How Chokepoints Eat Revolutions

A 150-Year Pattern of Productivity Surges and Why Apple Wins the Agentic Age

Roughly once a generation, a technology delivers a leap in productivity so large that users would rationally pay far more than they are charged. History is remarkably consistent on who captures that surplus. Not the inventor. Not the component maker. Whoever controls the chokepoint between the new productivity and the consumer.

The pattern runs the same way each time. A breakthrough makes something radically cheaper or more capable. Demand for the underlying input explodes. Then the component layer floods with competitors, margins collapse, and value migrates to the one link that is consolidated and unbypassable — the chokepoint that holds the spread between its falling cost and the price the consumer will bear. Across 150 years this has played out from Standard Oil to the automobile to Intel, and it is now landing on agentic AI. The answer to who captures the surplus this time is Apple, eventually sharing the position with Google.

“Own the gate to the consumer, and the productivity surge pays you — not the inventor.”

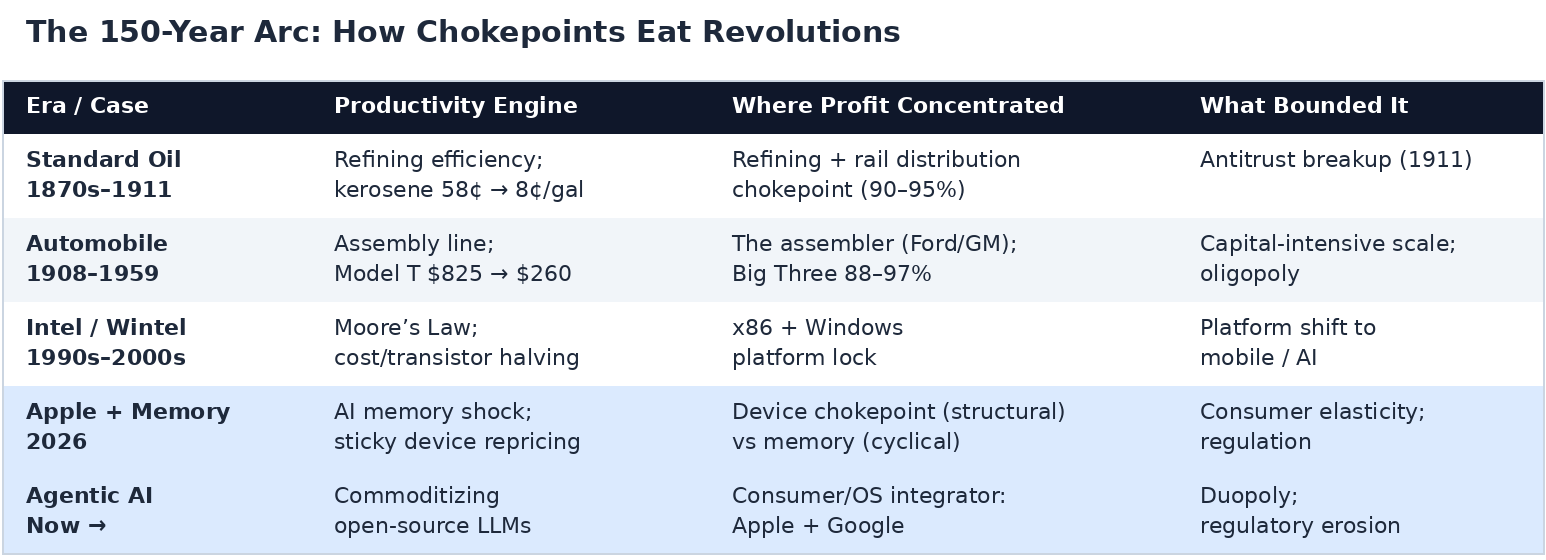

Oil, Cars, and Chips: The Pattern Runs Three Times Before Silicon Valley Is Born

Standard Oil is the clearest first proof. Refining innovation and scale drove kerosene from 58 cents to 8 cents a gallon — an extraordinary gift to households. Yet Rockefeller grew richer as his product got cheaper, because Standard controlled 90–95% of US refining plus the rail distribution that reached the consumer. Its genius was invisible surplus capture: consumer prices fell, costs fell faster, and Standard pocketed the widening spread no rival could match. The 1911 antitrust breakup ironically tripled Rockefeller’s wealth. That alone tells you how durable a true chokepoint is — even the government couldn’t destroy the economics, only redistribute the equity.

The automobile tells the same story, and it is the most direct template for AI. Early entry was trivial — buy parts on credit, sell the car for cash — and hundreds of assemblers bloomed once patents stopped gating the field. Ford’s assembly line cut the Model T from $825 to $260, and value concentrated violently. The Dodge Brothers began as Ford suppliers; the component makers got competed away. The assembler captured the rent. By 1959 the Big Three commanded 97% of the US market and GM was running roughly 25% margins. When the engine commoditized, durable profit did not stay there — it migrated to whoever assembled the thing the consumer had to buy.

Intel’s rise and fall completes the pattern and adds the crucial warning. Intel banked Moore’s Law inside the Wintel lock, holding premium pricing as cost-per-transistor collapsed. Its chokepoint was impregnable inside the PC platform — and perfectly defenseless when the platform shifted to mobile and AI. This is the error that decides the Apple-versus-Google endgame today: owning a strong position inside someone else’s platform is not the same as owning the platform.

Apple and the Memory Shock: The Pattern, Live

The 2026 memory cycle is the pattern running in real time. AI made memory scarce almost overnight — Micron posted an 84.6% gross margin on revenue that grew 346%; Samsung briefly outearned Apple. Facing a roughly 15% component-cost rise, Apple raised MacBook and iPad prices 13–25% under an “unavoidable cost” narrative, and simultaneously lobbied to source memory from blacklisted Chinese maker CXMT — a heads-I-win positioning only Apple’s volume and political weight enables. Either outcome converts a temporary upstream cost shock into a permanent downstream price reset, because device prices are sticky and never fall when memory normalizes.

