Apple Inc. (AAPL) — The Indispensable Toll

Why Wall Street Has the Memory Story Exactly Backwards and Why Apple Is the Screaming Big-Cap Buy of the AI Era

By JD Unfiltered | June 27, 2026

Last Price ~$284 | Street Median Target $293–$315

RATING: STRONG BUY — 12-Mo Base $400 (+41%) | Bull $442 (+56%) | 5-Yr $664–$734

Executive Summary

Every analyst, TV commentator, and economist hand-wringing over "higher memory costs hurting Apple" has the story upside down. The AI-driven memory squeeze is the most bullish development in Apple's history, because the same AI boom raising chip prices is making the iPhone and its hardware brethren more indispensable than ever. You do not penalize the toll booth when traffic explodes — you raise the toll. Critically, Apple's earnings power is accelerating — not decelerating — as free AI users convert to paid subscriptions that flow through Apple's highest-margin channel. The market has this exactly backwards. We rate AAPL a STRONG BUY.

"The market is still multiplying Apple's earnings like a hardware maker. We multiply them like the highest-margin toll booth in the AI economy — and the toll traffic is accelerating."

1. Why the Consensus Is Wrong

The bears are fighting the last war. When Tim Cook flagged "significantly higher memory costs," the commentariat reflexively coded it negative — missing the second-order effect. The AI boom driving memory prices up is driving the value of the device the memory sits inside up by orders of magnitude more. Proof is in the financials: Q2 FY2026 delivered a March-quarter record $111.2B revenue (+17% YoY), gross margin at a multi-year-high 49.3%, record Services, and iPhone revenue up 22%. This is margin expansion into the supposed headwind — and it is accelerating.

2. The Indispensable Toll: Pick-and-Shovel of the AI Race

In a gold rush you buy the picks and shovels. In the AI race, the "shovel" is the device in 1.4 billion hands that the AI must run on. While Amazon, Microsoft, Meta and Alphabet collectively plan ~$650B in 2026 AI capex, Apple plans ~$14B — outsourcing the models while keeping the customer, the device, and the margin. Apple is on track to clear $1B in AI revenue this year (including ~$900M from generative-AI apps via the App Store) without bearing the infrastructure cost crushing its peers. It collects the toll while others build the road.

