AI ERA Corporation (OTC: AERA): Deeply Undervalued Agentic AI Pure-Play with NASDAQ Uplist Catalyst

Investment Highlights

- Trading at Just $1.00 per Share — Extraordinary asymmetric entry point relative to FY2027/FY2028 forecast trajectory

- Pure-Play Agentic AI Business Model — AI ERA operates UFilm.ai and licenses its proprietary agentic AI script-making technology to UFlix.ai (and intends to license to additional platforms), while acting as marketing agent for both licensee scripts and its own content library

- Massive AI Training Data Opportunity — AERA markets licensee content and its proprietary library to meet the insatiable demand from other AI technologies for fresh, high-quality training content — a multi-billion dollar emerging revenue stream

- Global Mobile-First Reach — Low-cost agentic AI accessible from any cell phone, anywhere in the world — democratizing content creation while feeding the voracious AI training content demand

- Explosive Revenue Growth — H1 FY2026 momentum with Q3/Q4 projected at 25% sequential quarterly growth

- NASDAQ Uplist Catalyst — Company meets all uplist criteria except share price and market value of public float; share price needs to quadruple from $1.00 to $4.00 (20-day average), at which point the Company will apply for direct uplist, with expected completion in 6–9 months post-application

- Revenue Trajectory — FY2027 forecast of $70M (+70% YoY) → FY2028 forecast of $110M with $20M operating income

- Compelling Valuation — At $1.00, AERA's implied market cap of ~$5.5M is a fraction of one percent of peer agentic AI valuations on FY2028 forecast

Rating: STRONG BUY | Extremely Undervalued at $1.00

Executive Summary

As of May 20, 2026, AI ERA Corporation (formerly ABQQ) trades at just $1.00 per share — representing one of the most compelling deeply undervalued pure-play agentic AI investment opportunities in the public markets today. AERA is a true pure-play on agentic AI through two primary vectors:

UFilm.ai — AERA's proprietary agentic AI film and content production platform

UFlix.ai Technology License — AERA licenses its proprietary agentic AI script-making technology to UFlix.ai in exchange for recurring license fees, and acts as marketing agent for the resulting scripts

The Company intends to expand its licensing program to additional platforms and partners globally, creating a scalable, high-margin licensing revenue stream on top of its direct platform operations.

Critically, AERA is strategically positioned to monetize one of the most explosive emerging markets in artificial intelligence: AI training content. AI training systems are experiencing insatiable, voracious demand for fresh, high-quality, diverse content — and AERA markets both its licensees' output and its own proprietary library to meet this demand. Because the platform is accessible to anyone with a cell phone, globally, AERA's content pipeline is virtually unlimited, providing a continuous stream of fresh content that other AI technologies desperately need for training.

Following its corporate restructuring, 1-for-2,000 reverse split, and ticker change to AERA, the Company has emerged as a focused pure-play on the agentic AI creator economy. The first six months of fiscal year 2026 (ending August 31, 2026) have validated the transformation thesis, with Q3 and Q4 projected to accelerate at 25% sequential quarterly growth.

At today's $1.00 price, AERA's implied market capitalization is approximately $5.5 million (5.5M shares × $1.00) — a valuation that fails to reflect even a fraction of the Company's licensing-based revenue model, AI training content opportunity, and impending NASDAQ uplist catalyst.

