Stratasys (SSYS): A Transformational Defense and Commercial Drone Technology Play Through the SkyTech Replicator Partnership

March 25, 2026

IMPORTANT DISCLOSURE: This report contains the author's estimates, projections, and forecasts based on publicly disclosed information about the SkyTech-Stratasys manufacturing relationship. All revenue projections, timelines, and financial forecasts represent the author's analysis and should not be construed as guidance from Stratasys Ltd., SkyTech Orion Global Inc., or any affiliated parties. Actual results may differ materially from these estimates. The author holds positions in securities discussed in this report and reserves the right to buy or sell shares at any time without notice.

Executive Summary

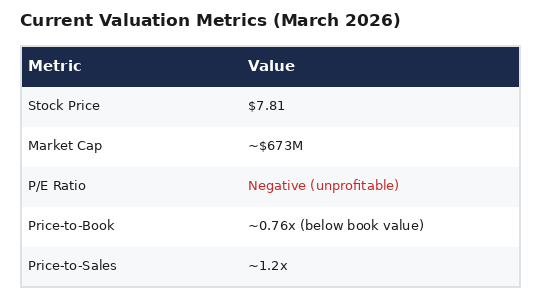

Stratasys Ltd. (NASDAQ: SSYS), currently trading at $7.81 per share with a market capitalization of approximately $673 million, is dramatically undervalued relative to the transformational manufacturing partnership disclosed by SkyTech Orion Global Inc. (OTC: CTGL, currently $0.05 per share). After years of stagnating revenue, persistent losses, and declining institutional investor confidence, the disclosed SSYS-SkyTech manufacturing arrangement for the Replicator line of advanced military and commercial drones represents a paradigm shift — not only in SSYS's business model but in how drones are manufactured globally.

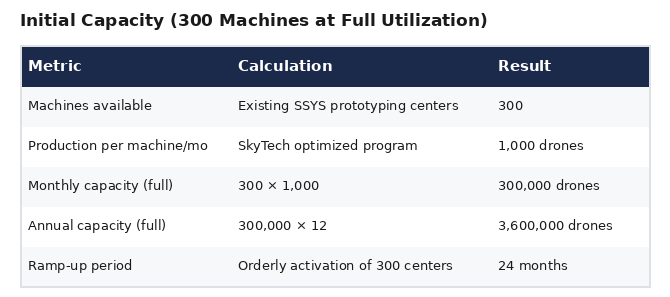

SkyTech has invented a revolutionary easy-manufacturing program that leverages Stratasys's existing global network of rapid prototyping centers to produce low-cost, modular drones at scale. Rather than requiring massive new capital expenditure for dedicated manufacturing facilities, this model activates approximately 300 existing Stratasys-equipped rapid prototyping centers worldwide, each capable of producing 1,000 drones per month per machine. This distributed manufacturing architecture — ramping to full capacity over 24 months — delivers initial annual capacity of 3.6 million drones per year with the ability to scale further as demand dictates, fundamentally addressing the global explosion in demand for low-cost tactical and commercial drones.

The SkyTech Replicator drone platform features:

- Ultra-lightweight construction: Total aircraft weight of only 2 lbs (well below FAA's 25 lb regulatory threshold)

- Modular "LEGO-style" snap-together design: Enabling one drone to serve multiple mission profiles through rapid field reconfiguration

- Dual-variant product line: Modular variant carrying up to 5 lbs payload; fixed FPV variant carrying up to 13 lbs

- High performance: 87 mph speeds, 12+ mile range, 15-inch enclosed propellers

- Near-term silent operation: CTGL possesses proprietary silent propulsion technology under its control and expected to deploy shortly

- Dual-use capability: Military reconnaissance/logistics and commercial last-mile delivery

We estimate that over a six-year forecast period, the SkyTech partnership will generate $1.46 billion in cumulative SSYS revenue and $804 million in cumulative profit at a blended 55.0% operating margin, transforming SSYS from a money-losing legacy 3D printing company into a high-margin defense and drone technology consumables business.

