The AI Data Center Supercycle

The Companies Powering the Buildout and Why the Smartest Money on Wall Street Is Crowding In

A nine-company infrastructure portfolio including AmpliTech Group (NASDAQ: AMPG) as a featured essential play and positioned for the largest capital-deployment cycle in modern history.

Executive Summary

The artificial-intelligence buildout has become the largest coordinated infrastructure capital deployment in modern history. The five largest hyperscalers alone are on track to spend roughly $805 billion in 2026 — nearly double the prior year — scaling toward $1.1 trillion in 2027, while Goldman Sachs projects a cumulative $7.6 trillion of AI-related capital expenditure between 2026 and 2031.¹ ² This is not a cyclical trade. It is a secular supercycle comparable to the railroads or the interstate highway system.

Crucially, the bottleneck is no longer chips or talent — it is power. The International Energy Agency projects global data-center electricity demand to more than double, from 415 TWh in 2024 to 945 TWh by 2030, with U.S. data centers accounting for nearly half of all electricity demand growth.³ Grid interconnection queues hold roughly 2,300 GW of pending projects and high-voltage transformer lead times now run three to five years. This structural choke point has reoriented sophisticated capital toward the "picks-and-shovels" layer: on-site power, optical networking, GPU cloud, repurposed mining infrastructure, memory, and the radio hardware of the AI-enabled edge.

The Core Thesis in Three Points

- Infrastructure beats applications. Every foundation model and every hyperscaler needs the same physical layer — power, cooling, networking, compute, storage. The infrastructure layer is winner-agnostic and protected by structural scarcity, long-duration contracts, and capital-intensity moats.

- The big moves are real — but it is still early. Most names in this portfolio have already delivered triple-digit returns, yet they trade against a capex wave that has barely begun to crest. 2026 hyperscaler spend nearly doubles 2025; the supercycle runs through 2031 and beyond.

- The smart money has converged. Across every hedge-fund style — macro, value, growth, multi-strategy — the most sophisticated managers are rotating from AI software into the physical infrastructure stack. This is one of the clearest institutional signals of the cycle.

The Macro Opportunity at a Glance

This report covers a nine-company portfolio spanning the full infrastructure stack — on-site power (Bloom Energy), photonics (Lumentum), GPU cloud (CoreWeave), repurposed data-center operators (Core Scientific, IREN, Applied Digital, Cipher Mining), memory (SanDisk), and a featured micro-cap essential play in AI-edge radio and RF hardware (AmpliTech Group). It documents the macro thesis, live valuations, the hedge-fund positioning behind the theme, and the risks every sophisticated investor should weigh.