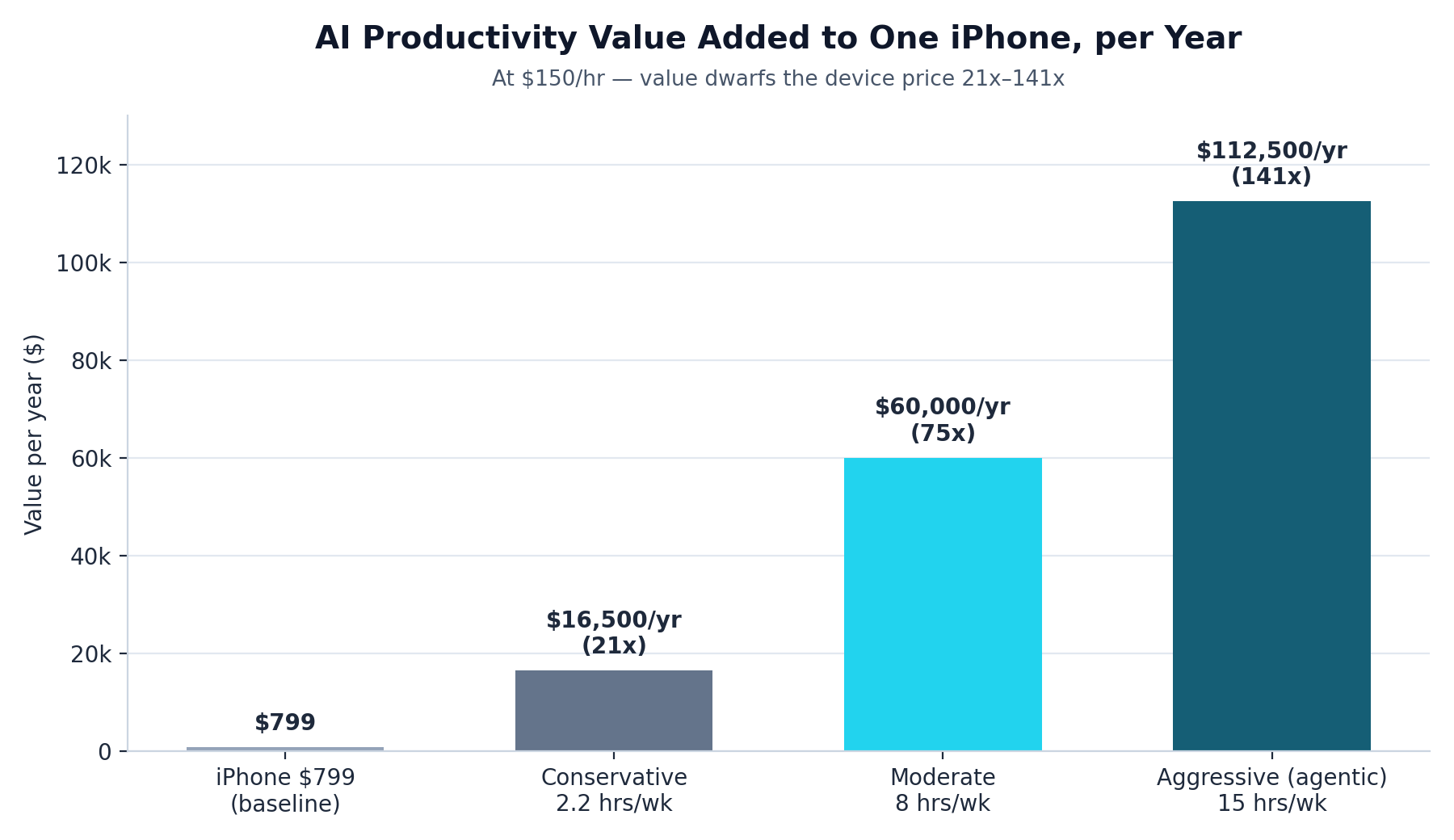

3. The Value Engine: 21x–141x the Price, Every Year

The iPhone is no longer a phone; it is a productivity terminal whose annual value to the user dwarfs its price. At a $150/hour professional rate, agentic AI access delivers $16,500/yr (conservative, ~21x the $799 price), $60,000/yr (moderate headline, ~75x), and $112,500/yr (aggressive/agentic, ~141x). When a device returns 21x–141x its price every year, demand goes inelastic — exactly what the data shows (iPhone elasticity ~ -0.08 to -0.8). Apple has historically raised prices 10–60% with no adverse sales effect.

Exhibit 1 — AI productivity value added to one iPhone per year, at a $150/hr advisory rate.