Timeline Clarification

Military Contracts (Near-Term Catalyst):

- First contract disclosures estimated: Within the next 3 months (by June 2026)

- Initial military contracts: Estimated to be awarded and executed over the first two years (2026-2028)

- Military scale-up to 1M annually: estimate for Year 3+ based on global tactical drone demand trends

Commercial Deployment (Forecast):

- Retail and commercial rollout: Forecasted to follow military validation; timing could be later than base case

- Regulatory advantage: Replicator's 2 lb aircraft weight + 5-13 lb payload = 7-15 lbs total, well within FAA's 25 lb limit, dramatically simplifying commercial certification

- Manufacturing advantage: SkyTech's easy-manufacturing program uses existing SSYS infrastructure globally — no new factory construction required

Price Targets

The Global Drone Demand Crisis: Why Low-Cost Manufacturing Matters Now

Unprecedented Military Demand

The global military drone market is experiencing explosive, unprecedented growth driven by lessons learned from modern conflicts. The military drone market is projected to reach $29.57 billion by 2030, with the tactical UAV segment alone worth $7.86 billion by 2030. Ukraine's drone production has surged 900%, with the country now producing 200,000 UAVs per month to meet battlefield consumption rates. The overall military drone market is projected to grow at a 7.5% CAGR through 2035, reaching $47.1 billion globally.

These staggering numbers reveal a fundamental truth: modern warfare consumes drones at rates that traditional manufacturing cannot sustain. Drones are now expendable tactical assets — used once, lost, damaged, or destroyed — requiring continuous mass production at low cost. The U.S. Department of Defense's Replicator initiative explicitly acknowledges this reality, seeking to field thousands of autonomous systems rapidly.

The small drones market alone is projected to reach $13.7 billion by 2036 as defense applications accelerate. This surge in demand creates an urgent need for manufacturing solutions that can scale rapidly without years of factory construction — precisely the problem SkyTech's easy-manufacturing program solves.

The Manufacturing Gap

The core problem facing every military and commercial drone buyer worldwide is manufacturing capacity. Traditional drone production relies on centralized factories with long supply chains, specialized tooling, and extended lead times. This model cannot scale to meet:

- U.S. military needs: Hundreds of thousands of tactical drones annually

- Allied nation demands: NATO members, Israel, Australia, Japan, South Korea all seeking mass drone procurement

- Commercial delivery requirements: Millions of drones annually for retail last-mile logistics

- Replacement cycles: Combat and commercial drones require constant replenishment

SkyTech's easy-manufacturing program, built on Stratasys's global rapid prototyping infrastructure, is the solution to this manufacturing gap.

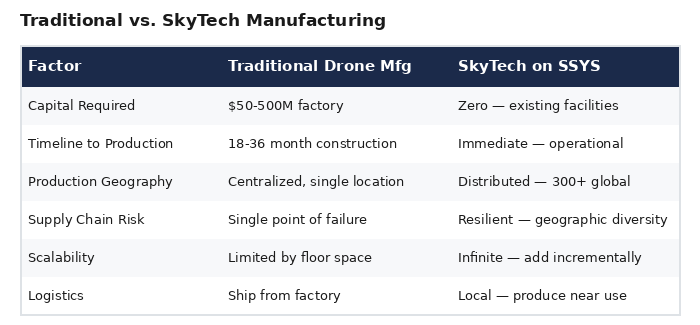

SkyTech's Revolutionary Easy-Manufacturing Program

The Innovation: Distributed Manufacturing on Existing Infrastructure

SkyTech Orion Global Inc. has developed a breakthrough manufacturing methodology that eliminates the traditional barriers to mass drone production. Rather than building new factories, SkyTech's program leverages the global installed base of Stratasys industrial 3D printers already operating in rapid prototyping centers, service bureaus, and manufacturing facilities worldwide.