1. The Macro Thesis: A Trillion-Dollar Supercycle

Capex on a Scale Without Precedent

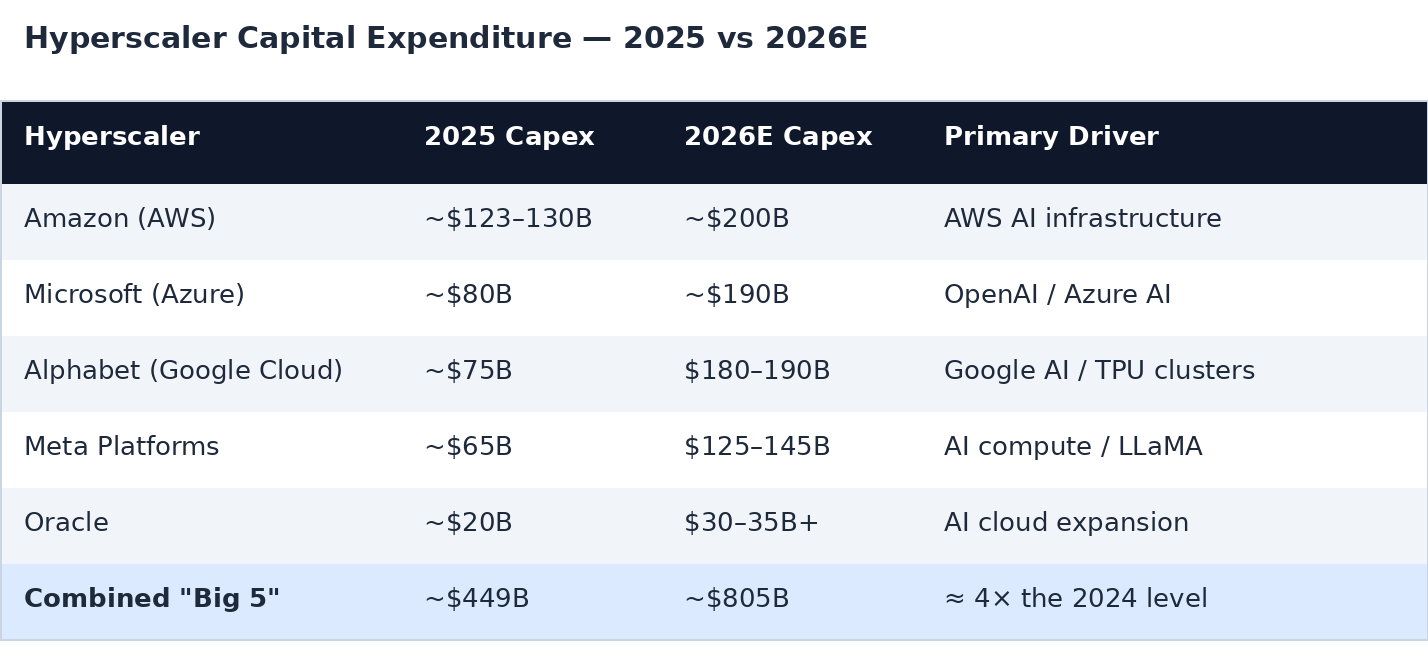

The defining feature of the AI buildout is the sheer magnitude of committed capital. Morgan Stanley raised its 2026 capex forecast for Amazon, Alphabet, Meta, Microsoft, and Oracle to $805 billion — nearly double 2025's ~$449 billion and more than four times the group's 2024 spend — and projects $1.1 trillion for 2027.⁴ Amazon alone guided to $200 billion of capex in 2026, the largest single-year investment commitment ever made by any company.⁵ Goldman Sachs models a cumulative $7.6 trillion of AI infrastructure spend across compute, data centers, and power between 2026 and 2031, reaching $1.6 trillion annually by 2031.⁶

Source: Morgan Stanley; company guidance; Goldman Sachs Global Institute (May 2026).

Power Is the Bottleneck

The rate-limiting factor for the entire buildout is electricity. The IEA projects global data-center electricity demand to more than double from 415 TWh in 2024 to 945 TWh by 2030 — roughly the entire electricity consumption of Japan today — with electricity use from AI-focused facilities expected to triple between 2025 and 2030.⁷ The supply side cannot keep pace:

- Interconnection gridlock: ~2,300 GW of generation and storage sat in U.S. interconnection queues at end-2024 — nearly double the installed U.S. fleet; median time to commercial operation now exceeds five years.

- Transformer scarcity: high-voltage transformer demand rose 119% from 2019 to 2025; lead times now run three to five years for high-voltage substations.

- "Bring Your Own Power": ~50 GW of behind-the-meter gas generation was announced in 2025 alone; on-site and hybrid generation now account for close to half of all announced capacity.

- Utility response: 51 U.S. investor-owned utilities have planned at least $1.4 trillion of capex through 2030, up 21% year over year, with 30+ citing data centers as a top growth driver.

Why "Picks and Shovels" Wins

The thesis parallels the 1849 Gold Rush: the merchants selling picks and shovels often outperformed the prospectors. In AI, the application layer faces fierce competition and uncertain monetization, while the infrastructure layer benefits from inelastic demand regardless of which model or cloud wins. Goldman Sachs concludes the ~$7.6 trillion aggregate is structural.⁶ Four properties make infrastructure the superior risk-adjusted exposure:

- Winner agnosticism — the physical layer is needed no matter which AI company wins.

- Structural scarcity — power, land, and long-lead equipment cannot be conjured like software.

- Contract duration — 10- to 20-year leases and PPAs create durable cash-flow visibility.

- Capital intensity as a moat — at $15–25M per MW, the cost of entry protects incumbents.