4. Price Is Sub-Inflationary; Value Dwarfs It

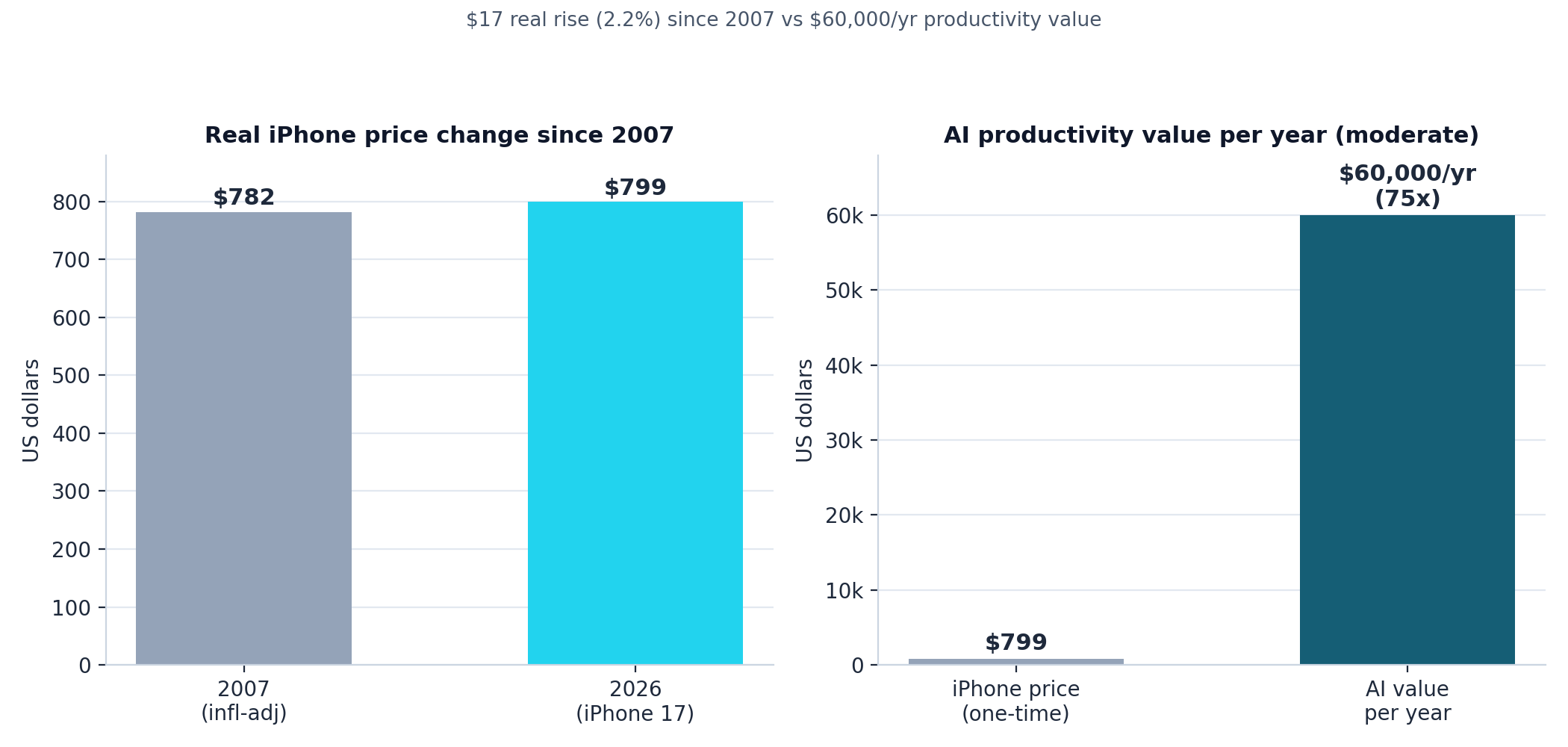

Adjusted for inflation, the original 2007 iPhone cost ~$782 in today's dollars; the iPhone 17 starts at $799 — a real increase of just $17 (2.2%) over 19 years. Against ~$60,000/yr of productivity value, any memory-driven price bump is a fraction of a percent of value gained. The "price increase" is not inflation; it is a negligible toll on a vastly larger productivity return.

Exhibit 2 — Sub-inflationary price (left) vs. annual AI productivity value (right).