How It Works:

- Software-Defined Manufacturing: SkyTech provides proprietary digital manufacturing files optimized for Stratasys printer platforms (FDM, PolyJet, SAF, P3). These files contain complete drone component designs, assembly instructions, and quality specifications.

- Existing Machine Utilization: Approximately 300 Stratasys-equipped rapid prototyping centers worldwide can be activated to produce Replicator drone components. These centers already have trained operators, material handling capabilities, quality systems, and shipping infrastructure.

- Capacity Per Machine: Each Stratasys industrial printer can produce components for 1,000 drones per month, leveraging the speed and reliability of SSYS's proven additive manufacturing platforms.

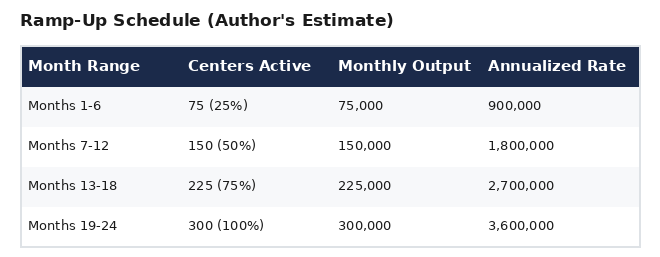

- Two-Year Ramp: The network ramps from initial activation to full capacity over 24 months, allowing orderly onboarding of centers, operator training on drone-specific production, and quality system validation.

- Scalable Architecture: Additional centers can be activated and new machines deployed as demand exceeds initial 300-machine capacity, creating a virtually unlimited production ceiling.

Why This Model Is Revolutionary

Production Capacity Analysis

Initial Capacity (300 Machines at Full Utilization):

Ramp-Up Schedule:

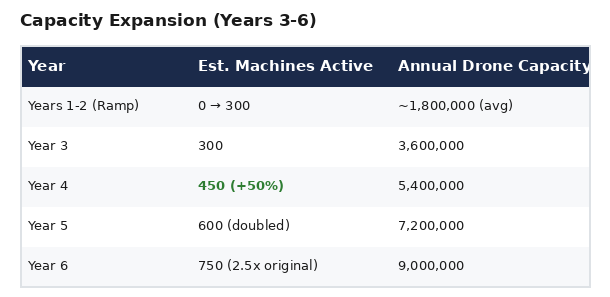

Capacity Expansion Beyond Initial 300 Machines (Years 3-6):

Product Overview: SkyTech Replicator Drone Specifications

Technical Specifications and Regulatory Compliance

Aircraft Weight and Regulatory Advantage:

- Base aircraft weight: 2 lbs (empty)

- Payload capacity:

- Modular LEGO-style variant: Up to 5 lbs

- Fixed FPV configuration: Up to 13 lbs

- Maximum takeoff weight: 7-15 lbs (aircraft + payload)

- FAA regulatory threshold: 25 lbs for commercial operations

- Compliance margin: 10-18 lbs below regulatory limit

This sub-25 lb total weight represents a critical competitive and regulatory advantage. The Replicator platform operates comfortably within existing FAA Part 107 commercial drone regulations without requiring special exemptions, waivers, or the multi-year certification processes that have delayed competitors. For comparison, Amazon's Prime Air MK30 drone weighs 80+ lbs and required 7+ years of FAA certification efforts. The Replicator's 2 lb aircraft weight makes it one of the lightest delivery-capable drones ever designed, enabling rapid regulatory approval across jurisdictions worldwide.

Performance Envelope:

- Maximum speed: 87 mph

- Range: 12+ miles

- Propulsion: 15-inch enclosed propellers

- Flight control: First Person View (FPV) capability for precision operation

- Payload enclosure: Fully enclosed for weather protection and safety

Acoustic Signature (Development Status):

Important Clarification: Current production Replicator units feature enclosed propellers that significantly reduce noise compared to open propeller designs, but are not yet truly silent.