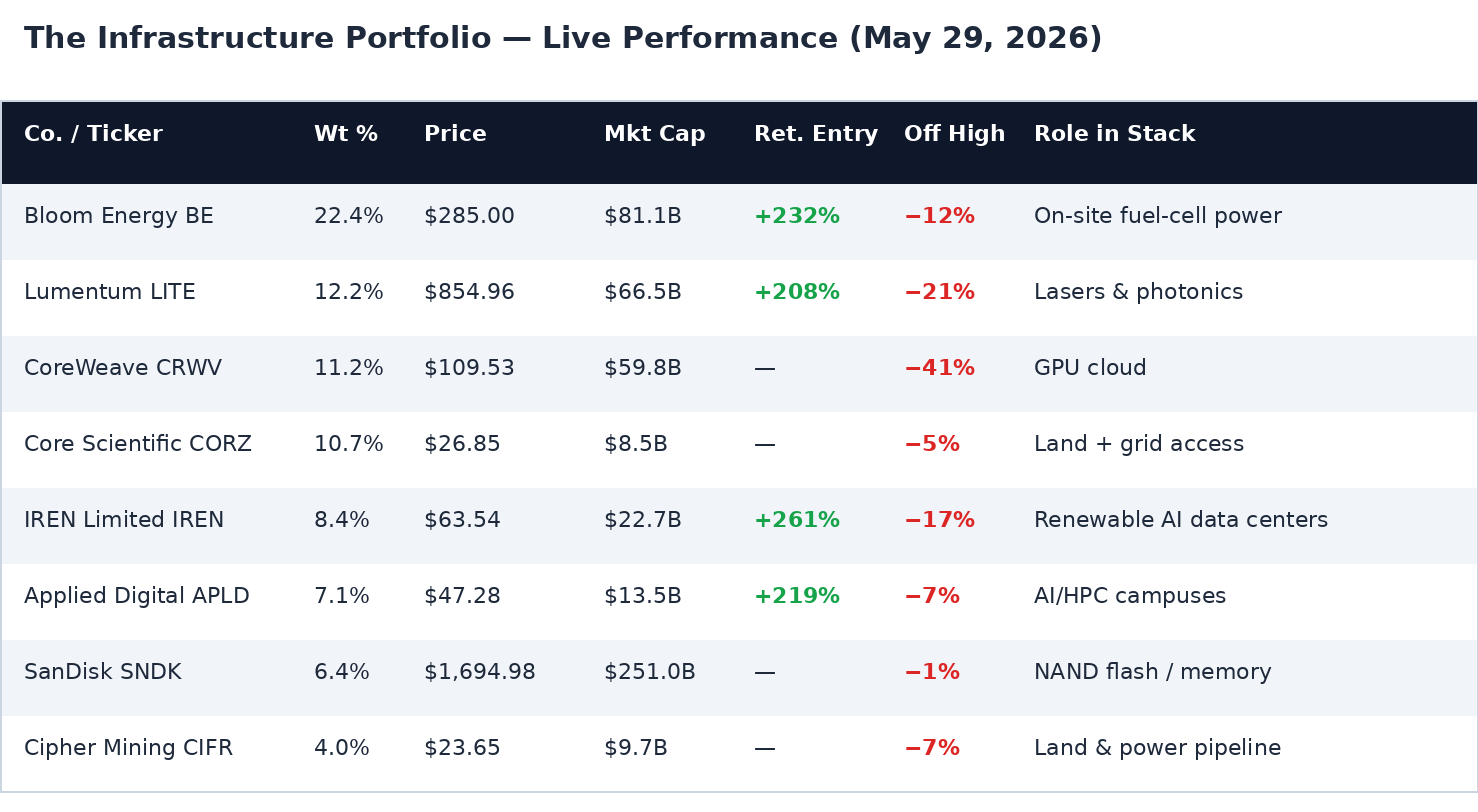

2. The Infrastructure Portfolio: Live Performance

The eight core holdings below map directly to the infrastructure stack — from the power feeding the rack to the memory inside it. All figures reflect live market data as of the May 29, 2026 close. Returns marked "from entry" are measured against documented accumulation levels; current prices and market caps are pulled from structured market data.⁸ The pattern is consistent: large moves already booked, yet each name still trades well below its 52-week high against a capex wave that is only now accelerating.

Weights reflect the documented "Situational Awareness"-style infrastructure portfolio (eight names = ~82% of weight). "—" entry returns denote post-IPO or newly initiated positions without a single documented entry price. Prices/market caps: structured market data, May 29, 2026 close.

