AmpliTech Group (AMPG) — The Only American Radio

Why the Memory-Cost Panic Misses a US-Made Sole-Source Riding the Fastest Infrastructure Buildout of the Decade

Last Price ~$6.98 | Market Cap ~$179M | NASDAQ: AMPG

RATING: STRONG BUY (Speculative) — Thesis: Sole-US-source x Buy-American law x AI-forced 5G SA acceleration

Executive Summary

The market has tarred AmpliTech with the same brush it wrongly used on Apple: a knee-jerk fear that rising component and memory costs will crush margins. This is exactly backwards. AMPG is the only American company designing and commercializing a carrier-grade O-RAN Massive MIMO radio at its specification level — and it sells into customers (cellular carriers, satellite operators, defense, quantum) who cannot simply shop elsewhere when US sourcing is legally favored or mandated. Like Apple, AMPG holds pricing power: when your product is indispensable and the buyer is funded by federal Buy-American dollars, you pass cost through and protect margin. The same AI-productivity wave forcing paid demand through Apple devices is forcing the 5G Standalone buildout that AMPG’s hardware enables — and it is happening fast. We rate AMPG a STRONG BUY for risk-tolerant capital.

“The market is pricing AMPG like a cost victim. We price it like the only American toll booth on a federally-funded, AI-accelerated road.”

