1927 = 2026: The American Ascendancy Thesis

Thesis Update — The Track Holds Through May, But Stronger. The Supply Build Is Now Three-Sided.

The Update in One Line

Through May 2026, the 1927 overlay is holding month by month, but running hotter, because AI is a more powerful leadership engine than radio ever was, and because the United States has inverted the 1927 energy equation to become the world's largest producer and the marginal barrel that bends the entire geopolitical board. The new development since the last memo: the coming oil glut is no longer two-sided. It is three-sided — domestic Utica supply, U.S.-controlled Venezuelan supply, and the eventual Gulf-led Iran rebuild — all converging into structural oversupply.

I. The Monthly Track Is Holding Through May — But Stronger

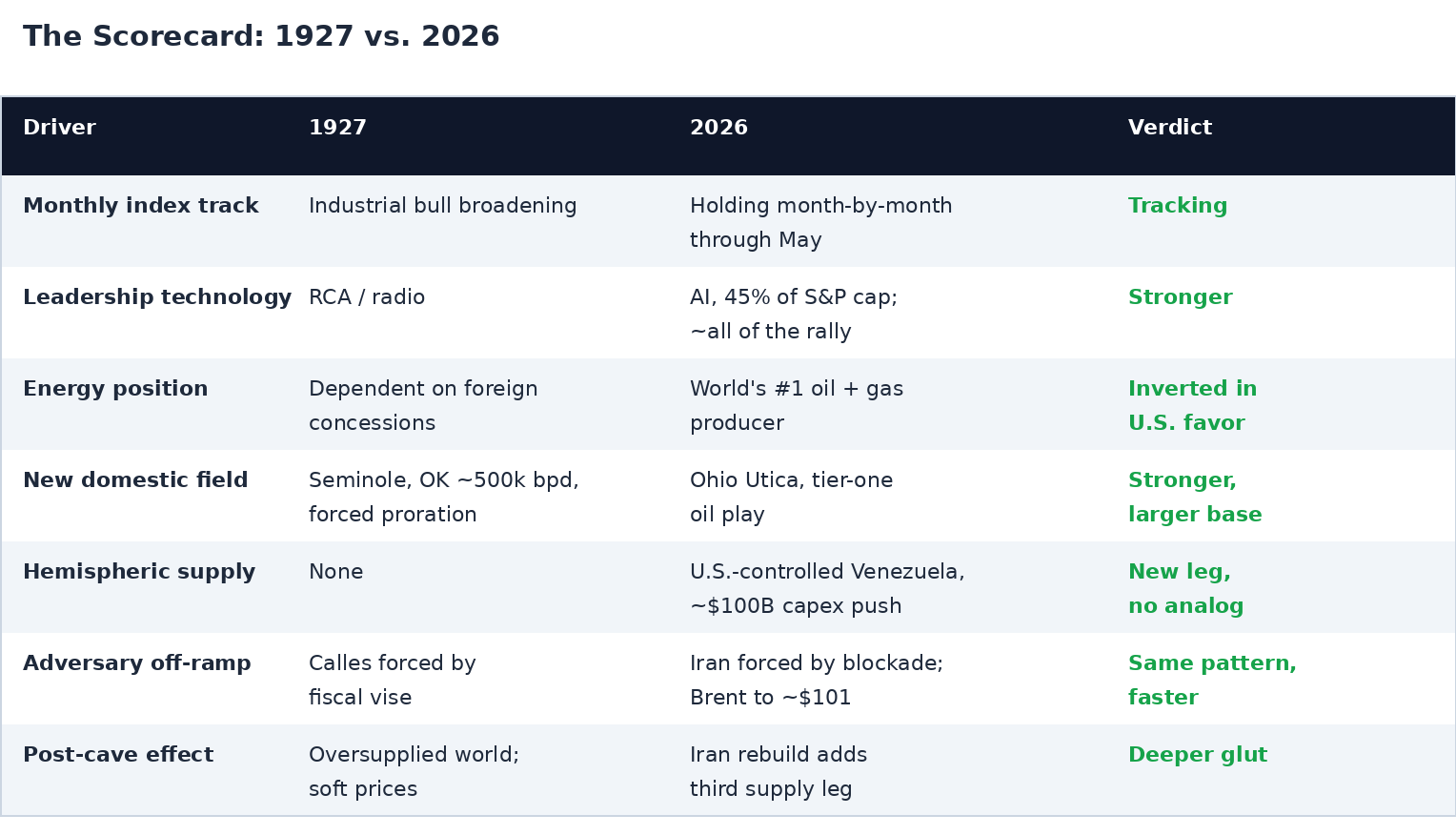

The directional, closing-price overlay of 2020–2026 onto 1921–1927 has stayed intact month by month into May, exactly as the prior memos said it would. The difference this cycle is magnitude, not direction: the S&P 500 is hitting fresh records, with the index near 7,100 by early May and a fourth straight year of gains underway. Where 1927 was carried by a broadening industrial bull, 2026 is carried by something more concentrated and more powerful — and that is the upgrade to the thesis.

II. AI Is the 2026 Accelerant — The New RCA, But Bigger

In 1927 the leadership engine was Radio Corporation of America; in 2026 it is AI, and the concentration is extraordinary:

- AI-linked stocks now account for a record 45% of the S&P 500's total market capitalization.