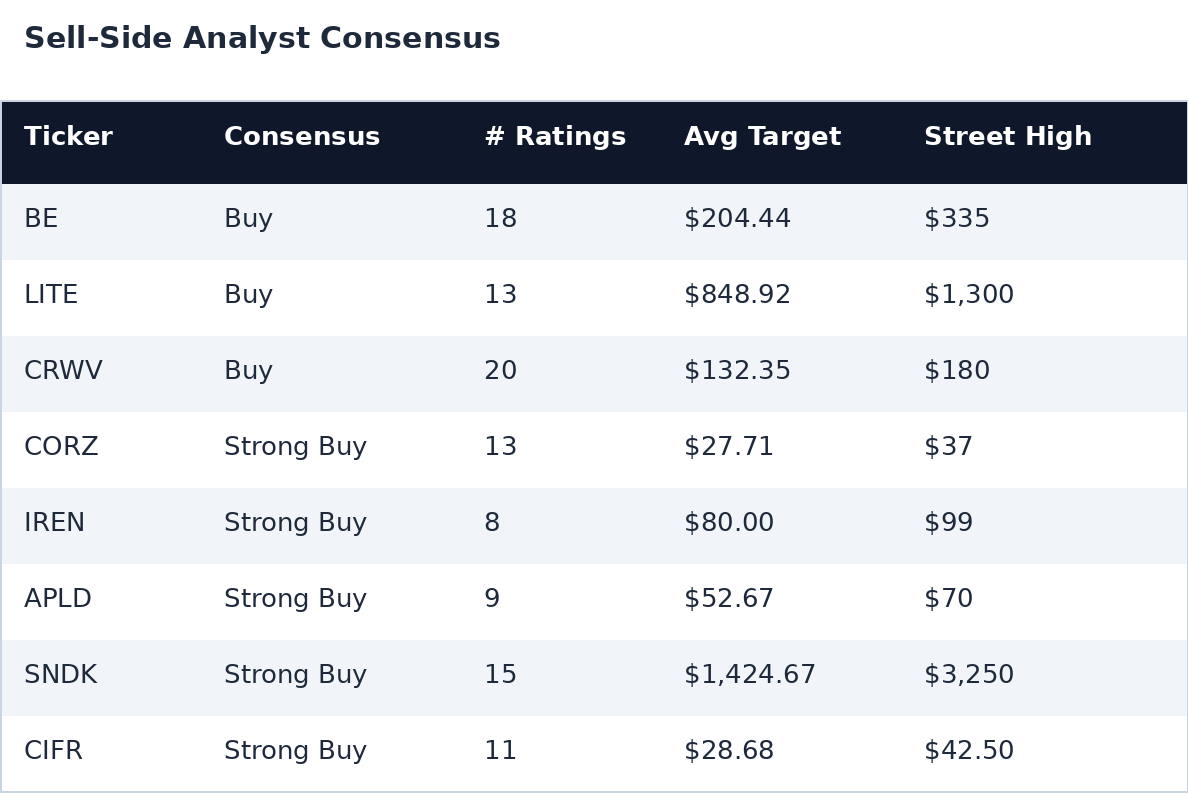

Sell-Side Consensus: Overwhelmingly Bullish

Wall Street analyst ratings reinforce the early-stage view. Five of the eight core names carry a Strong Buy consensus, several with 100% bullish coverage and average price targets above current levels.⁸

Source: structured analyst-research data, May 2026. Targets are consensus means; Street High is the most bullish published target.

Company Snapshots

A brief on each core holding and its position in the AI infrastructure value chain.

Bloom Energy (BE) — ON-SITE POWER • 22.4% weight

Bloom's solid-oxide fuel cells output low-voltage electricity directly, bypassing the transformer/grid bottleneck entirely — the single most valuable property in a power-constrained buildout. The company has 1.5 GW installed and a deal slate that includes a $5B Brookfield partnership, a $2.65B AEP contract, an up-to-2.8 GW Oracle agreement, and a $2.6B Nebius deal for 328 MW of AI data-center capacity.⁹

Lumentum (LITE) — PHOTONICS • 12.2% weight

As AI clusters scale to thousands of GPUs linked by high-speed optical interconnects, photonics has become the next bottleneck after power. Lumentum supplies the lasers, transceivers, and switches that move data inside and between AI data centers — a direct beneficiary of Nvidia's strategic $500M optical-connectivity investment in Corning.¹⁰

CoreWeave (CRWV) — GPU CLOUD • 11.2% weight

The defining GPU-cloud company and effectively the "third hyperscaler." FY2025 revenue of $5.1B (+168% YoY), 2026 capex guided to $30–35B against signed contracts with Anthropic, OpenAI, and Microsoft. Nvidia holds CoreWeave as its second-largest disclosed investment (~$3.65B). At ~41% below its high, it is the deepest discount in the portfolio.¹¹

Core Scientific (CORZ) — DATA-CENTER REIT-LIKE • 10.7% weight

A former bitcoin miner now CoreWeave's primary landlord, with ~590 MW contracted under long-dated leases — described as "a high-yield bond on hyperscaler AI demand wrapped in equity optionality." Acquired Polaris DS for $421M to expand Oklahoma power capacity.¹²

IREN Limited (IREN) — AI DATA CENTERS • 8.4% weight

Vertically integrated from kilowatt to GPU, IREN borrowed ~$3.6B to buy Nvidia chips and signed a $1.6B Nvidia deal for AI-infrastructure expansion. BlackRock boosted its stake by 604.9% in Q1 2026 to over $252M — a striking institutional endorsement.¹³

Applied Digital (APLD) — AI/HPC CAMPUSES • 7.1% weight

A purpose-built AI data-center developer whose Ellendale, North Dakota campus — with CoreWeave as anchor tenant and a 400 MW first phase — is the showcase asset. Holds a documented $320M position in the Situational Awareness portfolio.¹⁴

SanDisk (SNDK) — MEMORY • 6.4% weight

Spun off from Western Digital in early 2025 as a pure-play NAND/SSD company. Q3 FY2026 revenue of $5.95B (+251% YoY) with datacenter revenue up 645% YoY — what the CEO called "a fundamental inflection point." The most widely held "consensus picks-and-shovels" trade among major funds.¹⁵

Cipher Mining (CIFR) — LAND & POWER • 4.0% weight

Transitioning from bitcoin to high-performance computing, Cipher signed its third AI data-center lease (15-year, investment-grade tenant) and holds a 3.2 GW pipeline across six projects; its bond offering was ~6.5× oversubscribed. Jefferies initiated with Buy in May 2026.¹⁶

Featured Essential Play: AmpliTech Group (NASDAQ: AMPG)

