Turning Overbuild Into Advantage

How Owned Distribution Lets a Hyperscaler Retrench Into an Apple-Style Moat

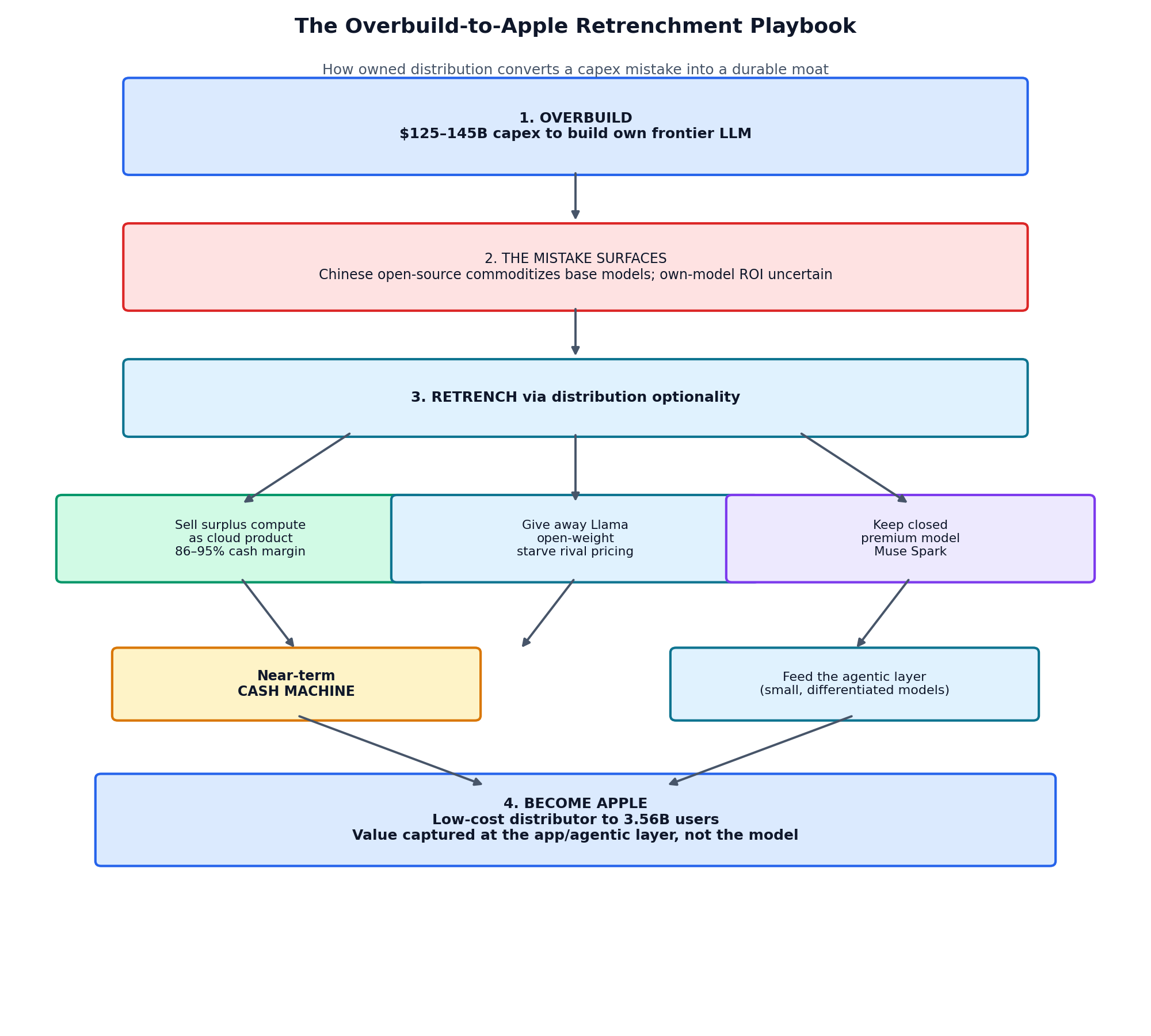

Meta’s July 2026 pivot into a cloud-compute business — “Meta Compute” — is not an ordinary infrastructure announcement. It is a case study in a repeatable corporate playbook: overbuild → retrench → monetize → distribute. A company that overspends to build its own frontier model can, if it owns consumer distribution, convert that apparent capex mistake into a near-term cash machine and then relocate value to the layer that does not commoditize — the application and agentic surface sitting on top of billions of users. As Chinese and open-weight competitors commoditize base models, the durable winners resemble Apple: low-cost, high-distribution integrators of differentiated, small-model agentic AI rather than sellers of the models themselves.

1. The Setup: A Justifiable Overbuild

The hyperscaler class committed roughly $600B+ in 2026 AI capex, with Meta alone guiding to ~$125–145B. Meta built this capacity to train and serve its own frontier models, betting that model leadership would be the prize. Two forces then destabilized that premise. First, base-model commoditization: open-weight releases — increasingly from Chinese labs — drove the marginal price of a “good enough” model toward zero, eroding any durable edge from owning the best model. Second, uncertain internal ROI: when the highest-value node of a value chain migrates, capex sunk into the former prize looks stranded — the classic “wrong node” risk of overbuilding a commoditizing layer.

2. Why Distribution Creates Optionality

The central claim of this paper is that owned distribution converts an overbuild from a write-down into an option. A firm without distribution must sell surplus capacity into a spot market at whatever price clears. A firm that owns 3.56 billion daily users can instead choose: consume the compute internally, sell the surplus, or feed it into owned applications. That optionality lets management exit a strategic error without stranding the asset, because the asset has multiple exits.