- Strip out AI and the ex-AI index has gone essentially nowhere since February — AI is driving virtually the entire rally.

- Over three years, the headline S&P 500 returned 76% versus just 32% for the ex-AI version.

- Year-end targets keep climbing on the AI trade — HSBC at 7,500.

This is the RCA dynamic of 1927–29 — one transformational technology pulling enormous capital into a single leadership cohort — but at a scale the radio boom never reached.

III. The Energy Equation Is Inverted in America's Favor

In 1927 the U.S. depended on foreign concessions (Mexico, Persia) to flow; in 2026 the U.S. is the dominant producer others must work around:

- The U.S. was the world's largest crude producer in 2025 at 13.58 million bpd, ahead of Russia (9.87) and Saudi Arabia (9.51).

- U.S. crude set an all-time record of 13.6 million bpd in 2025 and is expected to hold near record levels through 2026.

- The U.S. is also the largest gas producer and dominant LNG swing exporter, with North American LNG capacity on track to roughly double toward 28.7 Bcf/d by 2029.

IV. The Seminole–Utica Parallel: New Domestic Supply Crashing Price

The 1927 precedent is nearly exact. In late 1926, the rapid development of the large Seminole field in Oklahoma swung supply toward glut, with output of roughly 500,000 bpd driving prices down so hard it "threatened many firms" — forcing the first mandatory production controls in U.S. history with Oklahoma's compulsory proration order of August 9, 1927. The 2026 analog is the Ohio Utica, which has crossed from a gas play into a tier-one oil play, with EOG Resources elevating it alongside the Delaware Basin and Eagle Ford, and Ohio crude at a record 151,000 bpd — triple its mid-2021 level. In both periods, a major new American field arrives in the same window as a foreign resource off-ramp — but in 2026 the U.S. supply base is an order of magnitude larger.

V. The New Supply Leg: U.S. Virtual Control of Venezuela

This is the piece that did not exist in any prior cycle. Following U.S. special forces' capture of Maduro on January 3, 2026, the administration took effective control of Venezuela's oil sector and is leading a multi-year capital-spending drive to dramatically rebuild capacity:

- Trump has called for at least $100 billion in oil-industry investment, with U.S. firms financing reconstruction and recovering it from production.

- The EIA projects Venezuelan output can climb 30%–40% in 2026 — roughly 300,000–400,000 bpd — with production already back near 1 million bpd.

- Exports hit a fresh seven-year high in May, with output targeting ~1.3 million bpd in 2026, the single biggest contributor to global supply growth this year.

- Restoring Venezuela toward prior levels implies a multi-year capex boom that builds a durable new supply leg well beyond 2026.

This is a U.S.-directed capacity expansion in the Western Hemisphere with no 1920s equivalent — it adds directly and durably to the oversupply.

VI. The Iran Rebuild: The Third Supply Leg, Triggered by the Cave

When Iran caves, the second-order effect compounds the glut rather than relieving it. A negotiated end — the U.S. has already delivered a 15-point plan to Tehran — opens the door to a massive U.S.- and Gulf-led reconstruction of Iranian energy infrastructure aimed at restoring Iran to its old production highs and beyond. The blockade has cut Iranian exports to under one-sixth of pre-war levels, and the eventual rebuild brings those barrels back and expands capacity, layering a third supply wave on top of Utica and Venezuela. The off-ramp does not tighten the market — it floods it.

VII. Timing: October Is the Aggressive Case

The structural setup was bearish before the war — OPEC+ unwinding, a projected 3–4 million bpd surplus, U.S. and South American supply surging — so the war spike is a deviation on top of a market built to fall. The proof is already printing: on May 6, Brent dropped ~8% to ~$101 as Iran signaled it was weighing the U.S. proposal to end the conflict. With the blockade costing Iran roughly $6 billion and forcing a Calles-style economic off-ramp, October stands as the aggressive case for resolution and the drastic price break; year-end 2026 is the base case. Either way, the combination of domestic, Venezuelan, and Iran-rebuild supply points to an oversupplied world mirroring the post-Seminole, post-Mexican-crisis glut of 1927–28.

VIII. The Scorecard: 1927 vs. 2026

The Continuing Thesis

The 1921 = 2020 overlay has carried to the 1927 = 2026 waypoint month by month through May — but stronger, because AI is a more concentrated and powerful engine than radio, and because America has inverted the energy equation to become the world's largest producer and the marginal barrel that bends the board. The supply build is now three-sided: the Utica at home (the Seminole of this cycle), U.S.-controlled Venezuela rebuilding capacity over several years, and the coming Gulf-led Iran reconstruction once Tehran caves — all converging into structural oversupply. October is the aggressive case for the Iran resolution and the drastic price break; year-end is the base case. The track holds. The differences are all to the upside. We told you. It continues.

Disclosure: This memorandum is provided for informational and discussion purposes only and does not constitute investment advice, a recommendation, or an offer or solicitation to buy or sell any security. The author holds positions in securities mentioned and reserves the right to buy or sell at any time without notice. Historical analogies are illustrative and not predictive. Forward-looking statements involve risk and uncertainty; actual outcomes may differ materially.