This is the chokepoint dynamic made explicit: memory’s windfall is cyclical. Apple’s position is structural. Memory wins 2026; Apple wins the war.

Why Agentic AI Lands on Apple — and How This One Ends

Agentic AI — software that acts across your apps and data autonomously — is the once-a-generation product, and its engine is commoditizing faster than any prior technology revolution. Chinese open-source models (DeepSeek, Qwen, Kimi K2) now match or beat top closed models; roughly 80% of the world’s open-source AI developers build on them; analysts expect approximately 90% of the intelligence spectrum to commoditize within a few years. This is the Selden patent breaking again — the engine becoming free, which means value flows to the integrator who owns the consumer.

That integrator is Apple, with ~96% iPhone loyalty and 64% of global app spend flowing through ~30% of devices. At WWDC 2026, Apple declined the frontier-model arms race entirely and refortified the OS-level agentic layer instead. The message was deliberate: Apple does not need to build the miracle. It needs to own the door the miracle walks through.

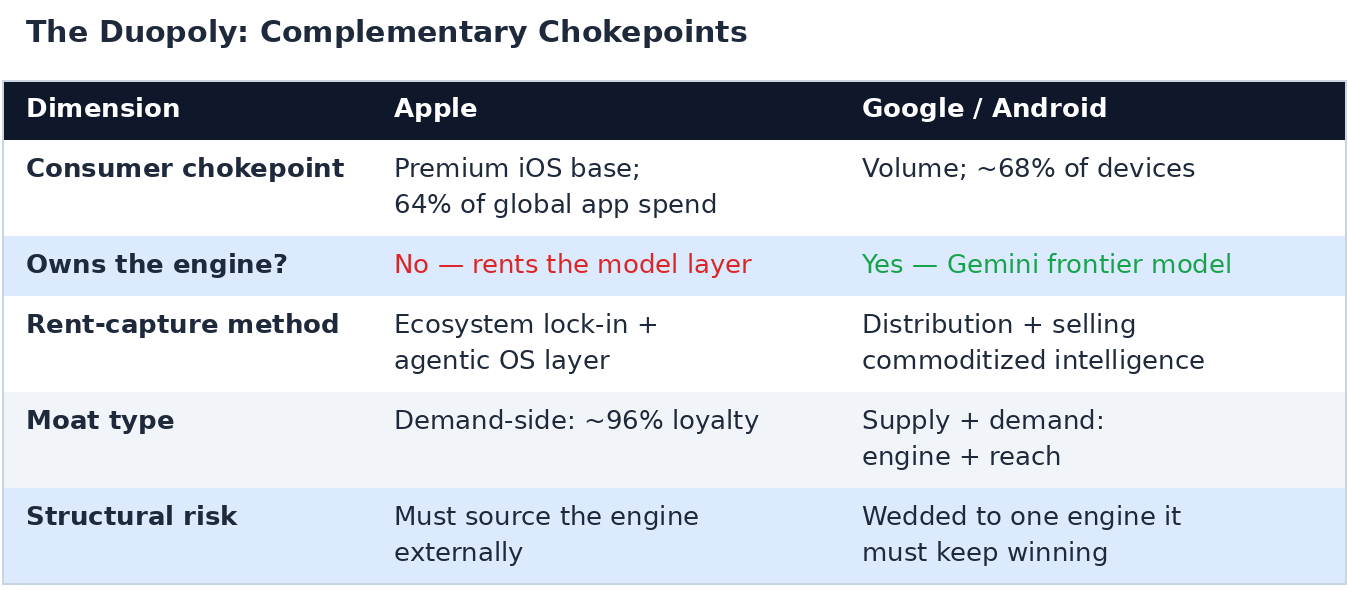

The Duopoly — and the Decisive Asymmetry

No prior productivity surge ended as a monopoly. Each consolidated into a small oligopoly — the auto Big Three, the smartphone duopoly. This one ends the same way, with Apple and Google occupying complementary chokepoints. The losers are the model and component makers, whose layer becomes a free, substitutable input.

The decisive asymmetry is this: Google made the Intel mistake in advance. It is wedded to its own engine — Gemini — and must keep winning the frontier race forever to justify its position. Apple, by owning the consumer and treating the model layer as a swappable commodity, can do what no prior integrator could: acquire the eventual winner of integrated agentic AI and bolt it directly onto the gate it already owns. Standard Oil owned the distribution. Ford owned production as the engine commoditized. Intel proved platform-position beats component-position. Apple has internalized all three lessons simultaneously — it lets a thousand engine-makers bleed to commodity prices, then purchases the survivor.

Google wins too, but Google is Intel-with-a-platform, betting its position on one engine it must never stop winning. The productivity surplus from agentic AI will be enormous. As it has been for 150 years, that surplus will not flow to whoever built the miracle. It will flow to whoever owns the door.

This brief synthesizes publicly reported information and historical analysis for strategic discussion. It is not investment advice and contains forward-looking interpretations that may prove incorrect. Sources: Standard Oil refining share and kerosene pricing (Britannica, FEE, Cato); Ford assembly-line cost reduction and Big Three concentration (Ford Motor Co., EBSCO); Intel/Wintel platform lock and decline (Rumelt, “Intel’s Fall From Grace”); 2026 memory cycle (Yahoo Finance, WSJ, Reuters); Apple CXMT lobbying (Financial Times, AppleInsider, The Verge); open-source LLM commoditization (Asia Society, Stanford); Apple moat and loyalty data (Asymco, Wedbush, Washington Post).