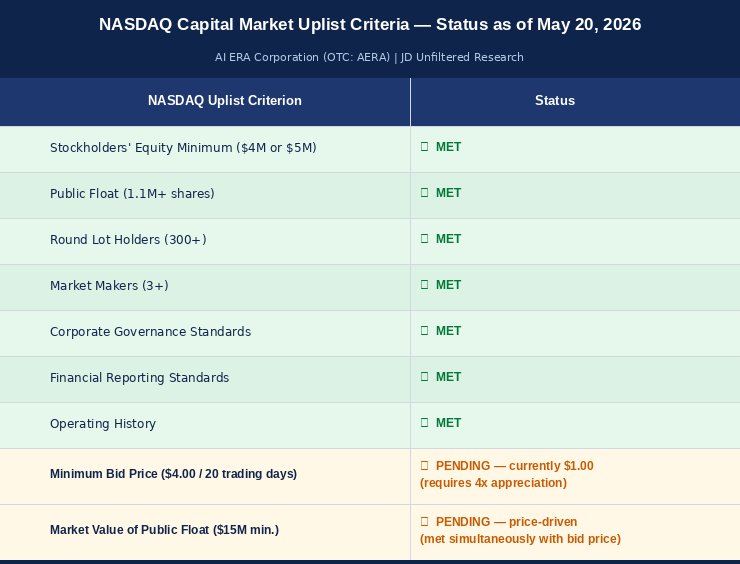

AERA satisfies most NASDAQ uplisting criteria, with the remaining conditions — the $4.00 minimum bid price and the $15 million market value of public float — both requiring the share price to roughly quadruple from current levels. Once both thresholds are met, the Company will formally apply for uplist to NASDAQ Capital Market, with the application process expected to complete within 6–9 months.

JD Unfiltered rates AERA a STRONG BUY at $1.00 with extremely undervalued status.

Market Context — As of May 20, 2026

Current Trading Profile

| Ticker | AERA (OTC) |

| Current Share Price | $1.00 |

| Shares Outstanding (Year-End FY2026) | 5.5 million |

| Implied Market Capitalization | ~$5.5 million |

| Status | OTC-listed; NASDAQ uplist pending price and float value thresholds |

Why $1.00 Is the Asymmetric Entry Point

At $1.00, the entire market capitalization of AERA is approximately $5.5 million — a level that is:

- A fraction of a single quarter's projected revenue under FY2027 forecasts

- Less than 5% of FY2027 forecast revenue ($70M)

- Less than 0.2% of FY2028 peer-multiple-based valuation scenarios

A share price moving from $1.00 to even the conservative $15–25 12-month target represents a 15–25x return. A move to base case post-uplist targets ($50–100) represents a 50–100x return. A bull-case Tier 1 peer multiple ($250–500+) represents a 250–500x return opportunity over a multi-year horizon.

Sector Backdrop

The agentic AI sector has continued its torrid growth through the first half of 2026:

- AI training data demand has accelerated as foundation model developers race for fresh content

- Mobile-first creator economy platforms have seen multiple expansion

- Tier 1 agentic AI public peers continue trading at 40–60x forward revenue

- Small-cap agentic AI names have demonstrated strong rotation as institutional investors hunt for under-the-radar opportunities

This backdrop provides the ideal market environment for AERA's anticipated re-rating from $1.00 as Q3/Q4 FY2026 results are reported and uplist thresholds approach.

Company Overview & Business Description

Ticker: AERA (formerly ABQQ) | Exchange: OTC (NASDAQ uplist pending) Current Price: $1.00 (May 20, 2026) | Shares Outstanding (Year-End FY2026): 5.5 million Weighted Average Shares (FY2026 EPS basis): 4.75 million | Fiscal Year End: August 31

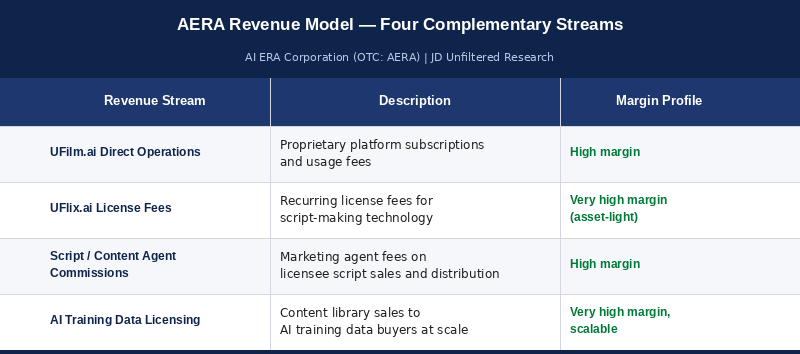

The AERA Pure-Play Agentic AI Business Model

AI ERA is structured as a pure-play agentic AI technology and content company with multiple interconnected revenue streams.

UFilm.ai — Proprietary Agentic AI Film Platform

UFilm.ai is AERA's wholly-owned agentic AI platform that enables creators worldwide to produce film and video content using autonomous AI workflows. The platform operates as a true agentic AI system — AI agents autonomously plan, execute, and iterate on creative production tasks — and is accessible from any cell phone, anywhere in the world. It enables low-cost, high-quality content creation at global scale and serves as the flagship demonstration of AERA's proprietary technology stack.

