SPCX: A Generational Acquisition Engine

The most expensive stock on Earth might also be the best acquisition currency ever created. Here's why — and where SpaceX should spend it first.

The Setup

Five days after the largest IPO in history, SpaceX trades at ~$2.7 trillion. At ~94x 2025 revenue, SPCX carries one of the richest multiples ever assigned to a company this large. Most investors are focused on whether that multiple is justified. We think they're asking the wrong question.

The right question is: what can SpaceX do with that multiple while it lasts?

The answer is something almost no company has ever been positioned to do — use an extraordinarily expensive stock as acquisition currency to absorb strategically critical capability at negligible dilution. The high multiple makes every deal accretive through pure multiple arbitrage: trade paper valued at 94x revenue for assets valued at 2x or 5x, and the acquired capability instantly re-rates toward the parent's valuation. This is the engine that built Cisco in the 1990s and Salesforce in the 2010s — but in a more extreme, vertically integrated form.

Our recommendation: run two programs. A repeatable bolt-on ladder of small RF/optical/AI tuck-ins, led by AmpliTech (AMPG). And a ring-fenced transformational track for one focused fab deal — GlobalFoundries over Intel.

Why This Almost Never Happens

The two ingredients SPCX has — and why they almost never coexist — are simple to state and hard to find together.

Most high-multiple companies are small or pre-profit. Most dominant cash generators trade at modest multiples. SPCX has both at once: total revenue rose 33% to $18.7B in 2025, Starlink grew ~50% to $11.4B with a ~63% EBITDA margin and ~85% recurring revenue, and the market pays 94x for it. That combination turns the stock into something more than equity. It turns it into a weapon.

The flywheel is self-reinforcing. High growth justifies the high multiple. The high multiple makes deals accretive. The core amplifies each acquisition by pushing a small product through Starlink/Starship scale. And accretive deals reinforce the growth narrative, sustaining the multiple and refreshing the currency for the next deal. McKinsey found the fastest-growing software companies do exactly this — layering frequent, complementary acquisitions on a strong organic core while maintaining ~31% growth.

What makes SPCX potentially unique in history is the scope of what it can absorb. The acquisition targets span the entire AI-infrastructure stack — RF components to fabrication to orbital compute — across a structural moat (reusable launch) that isn't easily competed away. The currency is already proven: the all-stock xAI merger and ~$60B Cursor deal show the machinery is live.