5. The Margin & Profit Upside Nobody Is Modeling

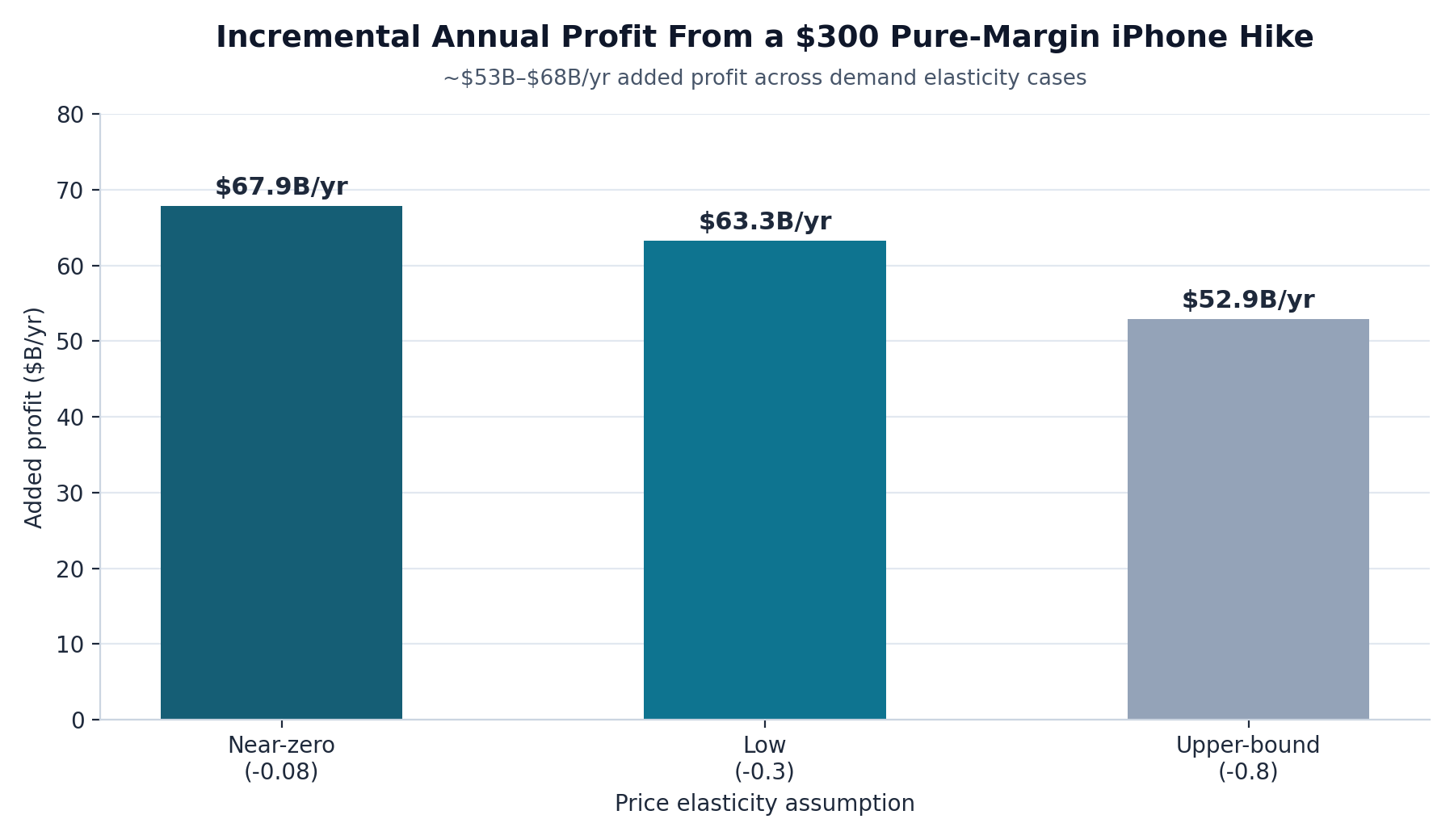

Should Apple take a $300 pure-margin increase above the memory-cost offset, incremental profit on ~232M units/yr ranges ~$53B–$68B/yr across documented demand elasticity. To a buyer capturing $60,000/yr in AI value, a $300 hike is a 0.5% toll — economically invisible, which is why volume barely moves. Crucially, the AI value lands in Apple's highest-margin channel: Services run at ~75% gross margin vs ~36% for products. As agentic productivity migrates onto the device — and users increasingly prefer running agents on mobility over a laptop — that value is taxed at Services rates, dragging blended margin structurally upward. This is why BofA sees earnings potentially doubling over five years.

Exhibit 3 — Incremental annual profit from a $300 pure-margin iPhone hike: ~$53B–$68B/yr.

