The American Orbital Singularity

How a Monopoly on Reusable Space Infrastructure Routes the Global Economy Through the United States and Makes SPCX a Generational Long-Term Buy

Executive Summary

On June 12, 2026, SpaceX went public on the NASDAQ under ticker SPCX at $135 per share, raising a base of ~$75 billion — expandable to roughly $86 billion with its 15% greenshoe — at a valuation near $1.75 trillion. Demand was overwhelming: SPCX is already trading at $166.29, up 23.18% on its first day, lifting its market cap to ~$2.17 trillion and pushing past the $2-trillion bull-case ceiling on day one. The base raise alone exceeds the combined total of every U.S. IPO in 2024 and 2025 ($73.6 billion).

This paper advances five linked propositions and one overriding investment conclusion:

- The orbital economy has a single physical gateway, and that gateway is American.

- AI compute, telecom, space mining, and defense must all flow through it.

- Competitors face a guns-or-butter capital burden the U.S. does not.

- The rational global response is to rent American infrastructure, not rebuild it — channeling foreign capital into the U.S.

- China, the only conceivable rival, is too financially encumbered to sustain the contest.

The overriding conclusion: because the United States is the structurally winning economy of the orbital age, and SPCX is the single asset that owns the chokepoint through which that economy must flow, SPCX is a massive long-term buy.

I. The Chokepoint: America's Monopoly on Reusable Rocket Infrastructure

The defining fact of 2026 is not that the U.S. launches rockets, but that it is the only nation launching reusable rockets at scale and reliability. The distinction is decisive: expendable rockets like Europe's Ariane 6 are technically usable, but only reusability delivers the cost-and-cadence advantage that makes the orbital economy viable. The U.S. conducted 181 launches in 2025 versus China's 91 and Russia's 17, and leads the world "by nearly every measure: number of launches, total mass to orbit, satellite count." SpaceX alone accounts for five of every six U.S. launches. Rivals remain at the demonstration stage — China's LandSpace reached orbit with Zhuque-3 in December 2025 but destroyed the booster on its first landing attempt. Until a competitor lands and reflies boosters at cadence and cost, there is no second on-ramp to orbit. The race to space runs through American pads — and those pads are SpaceX's.

II. Why Every High-Value Sector Flows Through the Same Gate

AI compute. Electric power has become the binding constraint on terrestrial AI, and orbital data centers solve it with uninterrupted solar energy and passive radiative cooling — claiming up to 90% lower electricity cost and zero water use. Nvidia-backed Starcloud has already placed an H100 GPU in orbit and targets a 5-gigawatt orbital data center with ~4 km solar arrays. The entire model is explicitly predicated on "falling launch costs" — which only the U.S. supplies at scale.

Telecom, mining, defense. Each converges on the same gateway:

- Satellite broadband requires sustained high-cadence deployment available only via U.S. reusable lift.

- Lunar and asteroid mining is "increasingly feasible," with analysts urging the U.S. to "define the future of space mining before rival nations do."

- Defense and intelligence demand the ability to "reliably and rapidly launch growing numbers of spacecraft" — a capability concentrated in the U.S. base.

Every one of these revenue streams must transit SpaceX's lift, and SpaceX's own Starlink already monetizes the telecom layer directly.

