

- Float shrinks — the 60-day standstill withdraws the most predictable supply.

- Equity cures without common issuance — the dilution escape valve is permanently sealed.

- Demand catalyst lands — Pillar I value recognition draws real buyers.

- Forced covering has nowhere to source — 40M of buy-to-cover demand meets a shrinking, fixed common pool.

When supply is fixed and falling while forced demand is large and rising, price discovery becomes violent. This is the textbook precondition for a vertical move.

Why the Two Pillars Reinforce Each Other

The pillars are coequal, but they are also coupled. Pillar I is the fuel; Pillar II is the ignition.

- The platform re-rating (Pillar I) is precisely the demand catalyst that forces covering (Pillar II). Buyers arriving for the highest-value chronic-disease patient base in US healthcare tighten the float just as shorts must source real shares.

- The squeeze (Pillar II) accelerates and overshoots the platform re-rating (Pillar I), carrying the price beyond fair value on forced demand before it settles at the level the platform economics justify.

- Each pillar de-risks the other: if the squeeze is slower than expected, the platform value still supports the valuation; if platform recognition lags, the structural setup still forces covering. The downside cases are not correlated, which is what makes the combined thesis asymmetric.

Conclusion

Vivos Therapeutics offers two independent, coequal reasons to be a MAJOR BUY: a dramatic undervaluation revealed by its patient base, and a structurally engineered short squeeze. Valued solely on its 36,000 Nevada patients at $3,000 each, the company's patient base supports an implied value of $7.71 per share with a single pharma partner, $38.57 per share across five, and $77.14 per share across ten — against a current share price a small fraction of even the single-pharma figure. This is before any national expansion through the asset-light 80/20 clinic model, which multiplies the aggregated base well beyond Nevada.

Layered on top of that undervaluation is the short-squeeze dynamic: an estimated 40 million share naked overhang that must close against a fixed, shrinking common float, with every escape valve sealed by a truly perpetual, non-convertible preferred and a known seller removed by the Streeterville standstill. The two forces compound — platform recognition ignites the squeeze, and the squeeze accelerates the re-rating the patient-base economics independently justify.

This combination of dramatic undervaluation and short-squeeze dynamics underlies our MAJOR BUY recommendation. We expect the decisive actions to be executed before June 30, 2026.

Disclosure: This report is based on publicly available clinical data, published preclinical research, SEC filings, corporate press releases, CDC chronic-disease statistics, regulatory frameworks, and deal terms. The authors hold positions in securities mentioned and reserve the right to buy or sell shares at any time without notice. Per-patient values, revenue-split, partnership, market-sizing, and valuation scenarios are illustrative models based on stated assumptions, not contracted or guaranteed revenue. Patient-access and data-monetization arrangements are subject to HIPAA, anti-kickback, and informed-consent requirements. It does not constitute investment advice; investors should conduct their own due diligence.