6. Valuation: The Re-Rating the Bears Are Positioned Wrong For

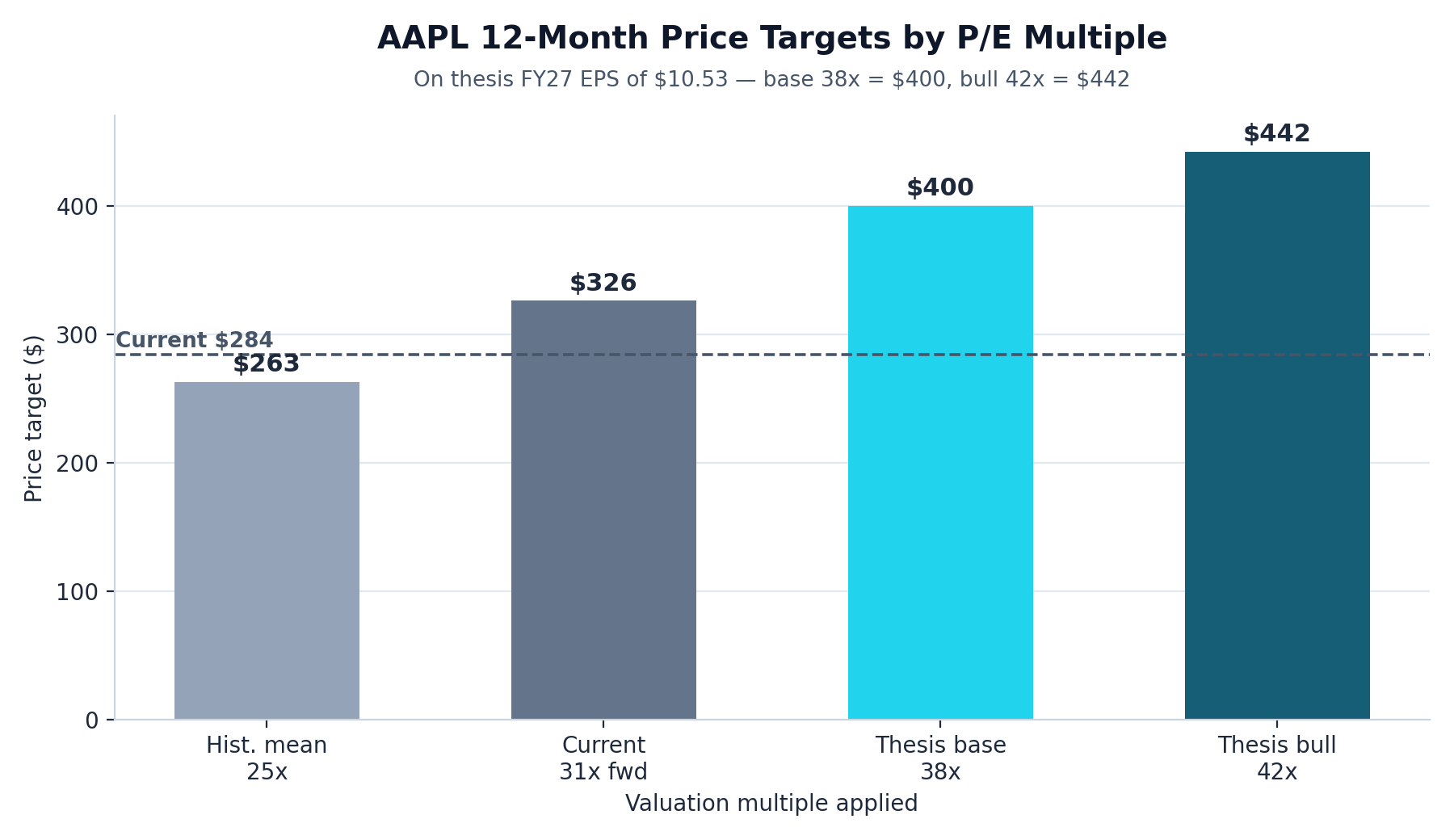

Apple trades near ~31x forward P/E vs a ~25x 10-year mean. Our thesis supports a 38x base / 42x bull multiple on a thesis FY2027 EPS of ~$10.53 (10% above the $9.57 consensus): 25x = $263 (-7%); 31x = $326 (+15%); 38x base = $400 (+41%); 42x bull = $442 (+56%). 5-Year case: a doubling of FY26's $8.74 EPS implies ~$17.48 by FY30-31. At 38x that is ~$664 (+134%); at 42x, ~$734 (+159%). Even compressing to ~31x on doubled earnings yields ~$542 (+91%) — the thesis works even if the re-rating never happens.