1. The Memory-Cost Panic Is Exactly Backwards

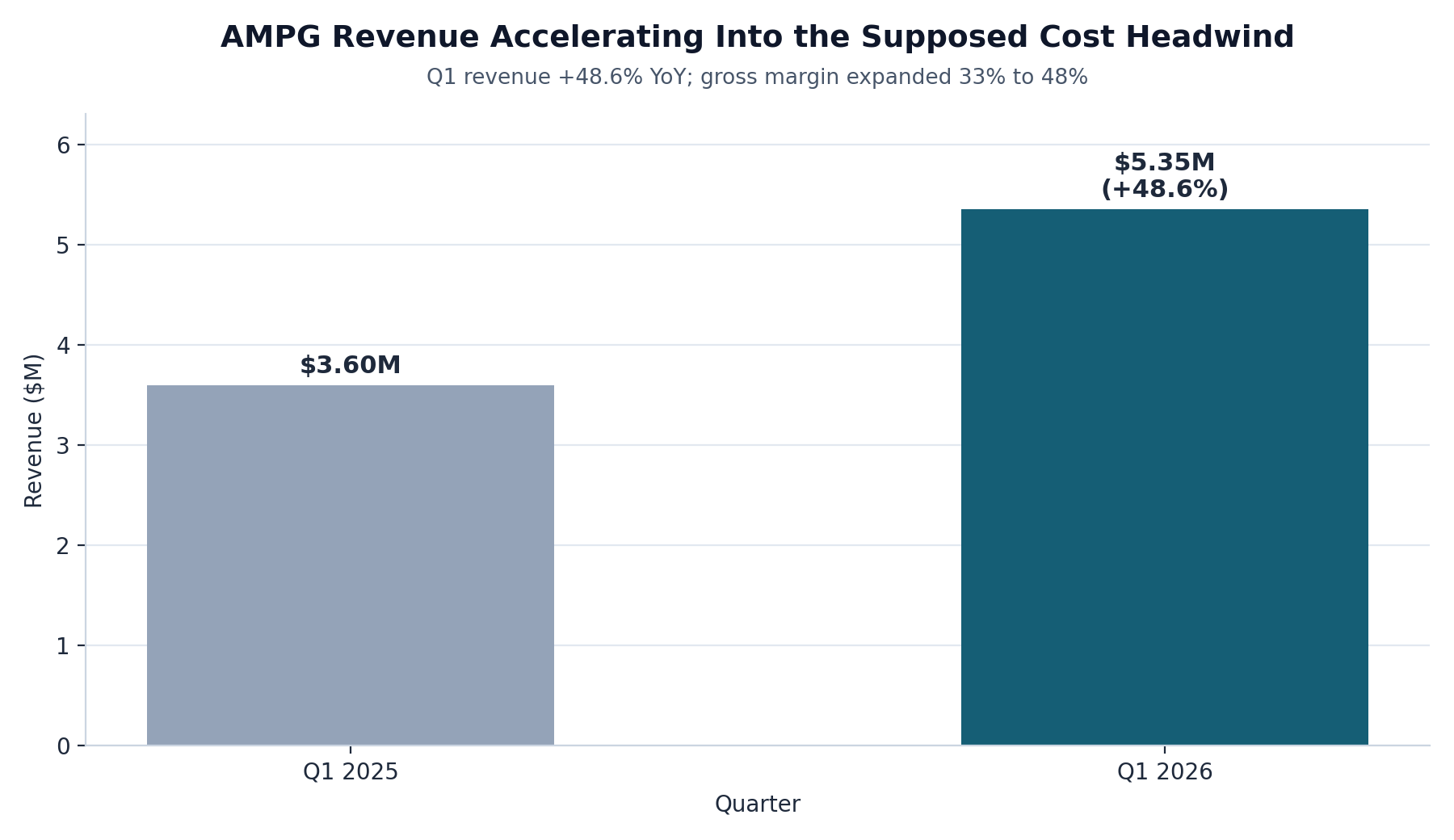

When component and memory costs rose across the hardware complex, the market reflexively punished AMPG — identical to the mistake made with Apple. But the cost narrative ignores the second-order truth: AMPG’s customers need the product. Cellular carriers completing their networks and satellite operators closing coverage gaps are not discretionary buyers; they are racing a federally-mandated, AI-accelerated clock. When demand is inelastic and the supplier is the only trusted domestic source, higher input costs are passed through, not absorbed. The proof is in the numbers: Q1 2026 revenue rose 48.6% YoY to $5.35M while gross margin expanded from 33.0% to 48.0%. That is margin expansion straight into the supposed cost headwind — the same signature that exposed the Apple misjudgment.

Exhibit A — Revenue +48.6% YoY with gross margin expanding 33% to 48% — margin expansion into the cost scare.

2. The Sole-American-Source Moat

AMPG is the only American company to have designed and commercialized an O-RAN radio at this specification level. This is not marketing — it is a structural moat with three edges. First, it aligns AMPG with US national-security and supply-chain policy that explicitly favors trusted, domestic equipment. Second, it insulates AMPG from tariffs and trade disputes that raise rivals’ costs. Third, it makes AMPG the default answer whenever a buyer’s funding or security requirements demand US content. In a market where the alternative vendors are foreign and increasingly restricted, being the only American option is the entire ballgame.