The Micro-Cap RF & AI-Edge Hardware Play

Most AI-infrastructure portfolios stop at the data-center fence line. AmpliTech Group extends the thesis to the wireless edge and the physical signal layer — the RF/microwave components, 5G Open-RAN radios, satellite amplifiers, and cryogenic amplifiers for quantum computing that connect AI compute to the world. It is the portfolio's deliberate high-asymmetry, micro-cap essential play: a debt-free, U.S.-manufacturing company at an inflection point, trading at a fraction of the valuations commanded by its larger peers.¹⁷

Why It Belongs in This Portfolio

AmpliTech occupies a narrow but strategically critical slice of the AI hardware stack — the physical-layer signal processing that the data-center names do not address:

- The only U.S.-made O-RAN CAT B 64T/64R Massive MIMO radio — a defensible position as operators face government pressure to diversify away from Chinese vendors. In May 2026 it was the central hardware platform in Northeastern University's world-first open-source Massive MIMO AI-RAN demonstration using NVIDIA's Aerial AI software.¹⁸

- Cryogenic HEMT amplifiers for quantum computing — operating at 4 Kelvin, already delivered to two Fortune 50 quantum leaders, with a USPTO Notice of Allowance secured.

- Ultra-low-noise amplifiers for LEO satellites — prototype units delivered to a Fortune 50 satellite provider, exposure to the Starlink/Kuiper backhaul layer connecting AI-capable edge nodes.

- Vertical integration from MMIC chip design to full radio system — rare at any scale, essentially unique among small-cap U.S. wireless-hardware companies.

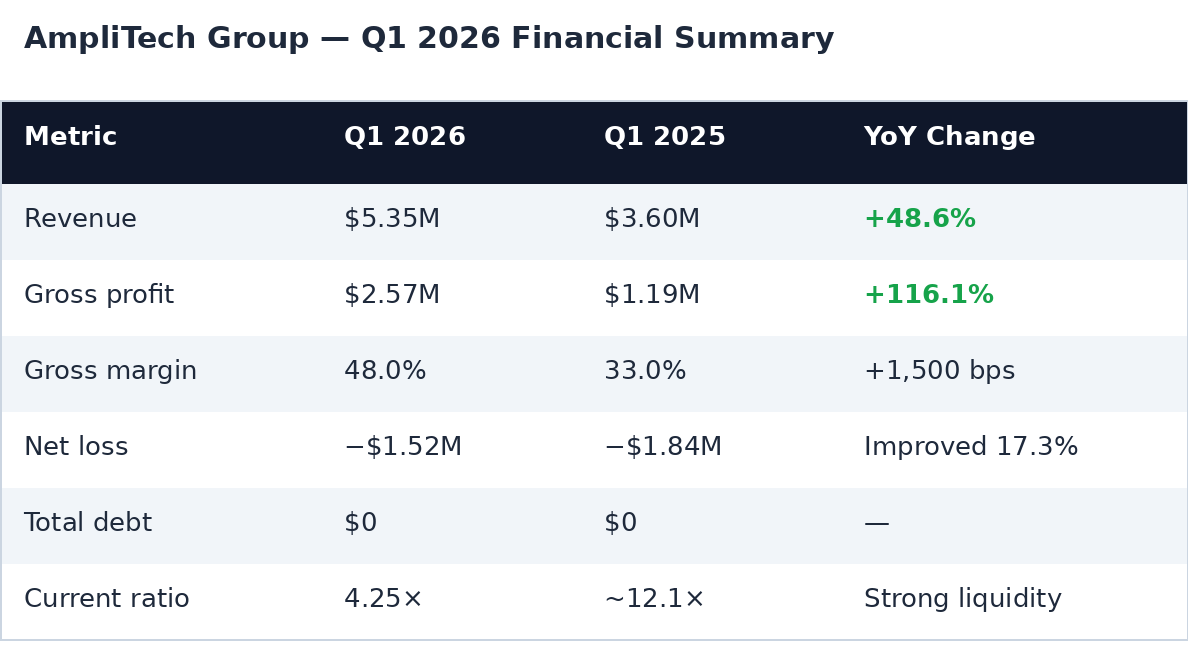

The Financial Inflection

AmpliTech reported record FY2025 revenue of $25.2M, up 163% year over year, and has guided to $50M+ in FY2026 — roughly 100% growth. Q1 2026 revenue rose 48.6% YoY to $5.35M while gross margin expanded ~1,500 basis points to 48%, confirming the unit economics are sound at scale. The balance sheet is clean: zero debt, a 4.25× current ratio, and ~$18.4M in cash and marketable securities.¹⁷ ¹⁹

Source: structured finance data; AmpliTech Q1 2026 earnings (reported May 13, 2026).

The Revenue Engine: Two Major LOIs

AmpliTech's near-term story is anchored by two large Letters of Intent that are converting into funded purchase orders:

- $40M LOI with a Tier-1 North American mobile network operator — over $20M in funded POs received, ~$12M shipped, shipments resumed in April 2026 with a further $2M+ in follow-on orders.

- $78M+ LOI with a value-add channel partner — management believes it will grow beyond $100M over two years; described as the largest O-RAN deployment in North America.