Where to Spend It: The Ranked Map

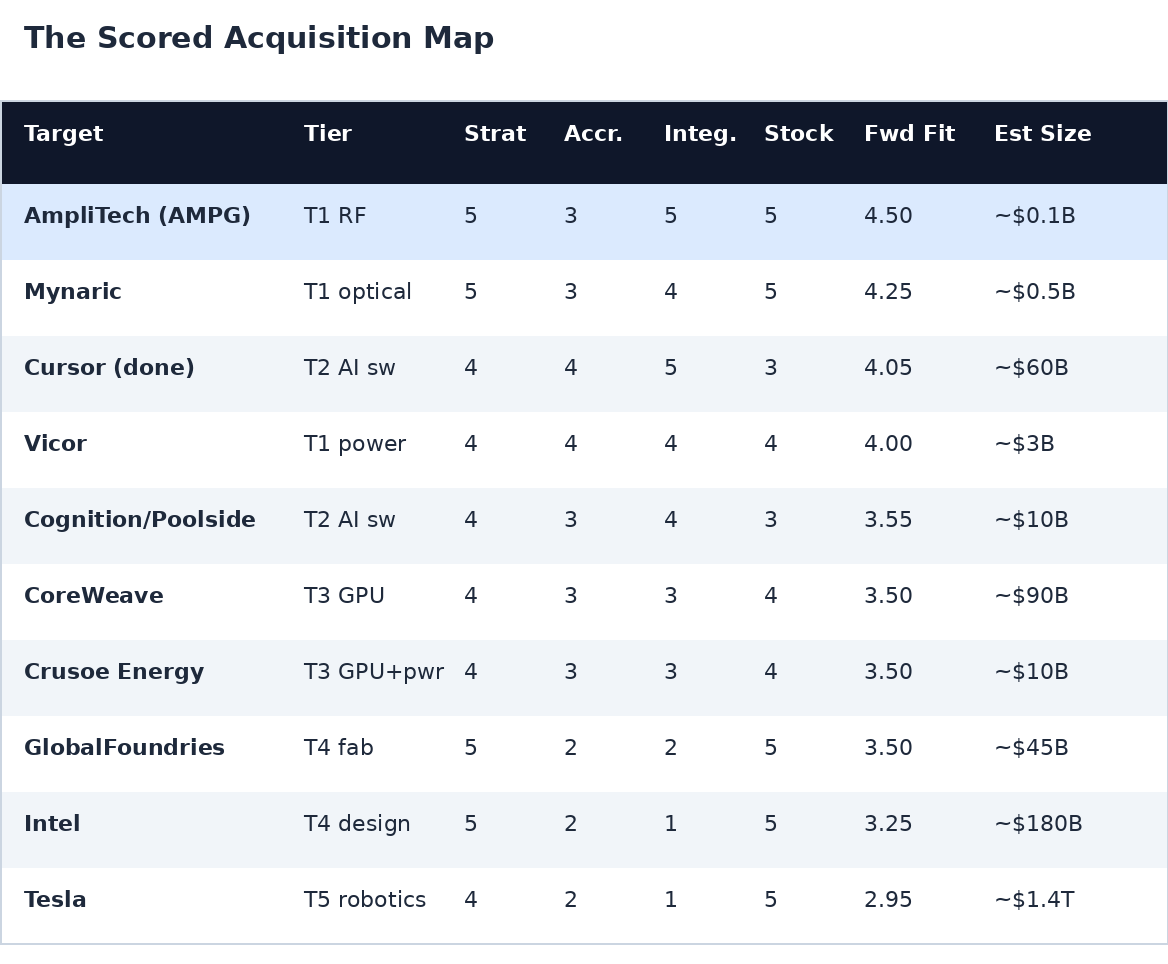

We scored ten named candidates on strategic fit, accretion, integration ease, and stock-deal fit (1–5, 5 = best; weighted 30/25/25/20). AmpliTech ranks first.

Scale: sub-scores 1–5 (5 = most favorable). Est size = approx. acquisition/market-cap scale.

The pattern is clear. Tier 1 dominates the top — small, vertically integrative supply-chain deals that amplify the core without straining it. AMPG leads at 4.50, maxing strategic fit, integration, and stock-deal fit; only accretion is capped because the value is capability, not current earnings. The silicon and robotics bets — GlobalFoundries, Intel, Tesla — score high on strategic fit but sink on accretion and integration risk. They belong on a separate track with different discipline.

