SpaceX (SPCX) — A Microsoft-Path Monopoly: The Starlink Direct-to-Device Thesis

Equity Research Report

IPO reference: $135/share (June 11, 2026) — the largest IPO in history

★ RECOMMENDATION: STRONG BUY ★

SpaceX (SPCX) — Reference $135 | Dramatically Undervalued vs. Perfect-Execution Value

Our conviction view. We rate SPCX a major BUY. We believe SpaceX will execute. Our perfect-execution scenarios imply a value many multiples above the $135 IPO reference, meaning the current price captures only a low-single-digit percentage of the franchise's modeled worth — a rare risk/reward profile that leaves enormous blue-sky upside still on the table.

Guiding principle: Never bet against a company that reuses its launch rockets. Reusability is the structural cost advantage that compounds every other layer of the thesis — launch, Starlink, direct-to-device, and the autonomous-machine connectivity frontier.

Executive Summary

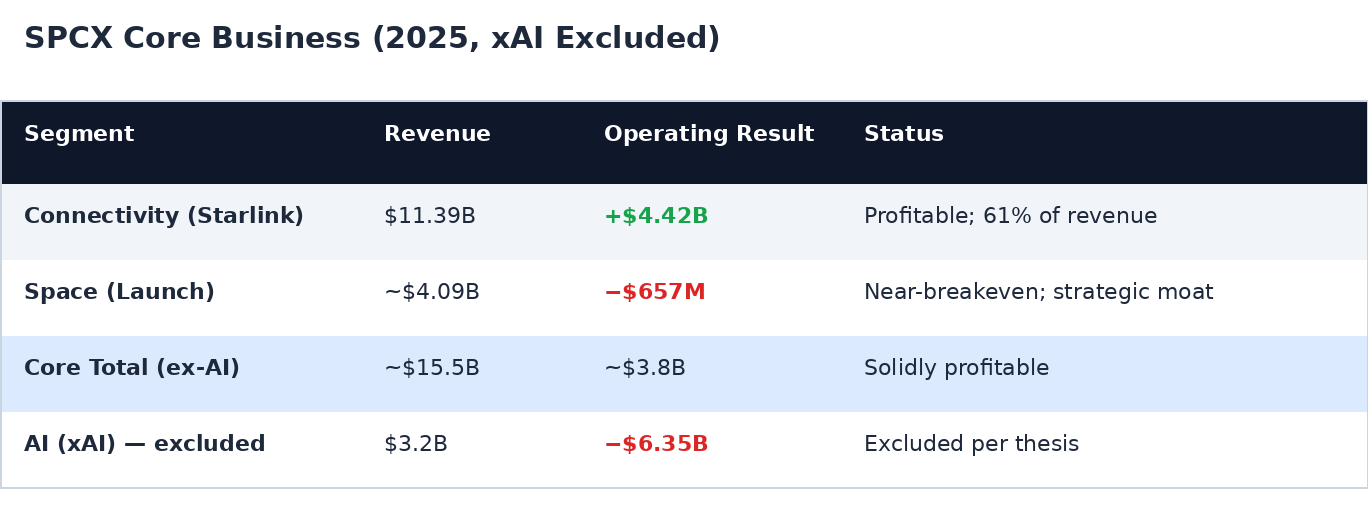

SpaceX completed the largest IPO ever on June 11, 2026, pricing 555.6 million shares at $135 to raise ~$75 billion at a ~$1.75 trillion valuation. Stripping out the loss-making xAI segment, the core Starlink + Launch business is profitable, dominant, and rapidly compounding.