3. Step One — The Near-Term Cash Machine

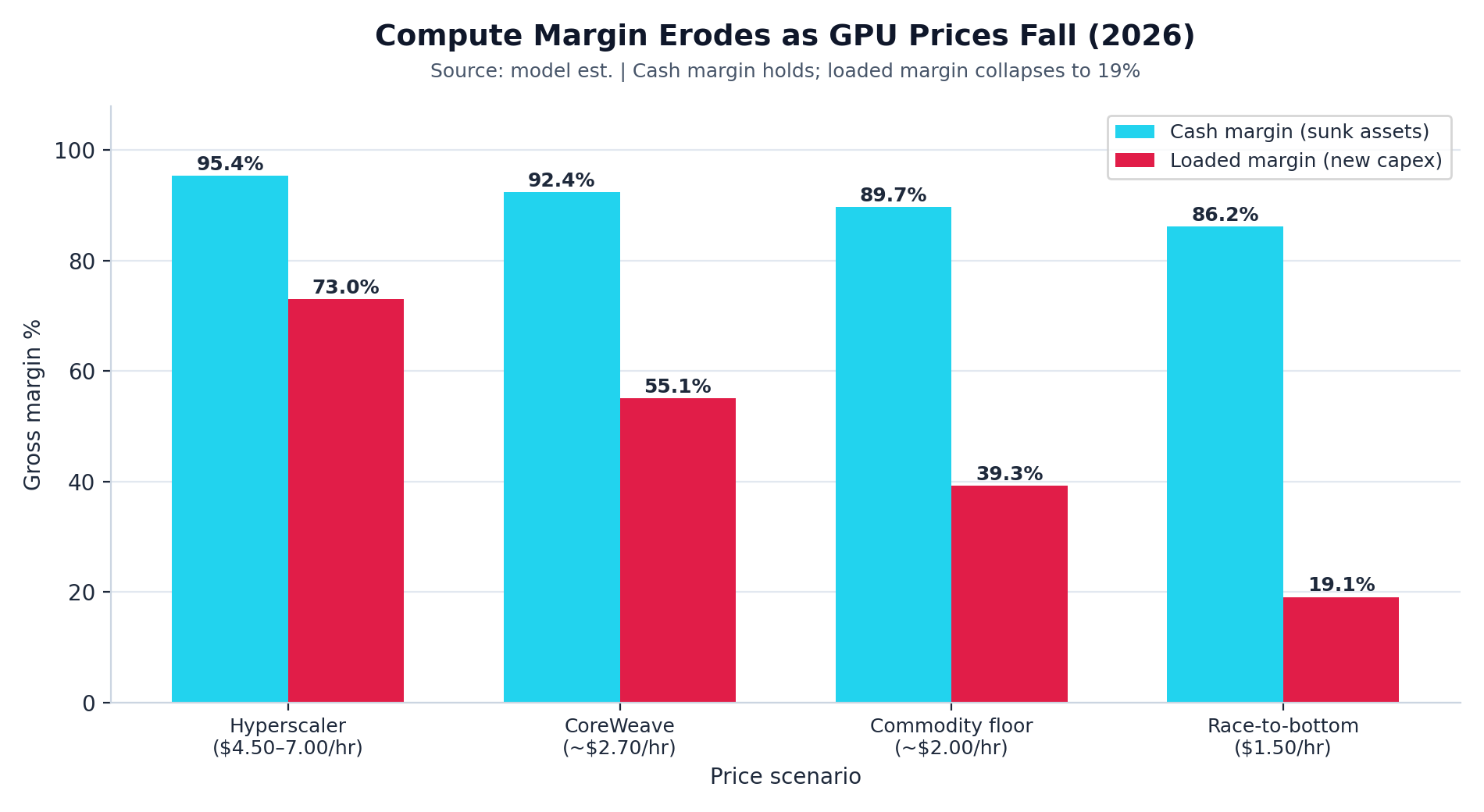

Because the data-center capex is already sunk, selling surplus GPU-hours is highly profitable on a cash basis, mirroring how SpaceX/xAI monetized excess compute. The key distinction is between cash margin and fully-loaded margin. On a cash basis — treating the hardware as already paid for — incremental margin exceeds 86% even in a race-to-bottom $1.50/hr pricing scenario, since the marginal cash cost is only ~$0.21 per GPU-hour. On a fully-loaded basis, however, margin collapses from 73% at AWS/Azure’s ~$4.50–7.00/hr rates toward 19% at the commodity floor, as the cost of new silicon gets allocated in. As pricing power erodes and capacity floods the market, those two lines converge downward.

The strategic reading is simple: compute is a cash machine, not a fortress. It funds the transition but will itself commoditize as capacity floods in. It is a bridge, not a destination.