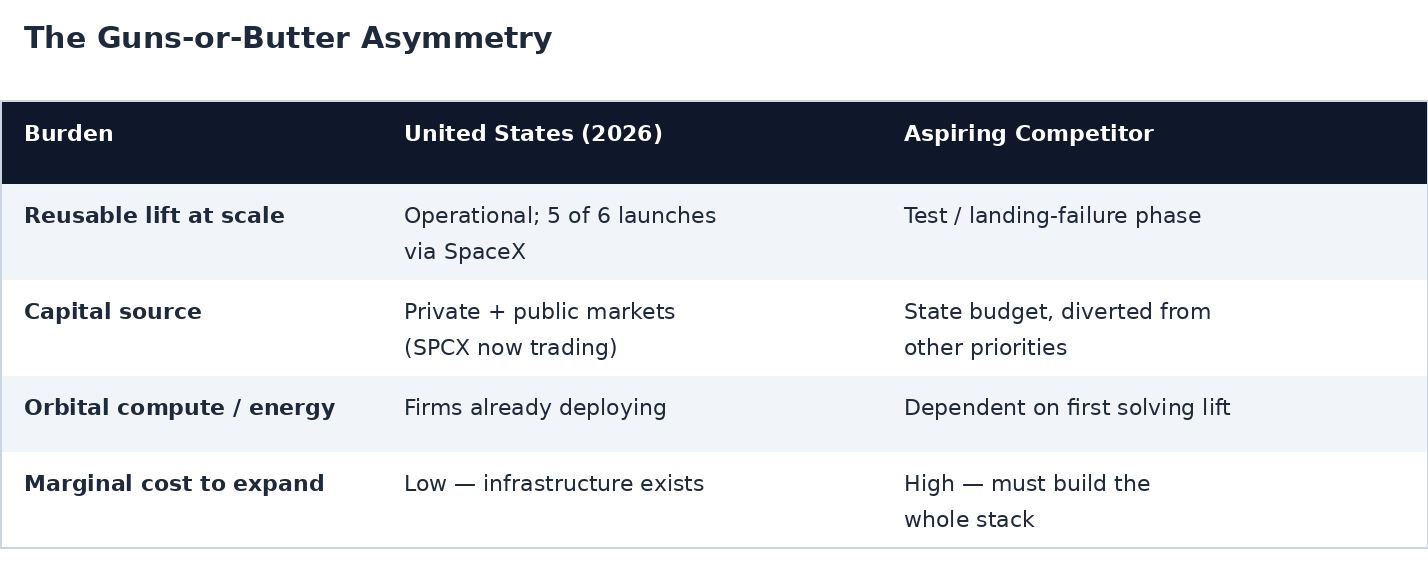

III. The Guns-or-Butter Asymmetry

To compete, a foreign state must fund the entire prerequisite stack — reusable rockets, launch sites, orbital manufacturing, solar-powered orbital compute — largely from scratch, while the U.S. private sector has already amortized that build-out.

Because launch capital requirements "make it difficult for new competitors to break in," a rival must choose between matching this spend and meeting domestic needs — a classic guns-or-butter tradeoff the U.S. does not face, having socialized the cost across deep private capital markets.

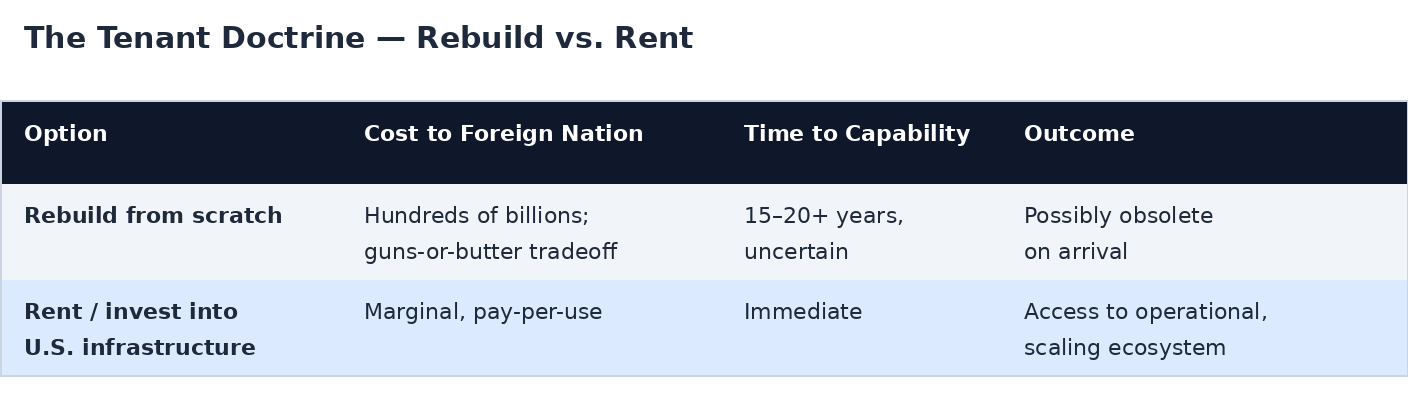

IV. The Tenant Doctrine: The World Will Pay Rent Rather Than Rebuild

The rational choice for other nations is not to duplicate the gateway but to rent it — investing capital into the U.S. to access SpaceX and its growing collateral infrastructure.

Europe is frozen out for a generation: its flagship Ariane 6 is expendable, built at high cost after a year-plus launcher gap, against an all-time European peak of just 11 launches per year (Ariane 4, mid-1990s). Analysts say Europe must "accept risk in space, or keep falling behind."

Russia has collapsed to early-1960s activity — 17 launches in 2025 — cut its space budget ~30% to roughly $17–20 billion, and abandoned its planned reusable rocket under fiscal pressure.

The developing world, including South America, lacks the capital to start from zero without sacrificing core domestic needs, leaving participation as the only rational path.

The consequence: global capital flows into the American ecosystem as rent, and a large share of that rent accrues directly to SpaceX as the gatekeeper.

V. The Reinforcing Flywheel: America's Capital and Productivity Boom

The decisive accelerant is that the U.S. is running the largest private capital-formation cycle of the century. The five largest U.S. cloud and AI firms have committed $660–690 billion in 2026 capex, nearly doubling 2025's ~$380 billion in roughly 18 months — "a boom without a parallel this century." Global data-center capex approaches $1 trillion in 2026 and $1.7 trillion by 2030, overwhelmingly U.S.-led. Crucially, the same American firms — Nvidia, the hyperscalers, SpaceX — are building both the terrestrial and emerging orbital compute layers, and the orbital versions depend on the falling launch costs only SpaceX supplies. The capital boom and the launch monopoly are one self-reinforcing flywheel — and SPCX sits at its center.