Our thesis has two pillars:

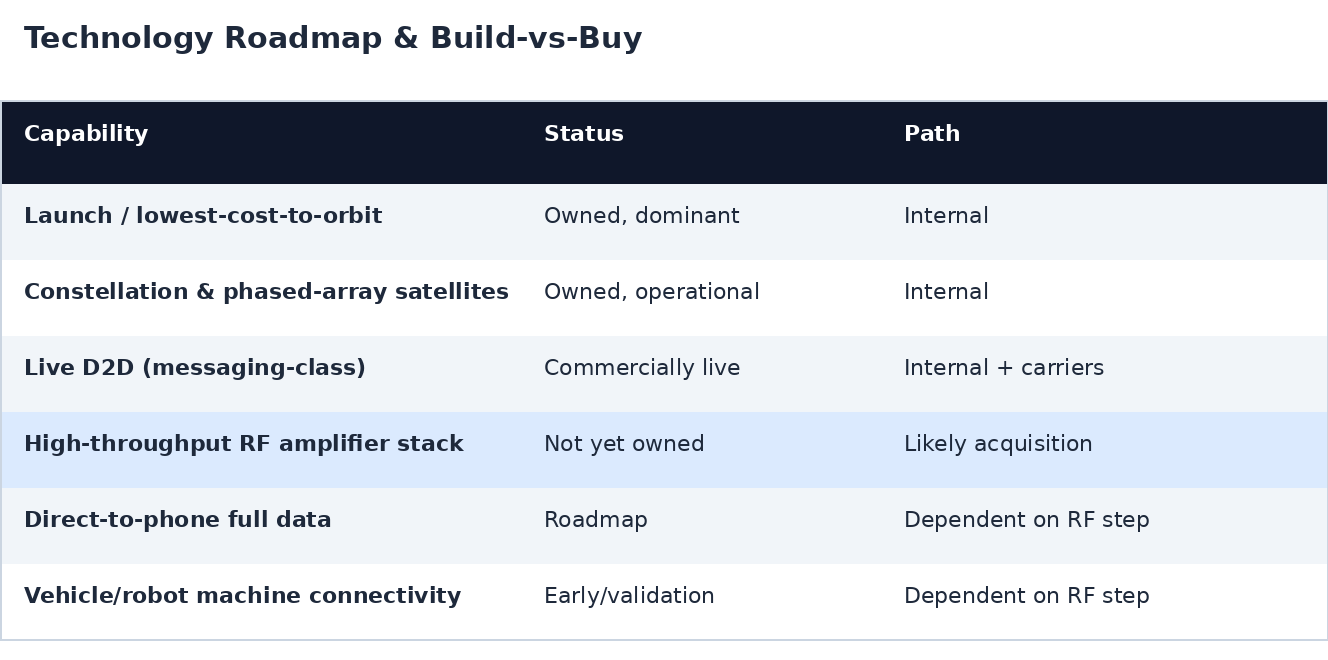

- The value engine is Starlink's direct-to-device (D2D) ladder — portable terminals today, direct-to-phone commercially live now, and autonomous vehicles and robots as the open-ended prize. The advanced RF amplifier technology required for the highest-throughput rungs is a stated future capability SpaceX expects to add, most likely via acquisition.

- This is a Microsoft-path monopoly. Any future antitrust action should resolve as Microsoft's did (survive intact, re-accelerate) rather than IBM's (erode by surrendering the next platform layer). Together these underwrite a TAM structurally larger than anything IBM or Microsoft commanded.

1. The Core Business Today (xAI Excluded)

Consolidated 2025 revenue was $18.7B (up 33%); the reported group net loss is driven entirely by xAI, not the core. Launch is the lowest-cost-to-orbit utility that makes Starlink possible — 74% of 2025 launches carried SpaceX's own satellites, a self-reinforcing flywheel.

2. The Value Engine — Starlink's Direct-to-Device Ladder

Rung 1 — Portable devices (today)

Starlink Mobile already delivers broadband to portable terminals using large phased-array antennas on the V2 satellites (20x prior traffic capacity). The advanced RF amplifier technology for full high-throughput D2D is a stated future capability SpaceX expects to add — most likely through acquisition rather than internal development — an execution and capital-allocation step not yet in hand.

Rung 2 — Direct-to-phone (commercially live)

Starlink Direct to Cell received FCC commercial approval in Nov 2024; T-Mobile launched T-Satellite commercially on July 23, 2025. It works on unmodified existing smartphones (~60 models), with the satellites acting as "cell towers in space." Available in 100+ countries; service is messaging-class today, with a text → voice → full-data roadmap as the constellation densifies.