4. Step Two — Relocating Value to the Distribution Layer

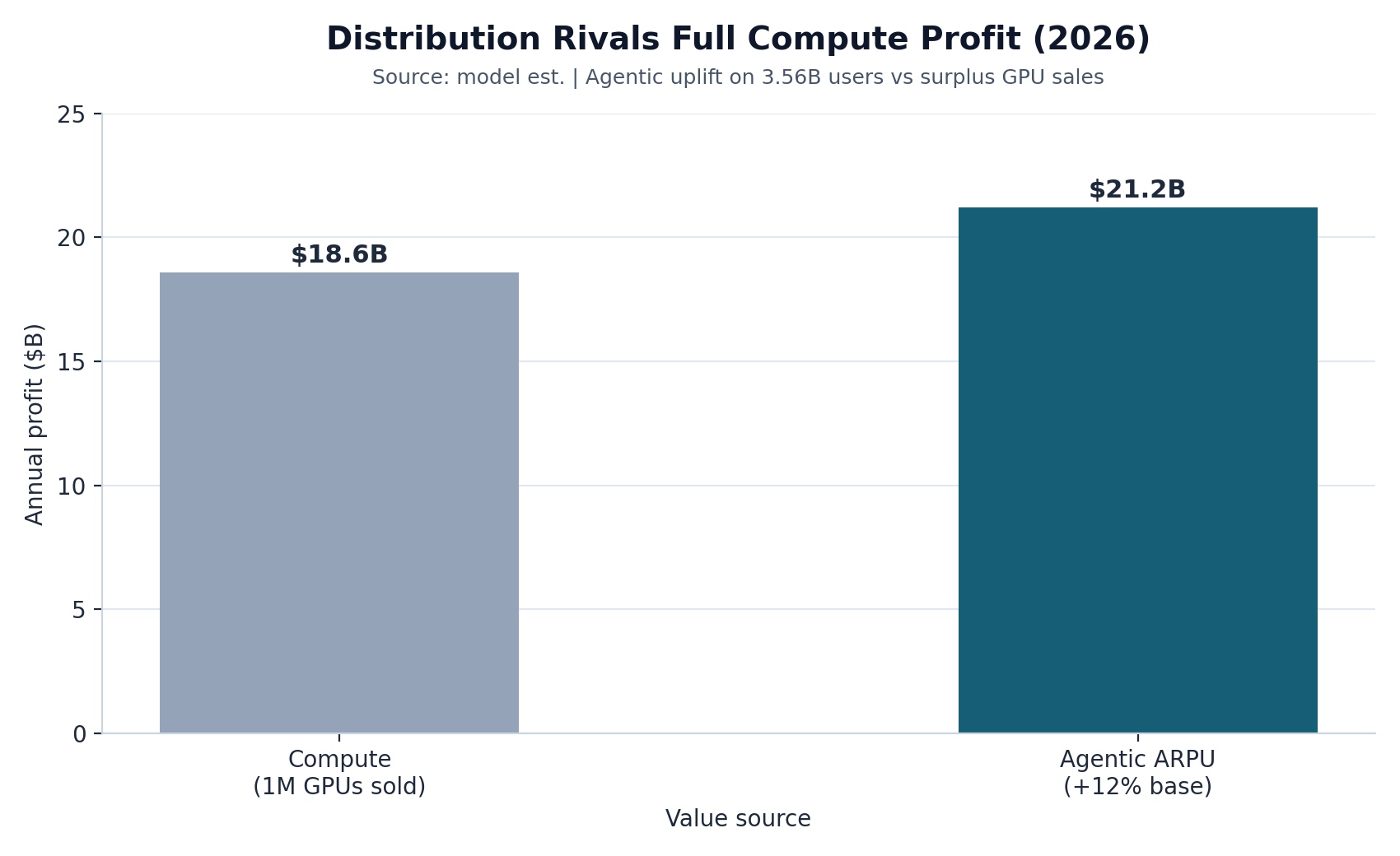

The durable return lives one layer up. Modeling an agentic ARPU uplift on Meta’s user base illustrates why the distribution layer is the actual prize. A base-case +12% agentic ARPU uplift adds approximately $21.2B on 3.56 billion users — roughly equivalent to the cash gross profit from selling one million surplus GPUs (~$18.6B), but at advertising-business margins with no new silicon required. And critically, ARPU is already compounding (~$44.63 → ~$53.21, +19%), so the agentic layer builds on an appreciating base, not a commoditizing one.