However, CTGL has confirmed it possesses proprietary silent propulsion technology that is under its control and will be deployed to the Replicator line in the near term. Once implemented, this enhanced silent operation capability will provide:

- Enhanced military reconnaissance value (reduced acoustic detection)

- Improved urban commercial deployment (reduced noise complaints in residential delivery zones)

- Extended operational hours (ability to operate during night/early morning periods currently restricted by noise ordinances)

- Competitive differentiation vs. all current commercial delivery drones

The financial projections do not depend on silent technology deployment — the baseline Replicator platform remains viable for military and commercial use with its current reduced-noise enclosed propeller design.

Modular "LEGO-Style" Architecture

The Replicator line's defining innovation is its snap-together component system enabling rapid field reconfiguration:

- Tool-free assembly: Components connect via standardized interfaces without fasteners or specialized equipment

- One drone, multiple missions: A single Replicator unit can be reconfigured for reconnaissance (minimal payload, maximum range), delivery (up to 5 lb payload), communications relay (antenna package), or other mission profiles in minutes

- Field repair capability: Damaged components replaced individually rather than scrapping entire aircraft — a soldier can swap a broken arm or propeller assembly in under 60 seconds

- Simplified logistics: Standardized components reduce spare parts inventory from dozens of unique parts to a handful of universal modules

- 3D printable components: Every structural component producible on Stratasys machines, enabling forward-deployed manufacturing at military bases or commercial distribution centers

Dual-Variant Product Line

1. Modular LEGO-Style Variant:

- Payload capacity: Up to 5 lbs

- Total weight: ~7 lbs maximum (72% below FAA 25 lb threshold)

- Reconfigurable for multiple mission profiles

- Primary military use: Field soldier operations, tactical reconnaissance, small resupply

- Primary commercial use: Light package delivery (e-commerce, pharmaceutical, documents)

- Higher selling price due to modular versatility and multi-mission capability

2. Fixed FPV Configuration:

- Payload capacity: Up to 13 lbs

- Total weight: ~15 lbs maximum (40% below FAA 25 lb threshold)

- Optimized for single-mission high-payload operations

- Primary military use: Submitted to U.S. Army Drone Dominance procurement bid; heavy resupply, ISR with advanced sensor payloads

- Primary commercial use: Restaurant/grocery delivery, hardware delivery to job sites, heavier packages

- Streamlined for high-volume production and standardized training protocols

Historical Financial Performance: A Company in Need of Transformation

Revenue and Profitability (2021-2025)

Stratasys has experienced prolonged financial deterioration, marked by declining revenue and persistent operational losses.

Revenue Performance:

- 2021: $607.2 million

- 2022: $651.5 million (+7.3% YoY) — the peak

- 2023: $627.6 million (-3.7% YoY)

- 2024: $572.5 million (-8.8% YoY)

- 2025 (TTM est.): ~$545-555 million (continued decline)

Revenue has declined over $100 million (16%+) from 2022 peak to present. Q3 2025 revenue of $137 million showed a 2.1% year-over-year decline with GAAP gross margins compressing from 44.8% to 41.0%.

Profitability Crisis:

- 2021: Net loss of $62.0 million

- 2022: Net loss of $29.0 million

- 2023: Net loss of $123.1 million

- 2024: Net loss of $120.3 million

- Four-year cumulative net loss: Over $334 million

Stock Price: From $25 to $7.81

SSYS stock has experienced catastrophic value destruction:

- January 2022 high: ~$25.00

- January 2026: $10.32

- Current price (March 25, 2026): $7.81

- Market capitalization: ~$673 million

- Four-year decline: -69%

- YTD 2026 decline: -24% (from $10.32 to $7.81)

The continued erosion into 2026 reflects the market's persistent pessimism about SSYS's standalone prospects and creates an even more compelling entry point for investors who believe the SkyTech partnership will transform the company.