3. US-Only Law Is a Massive, Funded Tailwind

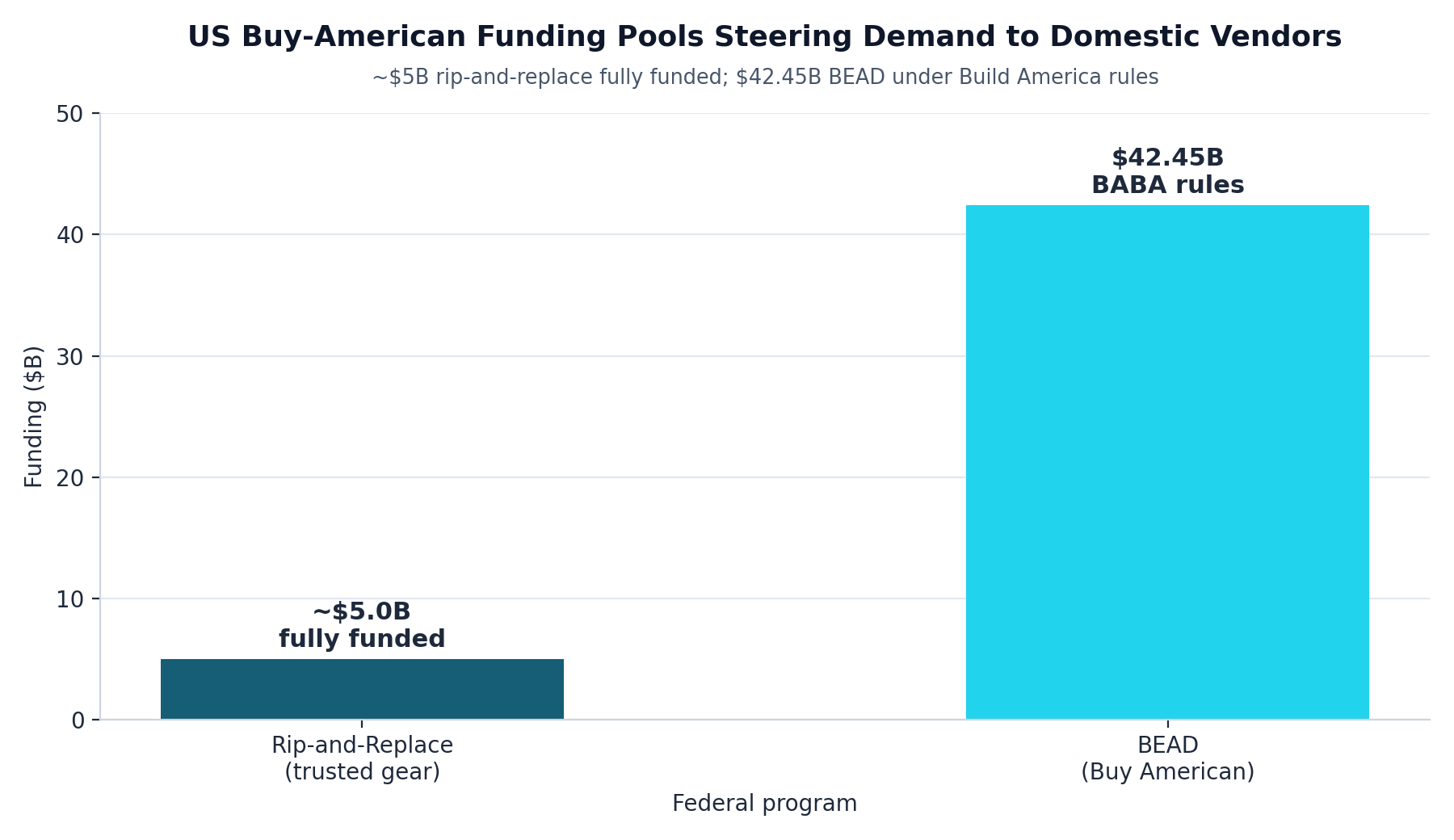

This is the heart of the thesis. Washington is not merely encouraging domestic equipment — it is funding the removal of foreign gear and reserving dollars for American-made content. The Secure and Trusted Communications Networks Reimbursement Program (“rip-and-replace”) is now fully funded at roughly $5 billion following the FY2025 NDAA, financing 126 carriers to tear out Huawei/ZTE equipment and replace it with trusted gear. Separately, the BEAD program directs $42.45 billion under Build America, Buy America (BABA) domestic-content rules. Together this is a federally-funded demand machine that channels buyers directly toward the only American radio maker. The buyer’s budget is underwritten by the US government on the explicit condition that the equipment be trusted and, increasingly, domestic — the single most favorable backdrop a sole-US-source supplier could ask for.

Exhibit B — ~$5B fully-funded rip-and-replace plus $42.45B BEAD under Buy-American rules.