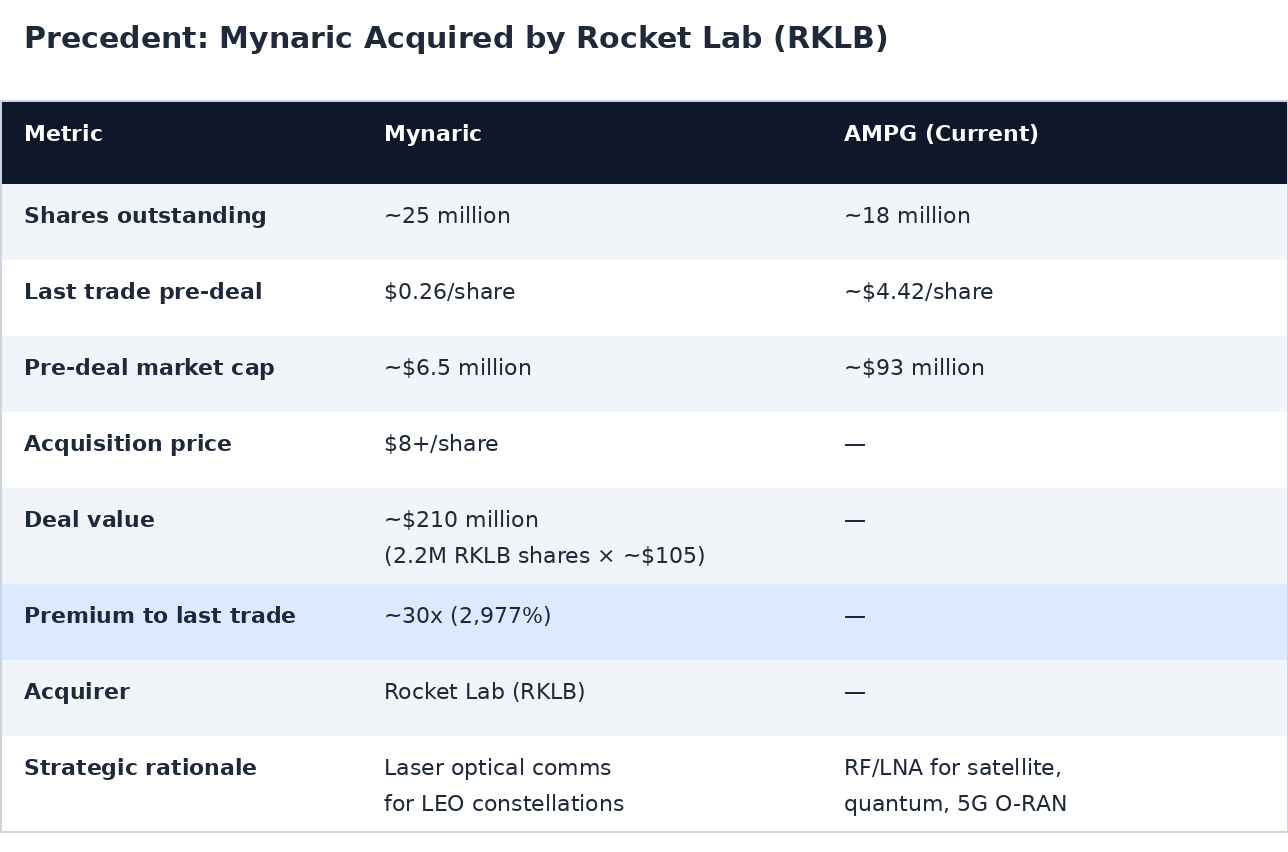

What Rocket Lab Just Proved About Space-RF Premiums

Before modeling AMPG deal terms, a real-world precedent landed. Rocket Lab (RKLB) acquired Mynaric — a laser optical communications company for LEO constellations — for approximately 2.2 million RKLB shares at ~$105/share, valuing the deal at roughly $210 million. Mynaric had ~25 million shares outstanding. Its last trade was $0.26.

The implied premium: ~30x the last traded price. Nearly 3,000%.

This isn't an outlier — it's the market telling you what strategically critical space hardware is actually worth to the right acquirer. And the parallels to AMPG are direct:

Same acquirer profile. A premium-multiple space company using its stock to absorb a micro-cap hardware supplier — the exact playbook this report recommends for SPCX.

Same strategic logic. Mynaric's laser comms are to Rocket Lab what AMPG's RF/LNA components are to SpaceX — physical-layer hardware the acquirer cannot do without and cannot efficiently build internally.

Same valuation dynamic. A company trading at a fraction of its strategic value gets re-rated through a blowout premium. If Rocket Lab paid ~30x last trade for Mynaric, what would SpaceX — with a currency 50x richer — pay for the only U.S.-domiciled supplier of space-grade cryogenic LNAs, 5G O-RAN radios, and satellite RF components?