Current Valuation Metrics (March 2026):

Trading below book value signals the market assigns essentially zero value to SSYS's technology portfolio, brand, and global installed base of 300+ rapid prototyping centers — precisely the assets the SkyTech partnership monetizes.

Strategic Failures That Created the Opportunity

- Failure to develop high-volume applications: SSYS maintained technology leadership but never commercialized recurring-revenue applications beyond traditional prototyping. SkyTech's easy-manufacturing program is exactly the type of application SSYS should have developed internally.

- Margin compression: GAAP gross margins declined from 44.8% to 41.0% amid tariff headwinds and competitive pressure from low-cost Chinese manufacturers like Bambu Lab.

- Value-destructive acquisitions: The Ultimaker investment resulted in a $33.9 million impairment charge, exemplifying poor capital allocation.

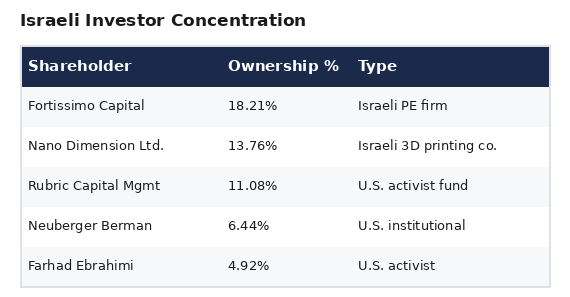

Institutional Ownership Exodus and Israeli Shareholder Concentration

Declining U.S. Institutional Support

Major U.S. institutional investors have systematically reduced SSYS positions over 2024-2025:

- RPG Investment Advisory: Cut position by 49.5%

- Primecap Management: Slashed holdings by 69.7%

- Legal & General Group: Reduced stake by 6.2%

- ARK Investment Management: Trimmed position by 15.9%

Israeli Investor Concentration

SSYS's ownership has shifted dramatically to Israeli investors:

Approximately 40%+ of SSYS is now controlled by Israeli investors, aligning perfectly with IDF procurement as a major customer for the Replicator program.

Fortissimo Capital's $120 Million Investment in February 2025 (11.65 million shares at $10.30) brought Israeli PE expertise to the board and growth capital to "seize market opportunities". Notably, Fortissimo invested at $10.30 — 32% above today's $7.81 price — signaling conviction that SSYS is materially undervalued.

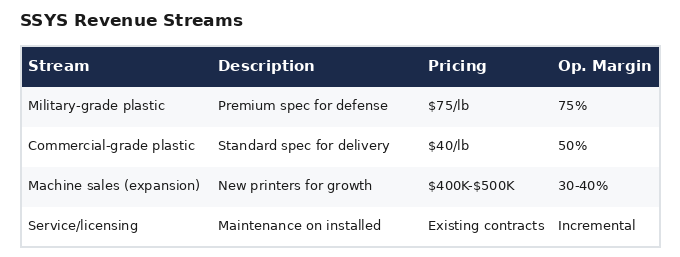

SSYS Revenue Model: Distributed Manufacturing Economics

How SSYS Monetizes the SkyTech Partnership

Under SkyTech's easy-manufacturing program, SSYS generates revenue primarily through proprietary plastic materials consumption — the classic high-margin consumables model.

Revenue Streams:

Per-Drone Economics (SSYS Portion Only):

- Revenue per military drone: $75 (1 lb of material)

- Profit per military drone: $56.25 (75% margin)

- Revenue per commercial drone: $40 (1 lb of material)

- Profit per commercial drone: $20.00 (50% margin)

Why Existing Infrastructure Eliminates Capital Requirements

The brilliance of SkyTech's easy-manufacturing approach is that SSYS does not need to build or deploy new machines for the initial 3.6 million annual drone capacity. The 300 rapid prototyping centers already exist, are already equipped with SSYS machines, already have trained operators, and already have quality systems and shipping infrastructure in place.