Combined, these programs represent over $118M of potential value — more than the company's entire current market capitalization — against a backlog already exceeding 4× quarterly revenue.¹⁹

Valuation & Analyst View

At $4.42, AMPG trades at roughly 1.9× its FY2026 revenue guidance — a modest multiple for a defense/telecom hardware company with this growth profile and AI/quantum/satellite optionality. Maxim Group maintains a Buy rating with a $7 price target, implying ~58% upside.²⁰ If AmpliTech executes on $50M in revenue with continued margin improvement, a 3–4× revenue multiple would imply a $150–200M market cap — with the quantum and LEO-satellite businesses essentially free at today's valuation.

Bull Case vs. Key Risks

BULL CASE

- ✓ Only U.S.-made 64T/64R O-RAN radio; validated in NVIDIA AI-RAN demo

- ✓ 163% FY2025 revenue growth; ~100% guided for FY2026

- ✓ 48% gross margin proves unit economics at scale

- ✓ Zero debt, 4.25× current ratio, ~$18.4M liquidity

- ✓ $118M+ in LOIs vs. a ~$93M market cap

- ✓ Free optionality on quantum and LEO-satellite hardware

KEY RISKS

- × Micro-cap liquidity; 52-week range spans a 244% spread

- × Not yet profitable; ~$3–4M quarterly cash burn

- × LOIs are non-binding; execution and timing risk

- × Active equity issuer — dilution risk

- × Single analyst (Maxim) provides coverage

- × Revenue is lumpy and back-half weighted in FY2026

AMPG is not a position for capital that cannot tolerate significant drawdowns or multi-quarter holding periods. It is sized as a small, high-asymmetry allocation alongside the larger, more liquid names — early-stage exposure to the physical-layer hardware of the AI era.