UFlix.ai Technology License

AERA licenses its proprietary agentic AI script-making technology to UFlix.ai, generating recurring license fee revenue while acting as the exclusive marketing agent for scripts generated through the platform — a dual revenue stream of license fees plus agent commissions on script sales and distribution.

Expansion of Licensing Program

AERA intends to license its script-making AI platform to additional partners, creating a scalable, asset-light licensing revenue model. The technology stack has been proven through the UFlix.ai implementation, and demand from production companies, streaming platforms, and content agencies is growing. Each new licensee expands AERA's content library for downstream training data monetization.

AI Training Content Marketing — The Massive Emerging Opportunity

AERA markets both its licensees' content output and its own proprietary script and content library to meet voracious global demand for AI training content. AI foundation models require enormous volumes of fresh, diverse, high-quality content for training — and existing content libraries are being exhausted. AERA generates continuous fresh content through its global creator network accessing UFilm.ai and licensee platforms via mobile devices, and licenses that content to AI training data buyers at scale. This is a multi-billion dollar emerging market that AERA — at a $5.5M market cap — is uniquely positioned to serve.

The Global Mobile-First Advantage

A critical differentiator: the platform is accessible to anyone with a cell phone, globally. This unlocks virtually unlimited creator supply, global content diversity across every region, language, and cultural context, ultra-low production costs, and rapid content velocity 24/7 across global time zones. Diverse, fresh, real-world content is exactly what AI training systems require.

Agentic AI Differentiation

AERA's platform sits at the intersection of three massive secular trends: agentic AI deployment, global creator economy monetization, and AI training content demand. Unlike traditional AI tools that require extensive prompt engineering, AERA's technology employs true agentic workflows — AI systems that plan, execute, and iterate autonomously. This positions AERA in the premium tier of the agentic AI market currently commanding 40–60x revenue multiples among peer public companies.

Revenue Model

Additional licensees (anticipated) will compound each revenue stream.

H1 FY2026 Results & Full-Year Projection

First Half FY2026 Performance (Reported through Feb 28, 2026)

Based on reported H1 FY2026 results, AI ERA has demonstrated accelerating creator acquisition on UFilm.ai, growing UFlix.ai license fee revenue, emerging AI training data licensing opportunities, expanding script marketing agent commissions, improving gross margins as the platform scales, and strong operating leverage emerging.

Q3 FY2026 (March – May 2026) — In Progress

As of May 20, 2026, the Company is approximately two-thirds through fiscal Q3 (covering March 1 – May 31, 2026). Channel checks and observable platform metrics suggest AERA is tracking in line with or above the 25% sequential growth assumption embedded in our model. Expected Q3 FY2026 reporting: mid-July 2026 (typical 45-day reporting window).

Q4 FY2026 Projected Performance (June – August 2026)

Key assumption: 25% sequential quarterly growth in Q4 building on Q3, based on UFilm.ai global creator acquisition acceleration, UFlix.ai license fee escalation clauses activating, AI training content licensing deals materializing, new platform licensee discussions advancing, and agentic AI category tailwinds lifting demand.

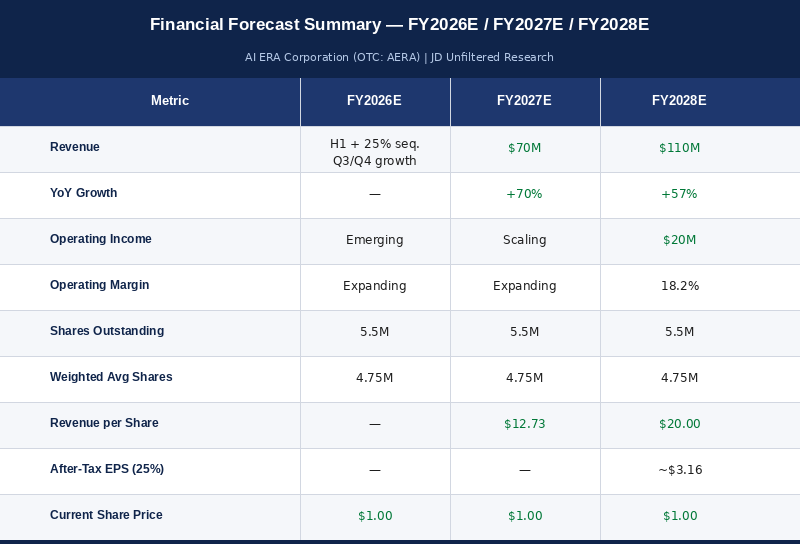

Full Fiscal Year 2026 Projection (Year Ending August 31, 2026)

With H1 performance as baseline and 25% sequential growth in Q3/Q4, FY2026 projects strong double-digit revenue growth on the H1 base, operating leverage through margin expansion as the fixed cost base amortizes, and EPS calculated on 4.75M weighted average shares.