SSYS's incremental cost to activate drone production: Essentially zero capital expenditure — only the marginal cost of materials (25% of military pricing, 50% of commercial pricing).

This means the operating leverage is extraordinary: every dollar of materials revenue drops to the bottom line at 50-75% margins from Day 1, with no upfront factory investment, construction delays, or equipment procurement timelines.

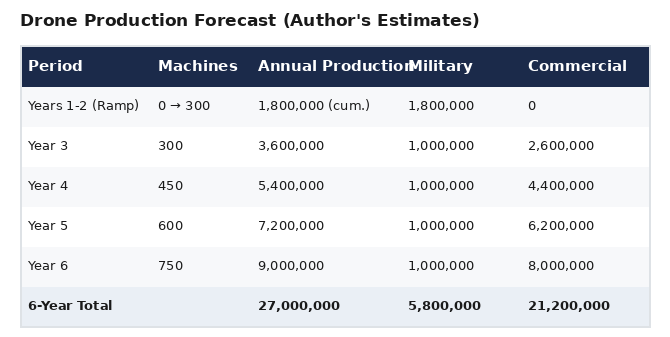

Consolidated Financial Forecast: Estimates (Years 1-6)

DISCLAIMER: All financial projections represent estimates based on disclosed partnership details and the distributed manufacturing model. These are NOT company guidance or commitments. Actual results may differ materially.

Drone Production Forecast

SSYS Materials Revenue and Profit Forecast

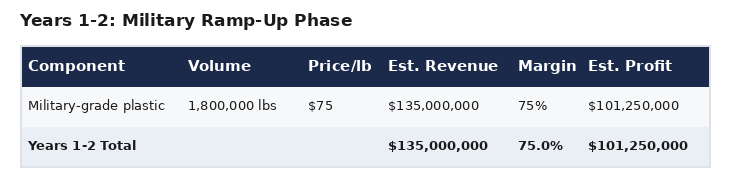

Years 1-2: Military Ramp-Up Phase

All production serves military contracts as the distributed manufacturing network is activated and validated:

Year 3: Full Capacity + Commercial Launch

Year 4: Expanded Capacity (450 Machines)

Year 5: Doubled Capacity (600 Machines)

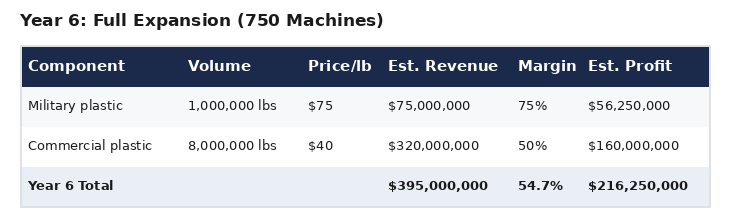

Year 6: Full Expansion (750 Machines)

Additional Machine Sales Revenue (Estimates)

As the network expands beyond 300 machines in Years 4-6:

Key Financial Highlights (Estimates):

- 6-Year Cumulative Revenue: $1.46 billion

- 6-Year Cumulative Profit: $804 million

- Blended Operating Margin: 55.0%

- Total Drones Manufactured: 27 million units

- Recurring Annual Revenue (Year 7+): $395+ million at 55% margins

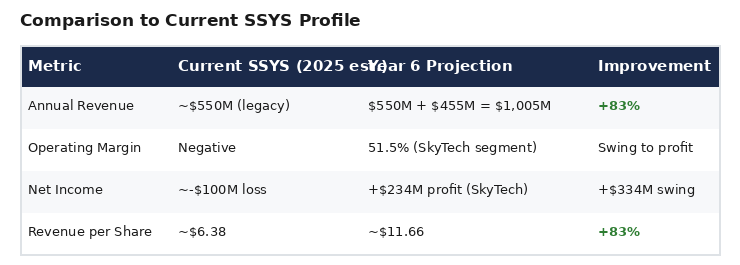

Comparison to Current SSYS Financial Profile

The SkyTech program alone generates more profit than SSYS's entire current revenue base, fundamentally transforming the company's financial character.