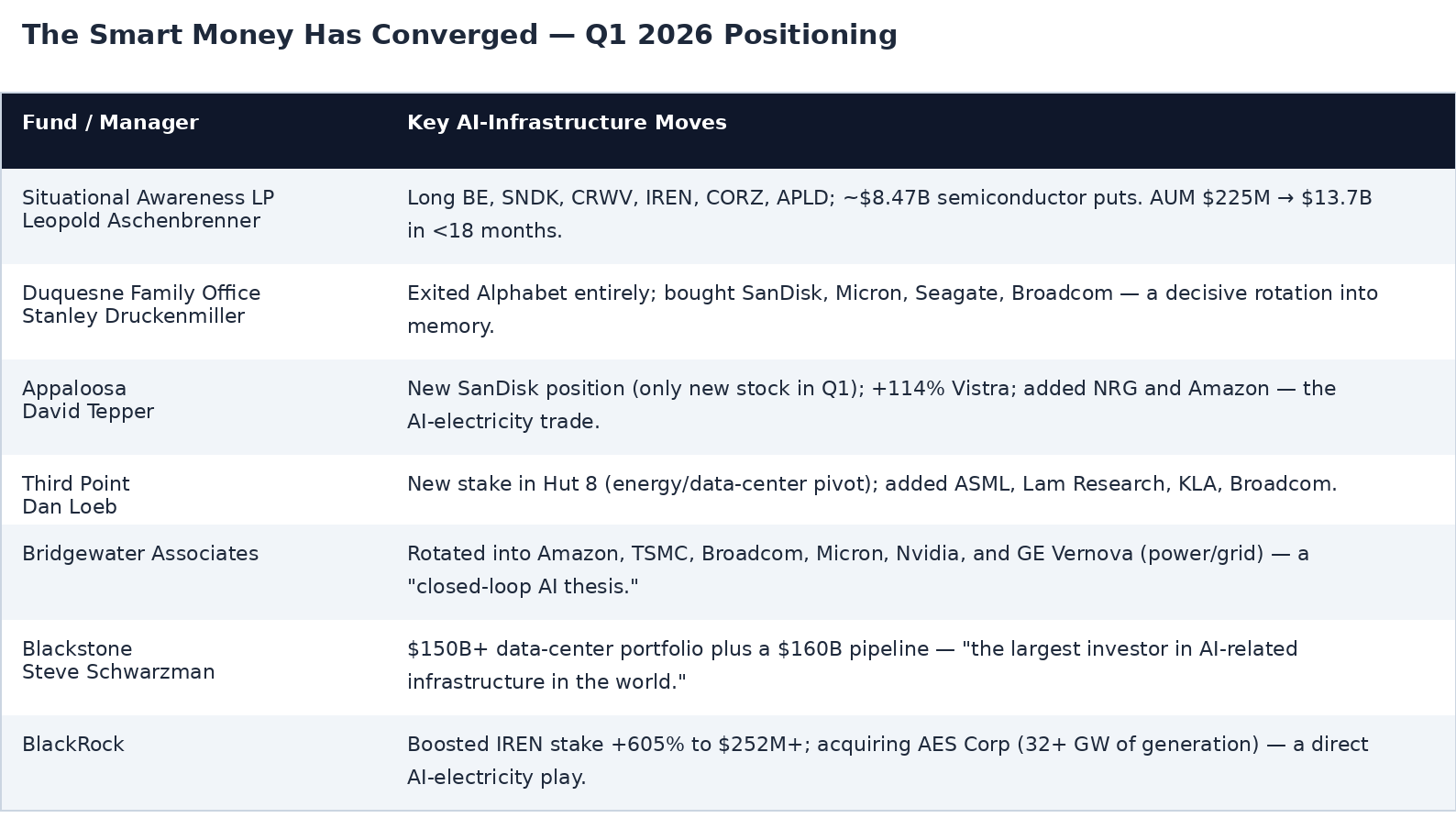

3. The Smart Money Has Converged

Perhaps the most powerful confirmation of this thesis is the convergence of sophisticated capital. Across the ideological spectrum of hedge-fund styles — macro, value, growth, multi-strategy — the most-watched managers on Wall Street are rotating out of AI software and application names and into the physical infrastructure layer. The shared logic: the buildout is inevitable and largely independent of which AI model or application ultimately wins.²¹

"Whichever foundation model wins and whichever hyperscaler captures the workloads, every token generated still needs DRAM to train it, NAND to serve it, and HDD to archive it."

— Thesis attributed to Stanley Druckenmiller, who exited Alphabet entirely to buy SanDisk, Micron, and Seagate

The Bellwether: Situational Awareness LP

No fund embodies the theme more completely than Situational Awareness LP, founded by former OpenAI researcher Leopold Aschenbrenner and backed by the Collison brothers, Nat Friedman, and Daniel Gross. Its disclosed assets grew from $225M to $13.7 billion in under 18 months — one of the fastest ramps in hedge-fund history — on a single trade: long the physical AI-infrastructure layer, short richly valued chipmakers.²² Its disclosed long book reads almost exactly like this portfolio:

- Bloom Energy ~$934M

- SanDisk ~$1.1B

- CoreWeave ~$697M

- IREN ~$401M

- Core Scientific ~$389M

- Applied Digital ~$320M

- Offset by ~$8.47B in semiconductor put options (Nvidia, SMH, Oracle, Broadcom, AMD) — a structural long-infrastructure / short-chipmaker-valuation trade.

A Cross-Style Consensus

What makes the signal compelling is its breadth. The same names appear across funds that rarely agree:

Source: Q1 2026 13F filings and public reporting. 13F holdings reflect disclosed positions as of quarter-end and carry a 45-day filing lag.

The convergence of Druckenmiller, Tepper, Aschenbrenner, Bridgewater, Loeb, Blackstone, and BlackRock on the same physical-infrastructure thesis — through public equities, private markets, and in some cases the most concentrated positions of their careers — is, in our view, the clearest institutional signal that the smart money has identified the AI buildout's true winners.