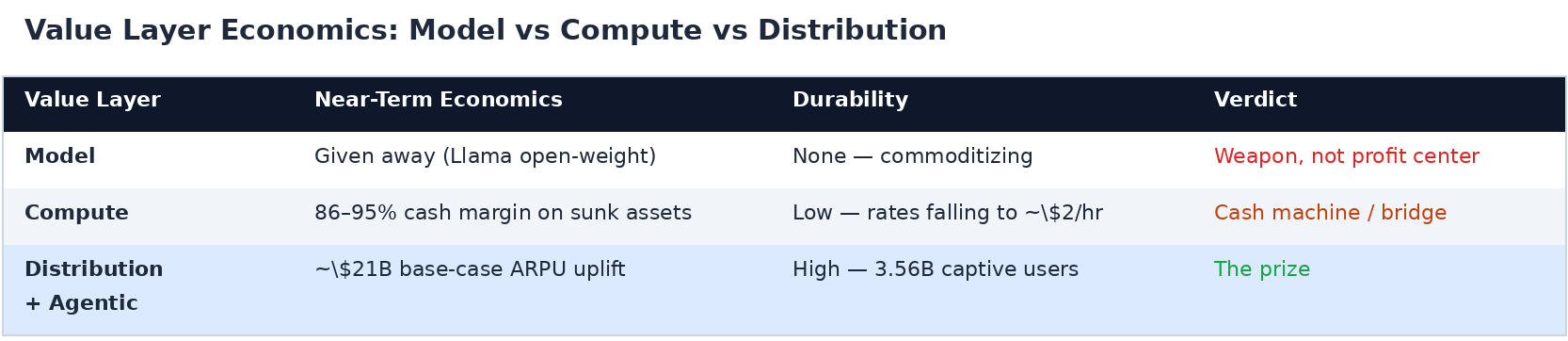

Put the three layers side by side and the verdict is clear.

The model is a weapon, not a profit center. Compute is a cash machine and a bridge. Distribution plus the agentic layer is the prize.

5. The Apple Analogy: Low-Cost Distributor of Differentiated AI

Apple rarely owns the most advanced component, but it owns the customer and integrates components into a differentiated, distributed experience. The thesis that AI winners may not be the ones providing the best models but rather the ones who own the users maps directly onto what Meta is attempting. The winning configuration in this framework is small, efficient models deployable at the edge and cheaply served — not frontier-scale models whose economics are being competed away — bundled into owned surfaces where switching costs and distribution decide winners. Meta and Apple both reach billions of users directly, distributing agentic experiences at a marginal cost no challenger can match. That is the moat.

This framing actually puts Meta in a stronger structural position than Google. Google is locked into Gemini — it has bet its AI identity on owning and winning the frontier model race, which means it must keep winning that race forever to justify its position. If open-weight models continue commoditizing the intelligence layer, Google's core asset depreciates. Meta, by contrast, has already made peace with not owning the best model: it gives Llama away as a competitive weapon while keeping a closed premium tier (Muse Spark) for high-value use cases, and treats the underlying intelligence as a swappable input. That is exactly the Apple posture — and it is more durable than Google's, because it does not require Meta to win an arms race it cannot control.

The broader winner's circle in this framework includes all three distribution owners — Apple, Meta, and Google — each holding a different chokepoint on the consumer. The losers are the frontier model makers: OpenAI and its brethren. As open-weight models drive the marginal price of intelligence toward zero, the companies whose entire value proposition is selling that intelligence find themselves on the wrong side of commoditization. The gains of the distribution layer come directly at the expense of the model layer — and OpenAI, with no comparable distribution surface of its own, is the most exposed.

6. Risks to the Thesis

Three risks deserve honest acknowledgment. First, the compute-as-fortress fallacy: the 86–95% cash margins that make Meta Compute attractive are precisely what attract capacity and drive rates toward the floor. What looks like a durable business is a bridge. Second, distribution dependence: with the model given away and compute commoditizing, nearly all durable value rests on the distribution and agentic layer and the closed premium model (Muse Spark). If either is disrupted or eroded, there is no fallback profit center. Third, regulatory and channel risk: owning 3.56 billion users invites antitrust scrutiny that could constrain the very bundling mechanism that captures agentic value.

7. Conclusion

Meta's move illustrates a durable lesson: owned distribution is the ultimate hedge against a strategic overbuild. It lets a company retrench from a model-ownership mistake, harvest sunk compute as a near-term cash machine, and relocate to the non-commoditizing layer — becoming, like Apple, a low-cost distributor of differentiated, small-model agentic AI as basic models are commoditized by open-source and Chinese competitors. The compute cash machine funds the journey. The 3.56-billion-user distribution surface is the destination.

In the end, this is a story with three winners and a clear set of losers. Apple, Meta, and Google each own the consumer through different surfaces and will capture the agentic value layer as it matures. The bill is paid by OpenAI and the other frontier LLM players — the companies that built the miracle but do not own the door it walks through.

Prepared July 1, 2026. Financial figures are modeled estimates based on public reporting and market pricing data. This document is for strategic discussion only and does not constitute investment advice.