4. How Fast This Is Happening — The AI-Forced SA Acceleration

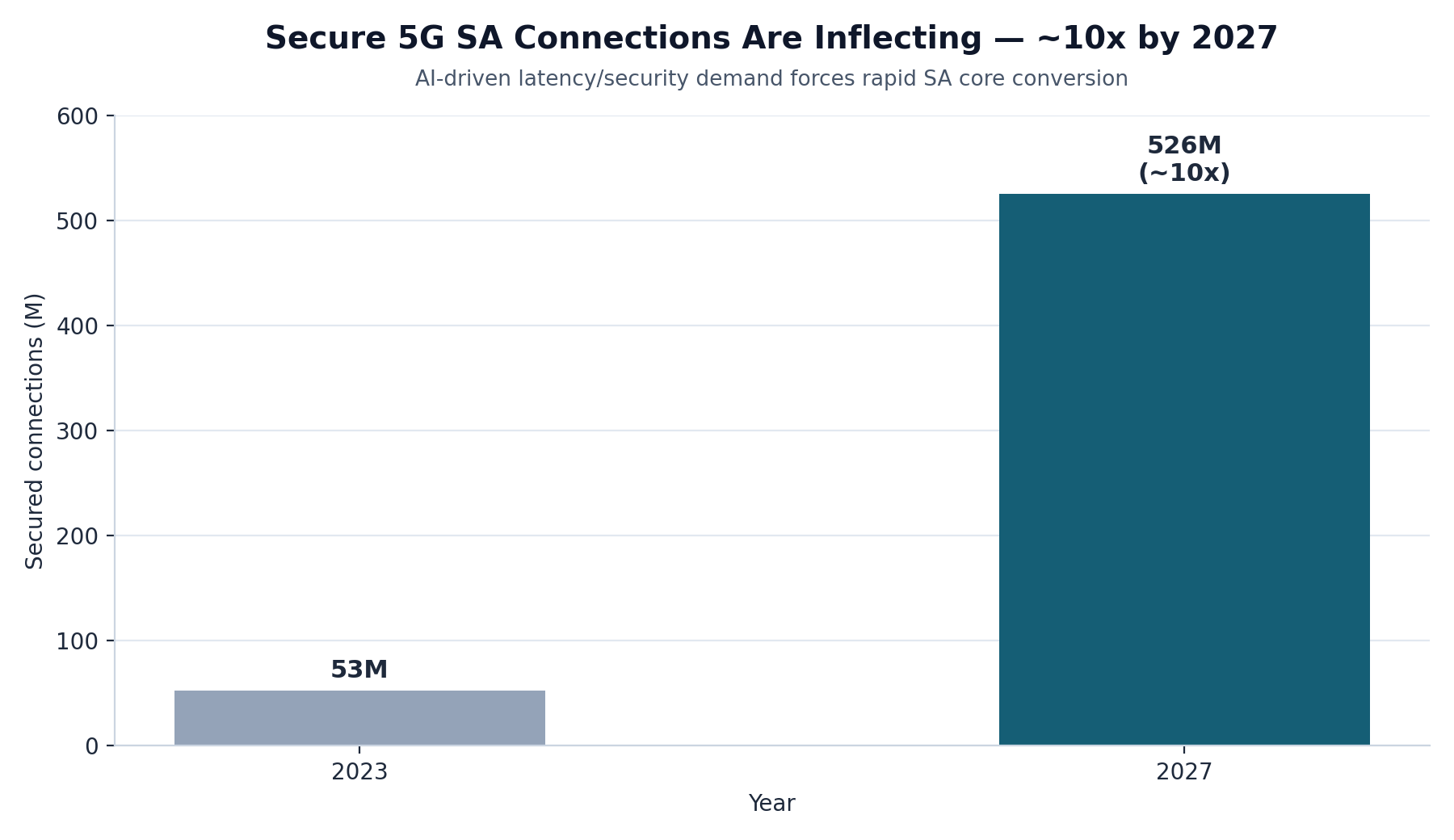

Speed is the under-appreciated variable. The same AI-productivity surge driving paid demand through Apple devices is forcing operators to complete the 5G Standalone (SA) core — the layer that delivers the low latency, network slicing, and end-to-end security that high-value AI workloads require. AI is now explicitly forcing networks to rethink upload and latency requirements, and SA deployment is inflecting: 78 operators had launched SA across 42 countries by September 2025, with 96 more committed. Secured SA connections are forecast to grow nearly 10x — from 53 million in 2023 to 526 million by 2027. Most US networks are slated to complete their transition by 2026. Every one of those upgrades needs trusted radio hardware, and the clock is being set by AI demand, not by leisurely carrier capex cycles.