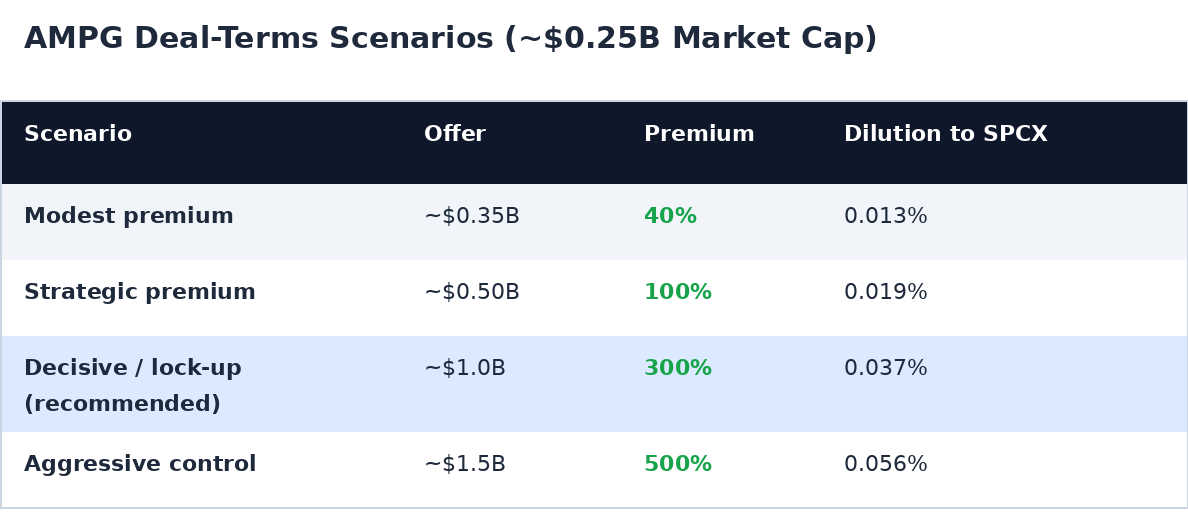

AMPG Deal-Terms: Pay Up for Critical Capability

AMPG trades at a ~$0.25B market cap. For a critical, irreplaceable capability, the decision should be driven by strategic necessity, not price — because even a $1B+ offer is a rounding error against SPCX's ~$2.7T value. The question flips from "what is AMPG worth?" to "what is control of this capability worth to SPCX?"

The case for paying up is straightforward:

The currency is free at the margin — trading paper valued at ~94x revenue for permanent, irreplaceable capability is pure multiple arbitrage. It pre-empts rivals and removes a supply dependency. A blowout premium guarantees closing — at AMPG's scale, a 300–500% premium is impossible to refuse and invisible on SPCX's cap table. And the Mynaric precedent validates the range: Rocket Lab paid ~30x last trade for a comparable space-hardware target. SPCX's recommended ~$1B offer (~4x AMPG's current cap) is, if anything, conservative by that standard.

Reserve price discipline for the large transformational deals — GlobalFoundries, Intel, Tesla — where dilution actually moves the needle.

Recommendation: lead with a decisive, all-stock offer for AMPG in the ~$1B range. The dilution is negligible (0.037%) and the capability is strategic.

The Honest Risks

This strategy is reflexive — it works only while the multiple holds, and the multiple is not guaranteed.

Damodaran estimates intrinsic value at ~$1.25–1.3T, below the current market price. The core is strained near-term: SPCX swung from a $791M profit in 2024 to a $4.9B loss in 2025 as capex nearly doubled to $20.7B, and xAI is dilutive, not yet accretive. And transformational deals can break the loop entirely — 1960s conglomerates and AOL–Time Warner are the cautionary tales of oversized, off-core deals collapsing the multiple that made them possible.

The discipline matters as much as the ambition. Which is why the recommendation is two separate programs: a repeatable bolt-on ladder where each deal is small enough to be invisible on the cap table, and a ring-fenced transformational track where a single focused fab deal (GlobalFoundries over Intel) is evaluated on its own merits with full diligence.

The Bottom Line

SPCX holds a position almost no public company has held at scale: a dominant, high-growth core paired with a currency so rich that acquiring critical capability costs essentially nothing in dilution. The window is real but finite — the multiple won't stay at 94x forever. The companies that used this window best — Cisco, Salesforce — defined their industries for decades. The ones that squandered it — or waited too long — watched the currency depreciate before they spent it.

Start with AMPG. Then the fab deal. Move while the currency is hot.

Disclosure: This report is prepared as strategic research. The authors hold positions in securities mentioned and reserve the right to buy or sell shares at any time without notice. Figures sourced from public filings, SPCX IPO prospectus and disclosures, and third-party analysis. Forward-looking statements and valuation scenarios are illustrative models based on stated assumptions, not forecasts. Not investment advice.