Stock Price Targets and Valuation Analysis

Current Valuation: Maximum Pessimism

As of March 25, 2026, both stocks trade at levels reflecting terminal decline or complete lack of recognition:

SSYS at $7.81 trades below book value, meaning the market assigns negative value to SSYS's technology, brand, patents, global customer relationships, and installed base of 300+ rapid prototyping centers. This represents maximum pessimism.

CTGL at $0.05 values SkyTech Orion Global at a fraction of a penny stock, reflecting the market's complete failure to recognize the transformational value of the Replicator drone technology and easy-manufacturing program. At $0.05, the market assigns essentially zero value to a company that has developed a patented modular drone platform with disclosed military and commercial applications and a manufacturing partnership with a NASDAQ-listed additive manufacturing leader.

SSYS Price Target Methodology

Price targets use P/E multiples applied to estimated EPS from the SkyTech partnership, assuming the market revalues SSYS from "distressed 3D printing vendor" to "defense/drone technology consumables supplier."

SSYS Price Targets

1-Year Target (Based on Year 4 Forecast):

- Estimated annual SkyTech profit: $162.3 million

- Combined with legacy business (breakeven assumed): $162.3 million net income

- Diluted shares: 86.2 million (current)

- Estimated EPS: $1.88

- Assumed P/E: 20x (conservative defense contractor multiple)

- 1-Year Price Target: $33.48

- Upside from $7.81: +329%

Rationale: A 20x P/E is conservative for a company with 50%+ margins and 80%+ profit growth. Defense contractors trade at 15-20x; drone specialists at 25-40x.

3-Year Target (Based on Year 6 Forecast):

- Estimated annual SkyTech profit: $234.3 million

- Legacy business recovery (assumed $20M contribution): $254.3 million net income

- Diluted shares: 90 million (modest dilution)

- Estimated EPS: $2.83

- Assumed P/E: 25x (growth premium for high margins + recurring revenue)

- 3-Year Price Target: $60.07

- Upside from $7.81: +669%

5-Year Target (Based on Steady State):

- Estimated steady-state annual profit: $200 million (recurring materials + modest machine sales)

- Diluted shares: 95 million

- Estimated EPS: $2.11

- Assumed P/E: 30x (50% multiple expansion for proven recurring model)

- 5-Year Price Target: $63.16

- Upside from $7.81: +709%

SSYS Price Target Summary

CTGL Valuation Context

At $0.05 per share, CTGL represents what we believe is an extraordinary disconnect between price and potential value. As the designer, IP holder, and licensor of the Replicator drone platform:

- CTGL collects license fees on every drone produced across the global SSYS manufacturing network

- CTGL retains all military and commercial drone selling price revenue beyond SSYS manufacturing costs

- CTGL holds the proprietary LEGO-style modular design patents

- CTGL possesses unreleased silent propulsion technology

- CTGL submitted the Replicator platform to the U.S. Army Drone Dominance bid

If the production estimates of 27 million drones over six years at a selling price of $5,000 (military) and lower commercial pricing materialize, the total addressable revenue for CTGL dwarfs its current micro-cap valuation by orders of magnitude. However, as an OTC-traded micro-cap, CTGL carries significant liquidity risk, regulatory risk, and execution risk that investors must weigh carefully.