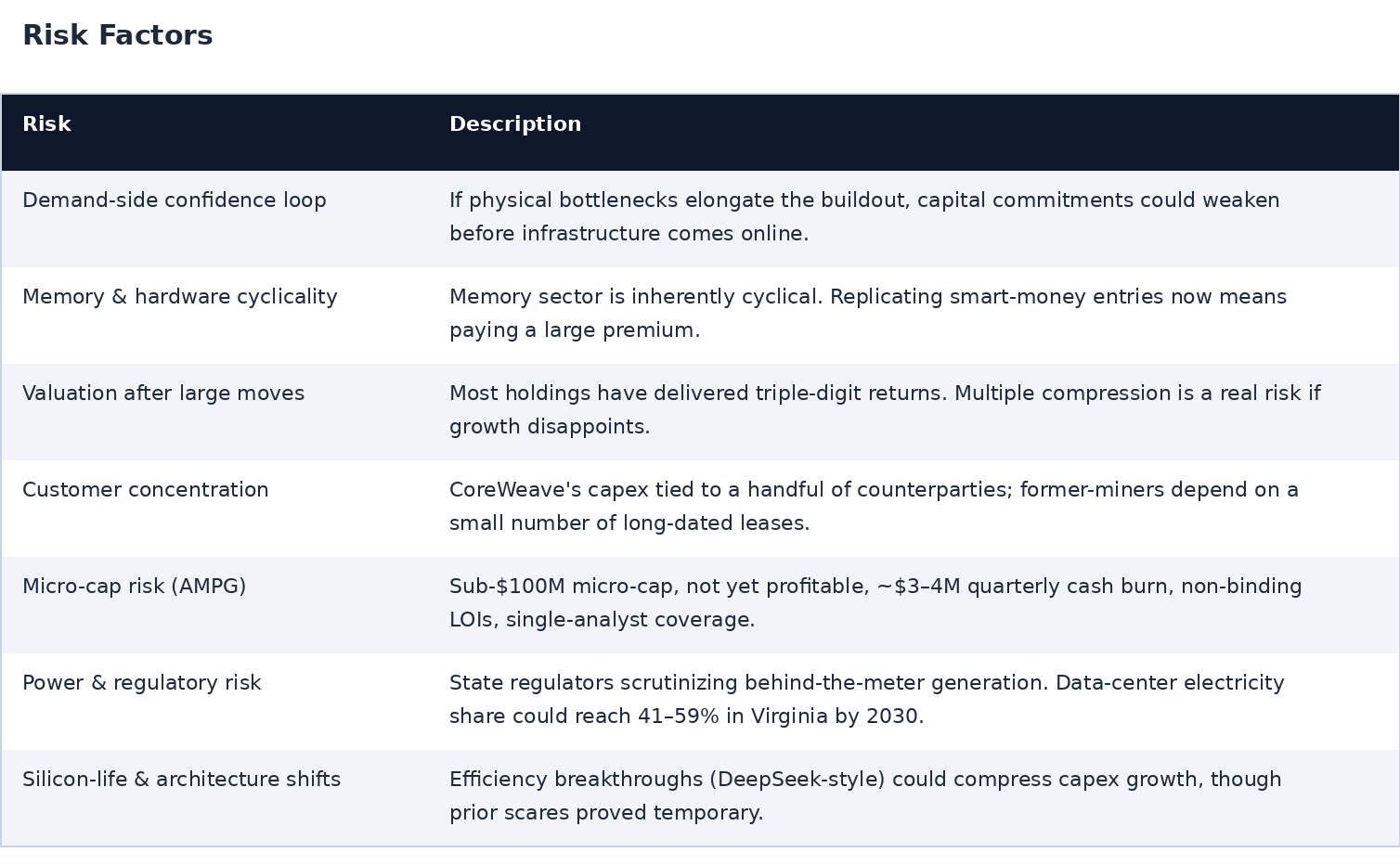

4. Risk Factors

No thesis is without risk, and sophisticated investors should weigh the following alongside the opportunity. This portfolio carries elevated volatility, concentration, and valuation risk by design.

The Bottom Line

The AI data-center buildout is a structural supercycle, not a passing trade. The bottleneck is power, and the durable winners sit in the infrastructure layer — on-site power, photonics, GPU cloud, repurposed data-center operators, memory, and the AI-edge radio hardware exemplified by AmpliTech. Most of these names have already moved sharply, yet they trade against a capex wave that nearly doubles in 2026 and runs through 2031. The convergence of the world's most sophisticated investors on this exact thesis suggests it is still early. For investors who can tolerate volatility and size positions appropriately, this is the picks-and-shovels portfolio of the AI era.

Sources & References

All market data, valuations, and analyst ratings are sourced from structured finance tools as of the May 29, 2026 close. Macro, company, and hedge-fund references are listed below.

Macro & Capex

- Goldman Sachs — "Tracking Trillions: The Assumptions Shaping the Scale of the AI Build-Out"

- Morgan Stanley — hyperscaler capex to $805B for 2026

- IEA — AI energy demand to double data-center power by 2030

- Morgan Stanley capex forecast

- Amazon Q1 2026 / $200B capex

- Goldman Sachs — cumulative $7.6T AI infrastructure spend 2026–2031

- IEA — data-center electricity demand to double by 2030

Portfolio Companies

- Live quotes, market caps, and analyst consensus from structured finance tools, May 29, 2026 close

- Bloom Energy deal slate (Oracle, AEP, Brookfield, Nebius)

- Lumentum / Nvidia $500M Corning photonics investment

- CoreWeave infrastructure analysis

- Core Scientific — $421M Polaris DS acquisition

- BlackRock +605% IREN stake

- Applied Digital / Situational Awareness 13F

- SanDisk Q3 FY2026 — datacenter revenue +645% YoY

- Cipher Mining — AI data-center strategy

AmpliTech Group (AMPG)

- AmpliTech investor relations & FY2025 results

- 64T/64R MIMO radio in Northeastern AI-RAN demo

- AmpliTech Q1 2026 earnings & Maxim Group rating

- Maxim Group Buy rating, $7 target

Hedge-Fund & Institutional Positioning

- Druckenmiller / Tepper / Aschenbrenner Q1 2026 13F summary

- Situational Awareness LP — full portfolio analysis

Disclosure: This report is for informational and educational purposes only and does not constitute investment advice, a recommendation, or an offer or solicitation to buy or sell any security. The authors hold positions in securities mentioned and reserve the right to buy or sell shares at any time without notice. Several holdings — particularly AmpliTech Group — are speculative, volatile, and may be unsuitable for many investors. Past performance is not indicative of future results. Forward-looking statements, hedge-fund 13F holdings (subject to a 45-day filing lag), and LOI/guidance figures are inherently uncertain. Conduct your own due diligence and consult a licensed financial professional before making any investment decision. Market data is as of the May 29, 2026 close and may not reflect subsequent changes.