VI. Why China Cannot Be a Near-Term Space-Based Competitor

China is treated as America's one credible rival, but its balance sheet reveals an economy too fragile to sustain an open-ended, high-risk space build-out. Its condition is best described as "prolonged decay — the declining efficiency and effectiveness of policy tools."

Trapped capital on false collateral. Chinese households hold ~160 trillion yuan (~$22 trillion) in low-yield deposits, hoarded out of risk aversion to the point of a near "liquidity trap." That banking system is propped up by impaired assets — an estimated ~$10.5 trillion in deadweight losses spanning developer defaults, local-government-financing-vehicle write-downs, household wealth destruction, and property-collateralized corporate loans. The property downturn is in its fifth year, impairing household, developer, and local-government balance sheets at once.

A decaying financial system. New household lending rose just 0.5% year-over-year in January 2026 — an all-time low — while land-sale revenue fell ~15% in 2025 to under half its 2021 peak, forcing a 10-trillion-yuan debt swap. A system this strained cannot simultaneously absorb capital flight and bankroll a reusable-rocket and orbital-compute program from scratch.

The dollar off-ramp. U.S. policy now pulls that trapped capital westward. The GENIUS Act — signed by President Trump on July 18, 2025 — creates the first federal framework for dollar stablecoins, mandating 1:1 backing in dollars and Treasuries. Combined with exploding tokenization of gold and hard assets, it builds a frictionless, credible exit into dollar instruments that a capital-controlled command economy is structurally ill-equipped to police.

The irony. The Starlink connectivity backbone routing global access is owned by SpaceX — now a public, American capital-market-funded company. A nation cannot easily wall its citizens off from dollar-denominated digital assets when the connectivity layer itself is American-controlled and orbital.

Documented vs. projected. The documented present — ~$22T trapped, ~$10T impaired, collapsing lending, the GENIUS Act and tokenization as real dollar-demand engines — stands on its own. The forecast that these forces trigger accelerating capital flight and, by 2028, a destabilizing run on the command-and-control banking system is a reasoned projection. Even on the documented half alone, an economy this financially encumbered is hard to fathom as a near-term space-based competitor.

VII. Overriding Conclusion: SPCX Is a Massive Long-Term Buy

Every thread of this analysis converges on one investment conclusion. The United States is the structurally winning economy of the orbital age — it owns the only reusable launch infrastructure at scale, every high-value space sector must flow through it, its rivals face a capital burden it does not, the rest of the world will pay rent into its ecosystem, and its sole conceivable competitor is financially incapable of sustaining the race. SPCX is the single publicly traded asset that owns the chokepoint through which that winning economy must pass.

The investment case follows directly:

- Monopoly economics. SPCX controls the gateway — five of six U.S. launches — giving it pricing power over AI compute, telecom, mining, and defense lift for years before any rival can scale reusability.

- Multiple compounding revenue layers. Starlink (telecom), launch services, and emerging orbital data centers stack on top of one another, each dependent on the same lift advantage SpaceX alone possesses.

- A renewable capital engine. Now public and already trading at ~$2.17 trillion, SPCX can raise equity and debt repeatedly off a $2-trillion-plus base, with a tiny ~4% float leaving vast room for future raises — the "virtually unlimited funding" thesis validated in real time by a 23.18% first-day pop.

- A widening, not closing, moat. The U.S. capital boom and SpaceX's launch monopoly form a self-reinforcing flywheel, while China's financial decay and Europe's and Russia's structural lockout extend the runway.

The verdict: SPCX is not merely a stock in a strong company; it is the equity proxy for American economic supremacy in the highest-growth domain of the next half-century. For the long-term investor, that makes SPCX a massive buy.

The One Disciplined Caveat

China grew from 68 to 91 launches year-over-year and is testing reusable boosters; if it achieves reusability at scale, a second gateway opens. This does not break the thesis — it defines the monitoring metric. The American lead is a commanding head start to be compounded, and the window is real but finite. SPCX is a buy for those who hold through that window, not a trade.

Disclosure: This whitepaper is strategic and analytical, not personalized investment advice. The authors hold positions in securities mentioned and reserve the right to buy or sell shares at any time without notice. SPCX priced at $135 and trades at $166.29 (~$2.17T market cap) intraday on June 12, 2026. The raise is best stated as a range (~$75B base, ~$86B with greenshoe); the 2028 China bank-run timeline is a reasoned forecast, not documented fact. Position sizing should reflect your own risk tolerance and the China-reusability monitoring metric above.