Catalysts for Recognition

Near-Term (Next 90 Days)

- Military contract disclosures (estimated within 3 months): Official U.S. military or IDF contract awards naming SkyTech/SSYS

- SkyTech partnership formal announcement: Press releases detailing the manufacturing agreement scope and economics

- Q4 2025 / Q1 2026 SSYS earnings: Management commentary on new strategic partnerships

- Analyst initiation: Defense and aerospace analysts initiating Buy ratings on SSYS

Medium-Term (6-18 Months)

- First revenue recognition: Initial military drone materials revenue in SSYS financials

- Fortissimo position increase: 13F filings showing expansion toward 24.99% maximum ownership

- Silent propulsion deployment: CTGL integration of proprietary silent technology into production units

- Retail partner pilot announcements: Early commercial deployment confirmations

Long-Term (18-36 Months)

- Commercial rollout acceleration: Major retailer deployment beyond pilot phase

- International military contracts: NATO allies, Pacific partners adopting Replicator

- Production capacity milestones: Activation of 450+ machines demonstrating scalability

- Defense contractor reclassification: SSYS sector re-rating from industrial to defense technology

Investment Risks and Mitigating Factors

Forecast Risk (Most Critical)

ALL PROJECTIONS ESTIMATES. Actual results may differ materially.

- Military contracts timing: First contracts estimated within 3 months may be delayed or smaller

- Military scale-up: 1M annual volume by Year 3 is the estimate

- Commercial deployment timing: Could be delayed multiple years beyond base case

- Distributed manufacturing activation: 300-center ramp may take longer than 24 months

- Pricing and margin assumptions: Based on estimates of manufacturing economics

Technology Risk

- Silent operation: Not yet deployed. CTGL has confirmed it has the technology under its control for near-term deployment, but integration timeline is not guaranteed.

- Weight specifications: The 2 lb aircraft weight + 5-13 lb payload represents the understanding of current specs.

- Manufacturing quality: Distributed production across 300 centers requires consistent quality control.

Regulatory Risk

While Replicator's 7-15 lb total weight (well below FAA's 25 lb threshold) provides substantial regulatory advantages, commercial drone delivery faces FAA operational restrictions, local government opposition, airspace management challenges, and international regulatory variation.

Stock-Specific Risk

- SSYS has declined 69% over four years and 24% YTD 2026; further downside possible if partnership does not materialize

- CTGL at $0.05 is an OTC micro-cap with limited liquidity, wide bid-ask spreads, and heightened volatility risk

- Both stocks carry significant speculation embedded in the targets

- CTGL's OTC status means limited financial disclosure and regulatory oversight compared to NASDAQ-listed companies

Conclusion: Asymmetric Opportunity at Maximum Pessimism

Final Note: This report presents the analysis and estimates of how the SkyTech-Stratasys partnership, powered by SkyTech's revolutionary easy-manufacturing program utilizing SSYS's global rapid prototyping network of 300+ centers, could transform both companies. The near-term catalyst — military contract disclosures estimated within the next 3 months — provides a concrete validation opportunity.

At $7.81, SSYS trades below book value with the market pricing in zero value for the SkyTech partnership, zero value for the global manufacturing network, and zero value for a potential $1.46 billion revenue opportunity over six years.

At $0.05, CTGL is valued at essentially nothing despite holding proprietary drone IP, a manufacturing partnership with a NASDAQ-listed company, a submission to the U.S. Army Drone Dominance program, and unreleased silent propulsion technology.

If the military contract timeline and distributed manufacturing model prove accurate, and if commercial deployment proceeds even at a fraction of the forecasted pace, both stocks represent compelling asymmetric upside:

SSYS Price Targets from $7.81:

The SkyTech easy-manufacturing program solves the central problem facing the global drone industry — how to produce millions of low-cost drones annually without billions in factory investment. By leveraging SSYS's existing worldwide infrastructure, this distributed model delivers immediate capacity (3.6 million drones/year), infinite scalability, supply chain resilience, and extraordinary operating margins (50-75%) on recurring materials revenue.

For investors with appropriate risk tolerance, the combination of maximum pessimism pricing, near-term military catalysts, proven manufacturing infrastructure, and a proprietary drone platform operating well within regulatory weight limits presents what we believe is a rare asymmetric opportunity in both SSYS and CTGL.

Investment decisions should be based on individual risk tolerance and independent due diligence, not solely on the author's projections contained herein.