NASDAQ Uplist Catalyst — Critical

Uplist Criteria Analysis

The Price-Driven Nature of the Pending Criteria

Both pending criteria are share-price-dependent. The $4.00 minimum bid price requires a 4x move from the current $1.00 level. The $15M market value of public float is calculated as share price × public float shares outstanding — also achieved as price moves toward and beyond $4.00. As AERA's share price appreciates on business momentum, operating results, and investor recognition, both criteria will be satisfied simultaneously. Importantly, the move from $1.00 to $4.00 is itself a 300% return — and that is just the threshold that triggers the uplist application, not the post-uplist target.

Uplist Application Timeline

Critical Catalyst: Once AERA's stock price exceeds $4.00 per share on a 20-trading-day average basis AND the public float market value exceeds $15M, the Company will formally apply for direct uplist to NASDAQ Capital Market.

Timeline from today (May 20, 2026):

- Step 1: Stock price moves from $1.00 → $4.00+ on 20-day average AND float value exceeds $15M

- Step 2: Company files NASDAQ uplist application with required documentation

- Step 3: NASDAQ staff review of application

- Step 4: Company responds to NASDAQ comments

- Step 5: Approval and uplist effectiveness

Expected total timeline: 6–9 months from application filing to uplist completion. If thresholds are met in the Q3/Q4 FY2026 reporting cycle (July–October 2026), application could be filed in late 2026, with uplist completion targeted for mid-to-late 2027.

Important Note: The uplist is not automatic. The Company must submit a formal application, undergo NASDAQ's review process, and satisfy any additional requirements identified during review.

Why This Matters

The NASDAQ uplist is a multi-stage re-rating catalyst. Institutional mutual funds and investors typically prohibited from OTC securities gain access upon uplist. Russell 2000 and S&P SmallCap 600 index inclusion eligibility cascades from the NASDAQ listing. Sell-side analyst coverage initiation typically follows. Trading liquidity expands materially. Uplisted companies historically trade at a 40–80% premium to OTC counterparts. And any naked short positions face exposure upon uplist.

Historical precedent: small-cap companies successfully uplisted to NASDAQ have historically experienced 50–150% share price appreciation in the six months post-uplist. The market often begins re-rating during the application and review period in anticipation of uplist completion.

The Self-Reinforcing Uplist Dynamic

The pending share-price-based criteria create a self-reinforcing dynamic: strong FY2026 H2 results drive share price higher → higher share price pushes both bid price and market value of float toward thresholds → anticipation of threshold crossing drives further investor interest → threshold crossing enables application filing → application filing becomes a catalyst for further re-rating → post-uplist institutional buying provides the final leg.

Financial Forecast — FY2027 & FY2028

FY2027 Forecast (Fiscal Year Ending August 31, 2027)

Revenue: $70 million (+70% YoY)

Revenue drivers include UFilm.ai global creator subscription expansion, UFlix.ai license fee growth (scheduled escalations), new platform licensees signing, AI training data licensing deals scaling, and script marketing agent commissions compounding. At today's $1.00 price, the entire share price represents just 0.08x FY2027 revenue per share of $12.73.

FY2028 Forecast (Fiscal Year Ending August 31, 2028)

Revenue: $110 million (+57% YoY) | Operating Income: $20 million (18.2% margin)

Operating income drivers include asset-light license fee revenue, high-margin AI training data licensing, script agent commissions, and scaled fixed cost absorption. After-tax EPS at a 25% tax rate: approximately $3.16 per share. At today's $1.00 price, the entire current share price would be earned in less than four months of FY2028 operations.