Rung 3 — Autonomous vehicles and robots (the large prize)

The FCC authorized Starlink on vehicles in motion in 2022; low-latency LEO connectivity is already applied to autonomous-vehicle safety, and research platforms now mount Starlink on mobile robots. As autonomy scales, every self-driving vehicle and mobile robot becomes a potential always-connected endpoint — a device class that dwarfs the human-handset market.

2a. Technology Roadmap & Build-vs-Buy

The build-vs-buy decision on the RF layer is the single most important near-term execution catalyst: it gates the transition from messaging-class D2D to the high-throughput service that unlocks the vehicle and robot rungs.

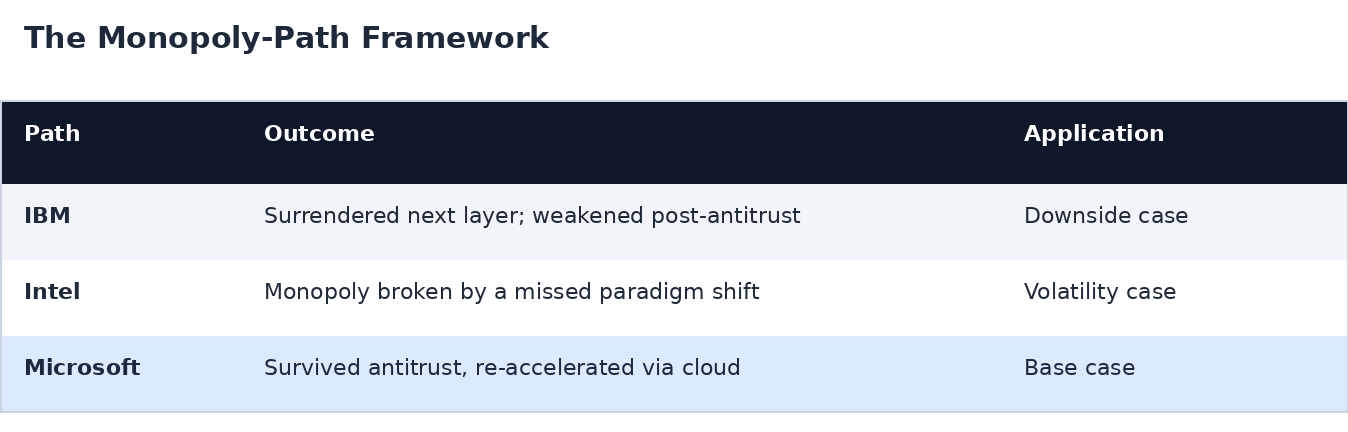

3. The Monopoly-Path Framework

IBM dominated ~70% of mainframes and once represented ~6.7% of the entire U.S. stock market, yet eroded after handing away the PC's platform layers. Intel rode x86 to ~$509B (2000) before disruption. Microsoft alone weathered antitrust and re-platformed onto cloud. The decisive variable across all three was platform control — not the lawsuit outcome.

4. Why Antitrust Resolves the Microsoft Way

- Intends to control the next layer — likely by acquisition. SpaceX owns launch, constellation, and network layers and intends to extend control into the RF/device layer via acquisition — Microsoft's pattern of buying into the next layer rather than surrendering it as IBM did (a forward commitment, not yet complete).

- The remedy problem favors the incumbent. The 13-year DOJ case against IBM produced no conviction; the Microsoft case ended in settlement, not breakup. A vertically integrated space network is even harder to unwind.

- Consumer-welfare framing is favorable. D2D eliminates dead zones via existing phones — a clear consumer benefit supporting a "dominant but pro-consumer" defense.

- Open, standards-based interconnection. D2D runs on 3GPP non-terrestrial-network standards and partners with carriers (e.g., T-Mobile) rather than displacing them.

- National-strategic indispensability. With five of six U.S. launches dependent on SpaceX, government is incentivized to regulate rather than dismantle.