Exhibit 4 — 12-month price targets by multiple on thesis FY27 EPS of $10.53.

7. Why It Could Go Even Higher: The Great Valuation Cession

Our targets may prove conservative. Today the AI market cap is concentrated in the pure large-language-model companies and the chip manufacturers that supply the compute. But value ultimately accrues to whoever delivers the productivity to the end user — not to the layer that merely produces the raw intelligence or the silicon. As agentic AI matures and models commoditize, we expect a structural cession of valuation from the LLM labs and chip makers toward the final product that puts that productivity in the user's hand. Apple owns that final product, the distribution, and the billing relationship.

"The picks and shovels get repriced once the gold is in someone's hand. We expect market cap to migrate from the model labs and chip foundries to the indispensable toll the productivity flows through — Apple."

In that re-rating, a 42x multiple is not a ceiling but a way-station: if Apple is recognized as the consumer-productivity monopoly of the AI age, multiple and earnings expand together, and the five-year figures above become a floor, not a target.

8. The Accelerant: Free-to-Paid Conversion Is Inflecting Now

The single most underappreciated driver of Apple's earnings acceleration is the migration from free to paid AI. Free models are adequate for low-risk personal tasks, but for work, sensitive data, and frontier capability, paid tiers win decisively on advanced reasoning, speed, file/vision tools, and — critically for professionals — data privacy, since most free tools may train on user inputs. Users are voting with their wallets: 35% of workers already pay out of pocket for AI tools their employer won't provide, and over 90% use personal AI tools regardless of corporate policy. The funnel is filling from the bottom up.