Exhibit C — Secured 5G SA connections forecast ~10x (53M in 2023 to 526M by 2027).

5. Pricing Power: AMPG Can Pass It Through Like Apple

The decisive parallel to Apple is pricing power. Apple raises its toll because the iPhone is indispensable and demand is inelastic; AMPG can do the same because cellular and satellite operators need trusted, US-made radios and have few-to-no domestic alternatives. When a carrier is on a federally-funded, AI-driven deadline to rip out foreign gear and stand up an SA network, a modest increase in equipment cost is a rounding error against the cost of missing the window or failing a trusted-vendor requirement. That is why AMPG expanded gross margin to 48% even as input costs rose — the cost was passed through, not eaten. Indispensable product plus funded, deadline-driven buyer equals durable pricing power.

“When the buyer is racing a federal deadline and you are the only American option, you do not eat the cost — you pass it along. AMPG just proved it with 48% gross margin.”

6. The Markets Are Broad and Compounding

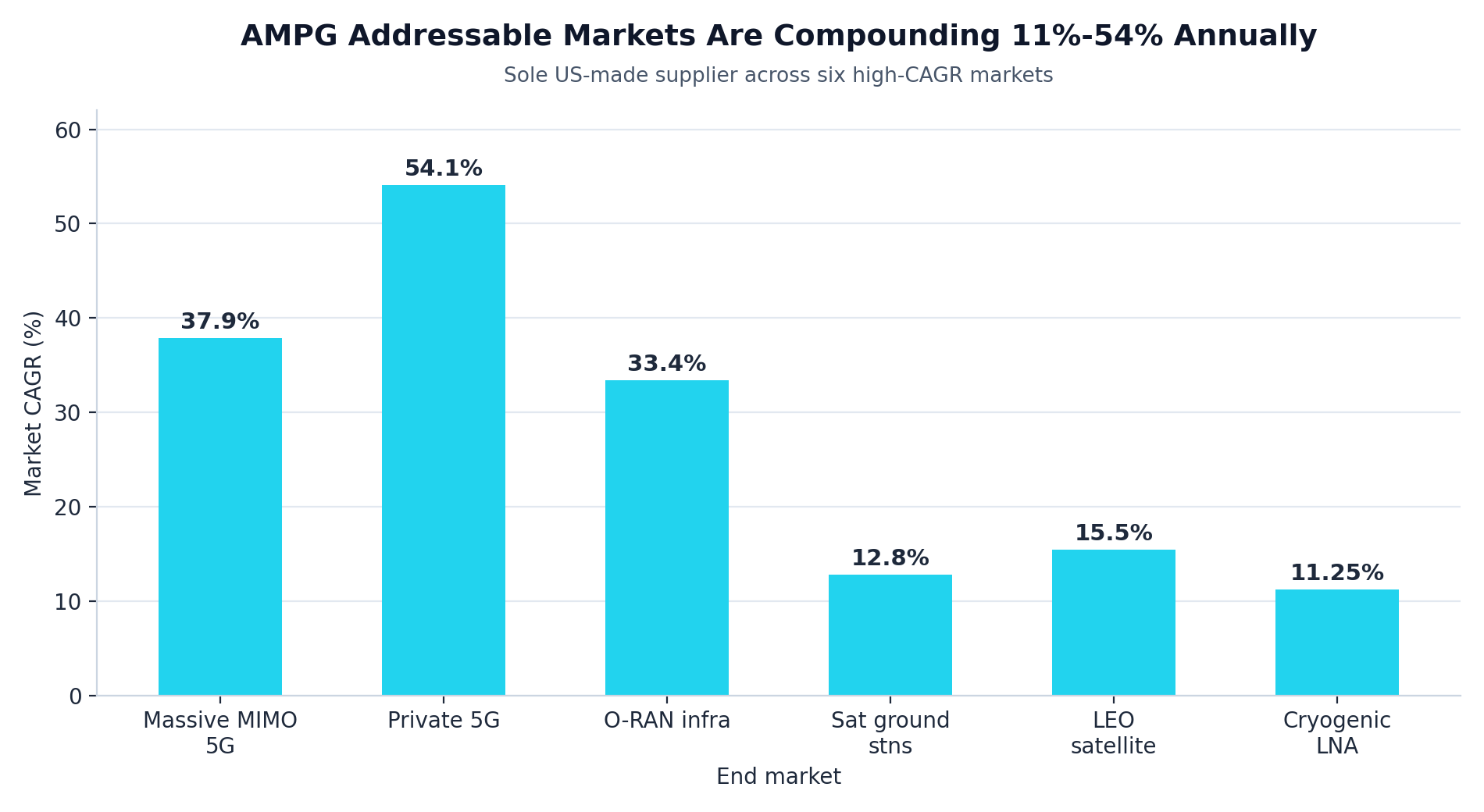

AMPG is not a one-trick supplier. Its trusted-domestic positioning spans six high-growth markets simultaneously, smoothing the ramp and multiplying the addressable demand: commercial Massive MIMO 5G O-RAN (~37.9% CAGR), private 5G networks for factories, logistics, military and healthcare (~54.1% CAGR), the total O-RAN infrastructure market (~33.4% CAGR toward $42B by 2030), satellite ground stations (~12.8% CAGR), LEO satellite communications such as the constellations closing the rural coverage gap (~15.5% CAGR), and cryogenic systems for quantum computing (~11.25% CAGR). New FCC and Canadian certifications for complete indoor 5G infrastructure open private and in-building deployments on top of all of this. Demand is diversified across independent drivers — no single cycle gates the story.

Exhibit D — Six addressable markets compounding 11%–54% annually, all favoring the sole US-made supplier.

7. Pipeline Visibility and the Setup