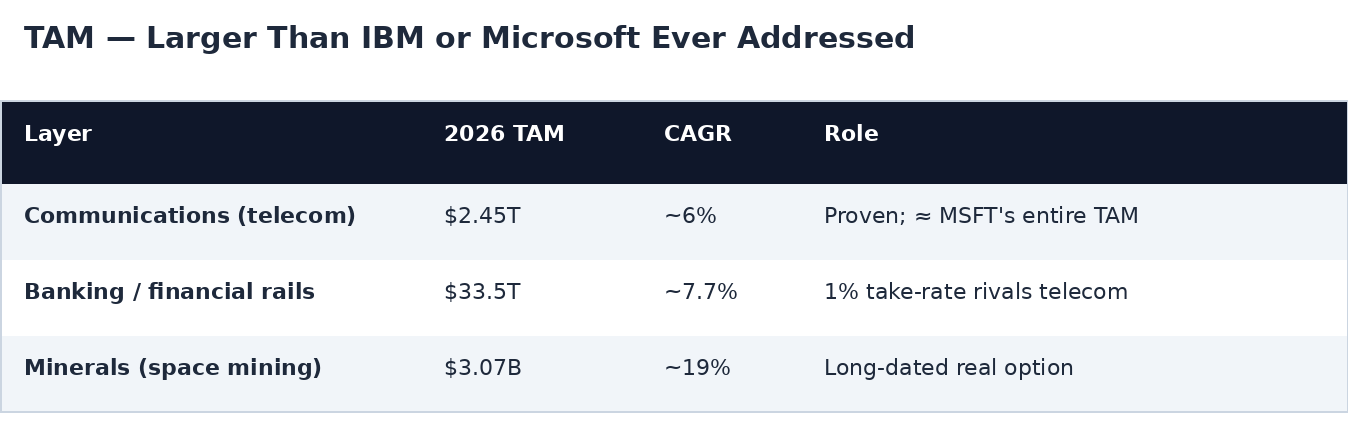

5. TAM — Larger Than IBM or Microsoft Ever Addressed

SpaceX's S-1 frames a combined TAM of $28.5 trillion, versus the ~$1–3 trillion markets IBM and Microsoft commanded at their peaks.