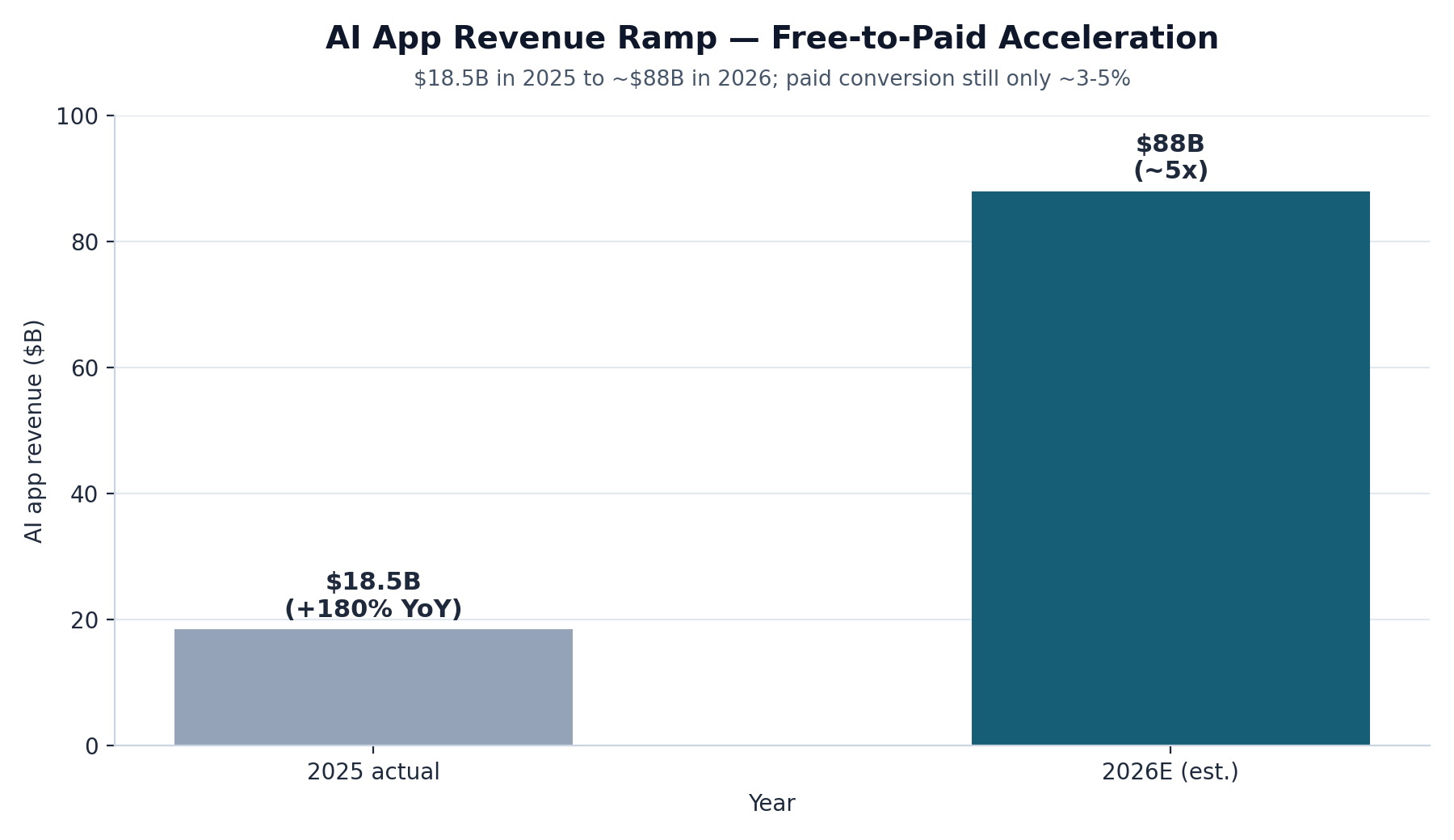

The revenue ramp is explosive. The AI app sector generated $18.5B in 2025 (+180% YoY) and is tracking toward ~$88B by end of 2026 — a near-5x jump in a single year, the fastest-growing app niche on record. Yet paid conversion remains in the low single digits (~3-5% of 1.1B+ AI app users), against US adult AI adoption of ~56-61% and a ~24% global diffusion rate. This is the tell: penetration of users is already enormous and compounding, while penetration of paying users is tiny. As that gap closes, the fastest-growing layer of AI monetization flows straight through Apple's App Store toll into its ~75%-margin Services line. The market is modeling a memory headwind; it is missing an accelerating, high-margin annuity.

Exhibit 5 — AI app revenue ramp $18.5B (2025) to ~$88B (2026E); paid conversion still only ~3-5%.

"Apple's earnings are not decelerating into the memory cost — they are accelerating into the free-to-paid conversion wave. Wall Street has totally misjudged the direction."

AUTHOR HEDGE & DISCLOSURE — READ BEFORE RELYING ON THIS DOCUMENT.

This report is published by JD Unfiltered Research for informational and educational purposes only. It is NOT investment advice, not a recommendation, solicitation, or offer to buy or sell any security, and is not a personalized recommendation for any individual. The author and/or affiliated entities may hold, and may at any time buy or sell, positions in Apple Inc. (AAPL) and related securities, and therefore have a potential conflict of interest. The author has not been compensated by Apple Inc. for this report. All price targets, EPS estimates, productivity-value figures, the $300 margin scenario, elasticity assumptions, adoption/penetration figures, and the "valuation cession" thesis are illustrative models and forward-looking opinions, not facts or guarantees, and rest on assumptions that may prove materially incorrect. Forward-looking statements involve significant risks and uncertainties — including AI adoption and paid-conversion rates, competitive dynamics, regulatory and antitrust action, supply-chain and memory-cost volatility, macroeconomic conditions, and changes in consumer demand — and actual results may differ materially. Past performance and historical multiples do not predict future results. Third-party data (consensus estimates, analyst targets, financial and adoption figures) is believed reliable but has not been independently verified. Readers must conduct their own due diligence and consult a licensed financial, tax, and legal advisor before investing. The author and JD Unfiltered Research disclaim any liability for losses arising from use of this document. By reading you accept these terms. © 2026 JD Unfiltered Research. For external distribution.