The demand is not hypothetical. AMPG carries a Letter-of-Intent pipeline exceeding $100 million with major Asian and North American operators, a portion already converted to funded purchase orders that began shipping in late 2025, plus a five-year supplier agreement with Fujitsu validating the technology globally. Against a ~$179M market capitalization, a sole-US-source supplier with margin expansion, a $100M+ pipeline, and a federally-funded, AI-accelerated demand backdrop is being valued as a cost casualty rather than the trusted toll booth it is. The market made this exact error with Apple. We believe it is making it again with AMPG.

“AMPG has been unfairly tainted as a cost victim. It is in fact the only American radio on a federally-funded, AI-accelerated buildout — and the demand is arriving now.”

AUTHOR HEDGE & DISCLOSURE — READ BEFORE RELYING ON THIS DOCUMENT.

This report is published by JD Unfiltered Research for informational and educational purposes only. It is NOT investment advice, not a recommendation, solicitation, or offer to buy or sell any security, and is not a personalized recommendation for any individual. AmpliTech Group (NASDAQ: AMPG) is a micro-capitalization stock that is speculative, thinly traded, and subject to elevated volatility, dilution, and liquidity risk. The author and/or affiliated entities may hold, and may at any time buy or sell, positions in AMPG and related securities, and therefore have a potential conflict of interest. The author has not been compensated by AmpliTech Group for this report. All revenue figures, pipeline/LOI conversion assumptions, market-size and CAGR estimates, the pricing-power and “pass-through” thesis, and all forward-looking statements are illustrative opinions, not facts or guarantees, and rest on assumptions that may prove materially incorrect. Letters of Intent are non-binding and may not convert to revenue. Forward-looking statements involve significant risks — including LOI-to-order conversion, customer concentration, supply-chain and component-cost volatility, competition, changing regulation and the absence of any law guaranteeing sole-source awards, capital needs and dilution (including recently listed rights), and macroeconomic conditions — and actual results may differ materially. Third-party data is believed reliable but has not been independently verified. Readers must conduct their own due diligence and consult a licensed financial, tax, and legal advisor before investing. The author and JD Unfiltered Research disclaim any liability for losses arising from use of this document. By reading you accept these terms. © 2026 JD Unfiltered Research. For external distribution.