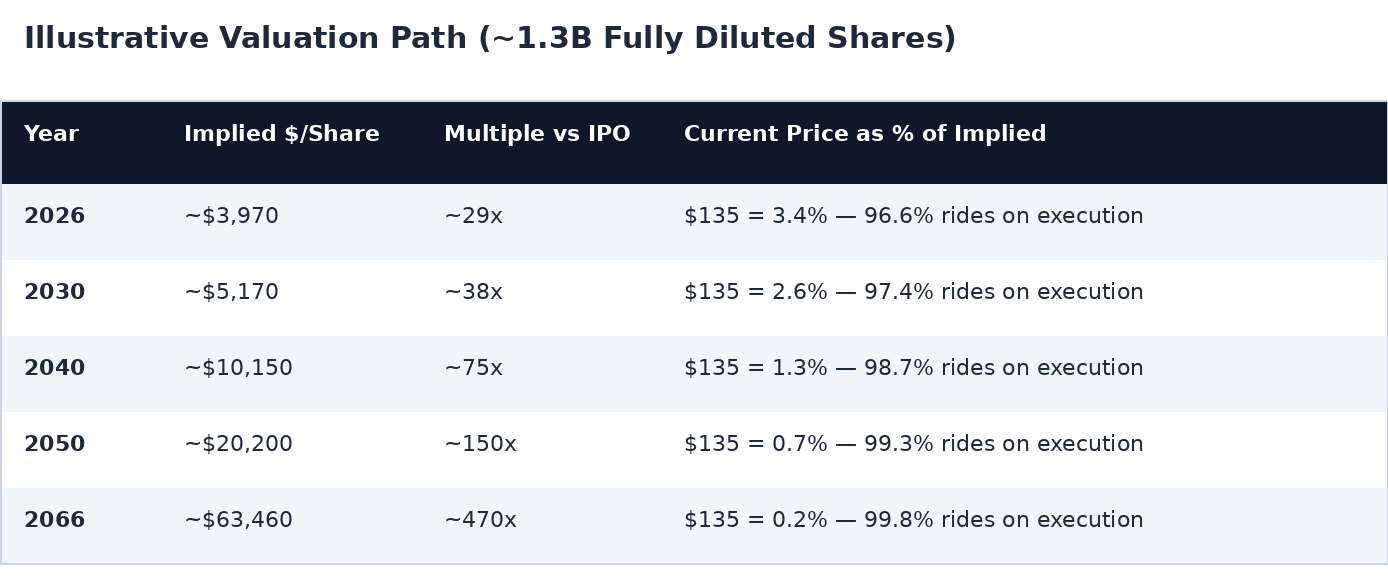

6. Illustrative Valuation Path (Scenario, Not Forecast)

Layer-specific revenue multiples (comms 4x, banking 8x, minerals 3x) applied to modeled TAM capture, off the $135 IPO across ~1.3B fully diluted shares:

Interpretive note. The current $135 reference price represents only a low-single-digit percentage of each year's implied value, falling toward zero over time. Virtually the entire modeled return is contingent on great execution — none of it is "in the price" today. Closing the gap requires three sequenced milestones: (1) securing the high-throughput RF amplifier capability (build-vs-buy acquisition); (2) advancing direct-to-phone from messaging to full voice/data at scale; and (3) converting the autonomous-vehicle and robot connectivity layer from validation into monetized endpoints. We view this gap not as a warning but as the opportunity: the market currently prices SpaceX below even the IPO level (Morningstar fair value ~$63), leaving extraordinary blue-sky upside if — as we expect — the company executes.

7. Key Risks

- RF technology dependency. The high-throughput RF amplifier capability is not yet owned; likely acquisition introduces cost, integration, and competitive-bidding risk before the largest TAM rungs monetize.

- Valuation gap. Morningstar fair value ~$63/share — under half the $135 IPO — implying ~67x sales, three times Nvidia's multiple.

- ARPU compression. Starlink ARPU fell from $99 (2023) to $66 (Q1 2026); volume must outrun price erosion.

- Regulatory/spectrum dependence. D2D needs ongoing FCC and international spectrum approvals and carrier partnerships.

- Government dependence. Heavy reliance on federal launch contracts creates procurement and political exposure.

Conclusion

SpaceX is a profitable, dominant connectivity franchise whose value engine is the Starlink direct-to-device ladder, underwritten by a stable, dominant launch business. The advanced RF amplifier technology for the highest-throughput rungs is a stated future capability SpaceX will most likely acquire, making the build-vs-buy step the key near-term catalyst. Benchmarked against history, SpaceX most resembles Microsoft, not IBM or Intel: we believe future antitrust resolves the Microsoft way because SpaceX intends to control each successive platform layer, operates on open interconnection standards, delivers clear consumer benefits, and is strategically indispensable. The combined communications-plus-financial-rails TAM is structurally larger than anything either predecessor commanded, with space minerals as a long-dated free option.

★ RECOMMENDATION: STRONG BUY ★

SpaceX (SPCX) — Reference $135 | Dramatically Undervalued vs. Perfect-Execution Value

Our conviction view. We rate SPCX a major BUY. We believe SpaceX will execute. Our perfect-execution scenarios imply a value many multiples above the $135 IPO reference, meaning the current price captures only a low-single-digit percentage of the franchise's modeled worth — a rare risk/reward profile that leaves enormous blue-sky upside still on the table. The price-versus-implied-valuation gap is not a warning — it is the opportunity: the market is offering this franchise far below its execution-adjusted worth, and we are buyers.

Guiding principle: Never bet against a company that reuses its launch rockets.

Disclosure: This report is for informational purposes only and does not constitute investment advice, a recommendation, or an offer to buy or sell any security. The authors hold positions in securities mentioned and reserve the right to buy or sell shares at any time without notice. Forward-looking statements and valuation scenarios are illustrative models based on stated assumptions, not forecasts. Recipients should conduct independent due diligence and consult their own advisors. Figures derive from SpaceX's S-1, public filings, and third-party sources cited herein.

Sources: SpaceX S-1 and IPO disclosures; FCC filings; T-Mobile/Starlink announcements; third-party market research and reporting as cited.