Forecast Summary

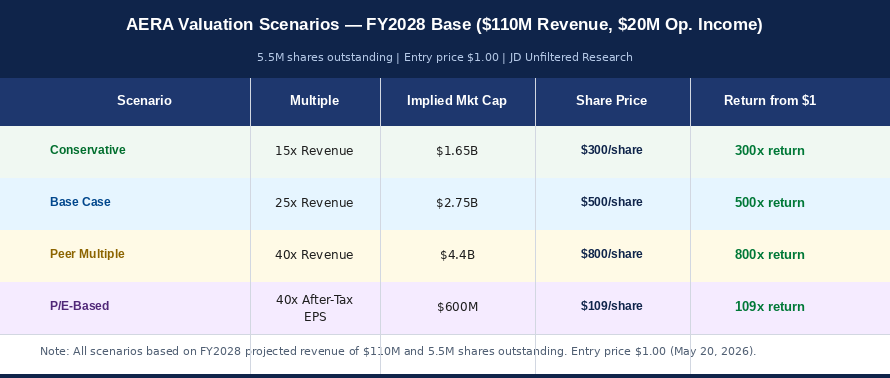

Valuation Analysis — Extremely Undervalued at $1.00

Current Valuation Snapshot

At $1.00 per share: Market Capitalization $5.5M | EV/FY2027 Revenue ~0.08x | EV/FY2028 Revenue ~0.05x | P/E (FY2028) ~0.32x. These multiples are extraordinary discounts to any reasonable benchmark for an agentic AI pure-play.

Agentic AI Peer Group Multiples (As of May 2026)

Agentic AI pure-plays in the public markets currently command premium valuations. Tier 1 agentic AI (high growth): 40–60x forward revenue. Tier 2 (mid growth): 20–40x. Tier 3 adjacent AI (slower growth): 10–20x.

AERA deserves Tier 1 valuation due to its true agentic AI technology (not prompt-based tools), asset-light licensing model, AI training data monetization exposure, global mobile-first reach, and 70% revenue growth profile.

AERA Valuation Scenarios from $1.00

Why AERA Is Extremely Undervalued at $1.00

Current $1.00 market valuation fails to reflect pure-play agentic AI positioning through UFilm.ai + UFlix.ai technology licensing, the AI training data licensing opportunity (voracious emerging demand), the scalable asset-light licensing model (additional licensees coming), global mobile-first reach (virtually unlimited creator supply), the NASDAQ uplist application catalyst not priced in, Tier 1 peer group multiple expansion opportunity, a 70% revenue growth profile commanding premium valuation, and the pre-uplist institutional discovery phase.

Catalysts — Next 12–24 Months from May 2026

Near-Term (Summer/Fall 2026) — Drivers from $1.00

- FY2026 Q3 Results (mid-July 2026) — Validation of 25% sequential growth thesis

- FY2026 Q4 Results (November 2026) — Full-year results and FY2027 guidance

- New Platform Licensee Announcements — Expansion of licensing program

- AI Training Data Licensing Deals — Material contract announcements

- UFilm.ai Creator Milestones — Global creator base milestones

- $4.00 Share Price Breach + $15M Float Value — Triggers NASDAQ uplist application (4x return just to reach this threshold)

Medium-Term (Late 2026 – 2027)

- NASDAQ Uplist Application Filing — Initiates formal review process

- NASDAQ Review Milestones — Progress during 6–9 month review window

- Uplist Completion (mid-to-late 2027) — Institutional unlock upon approval

- Sell-Side Analyst Coverage Initiation — Post-uplist coverage

- Index Inclusion — Russell 2000 mechanical buying

- FY2027 Revenue $70M Milestone — Growth thesis validation

- Additional Licensee Signings — Licensing program expansion

- Major AI Training Data Customer Wins — Enterprise AI companies signing

Long-Term (FY2028+)

- $110M Revenue Achievement — Scale demonstrated

- $20M Operating Income — Profitability inflection

- Strategic Partnership Potential — Major tech/media collaborations

- International Expansion — Geographic diversification

- AI Training Content Category Leadership — Dominant position in fresh content supply

Risk Factors

Investors should consider the following risks:

- Execution Risk — Creator acquisition and licensee signing require sustained execution

- Competitive Entry — Agentic AI and AI training data spaces attracting competition

- Uplist Application Risk — NASDAQ review takes 6–9 months and is subject to regulatory discretion

- Uplist Timing — Both the $4.00 bid price (4x from current $1.00) and $15M market value of public float thresholds depend on share price appreciation; if the share price does not move sufficiently higher, the uplist will be delayed

- Market Value of Public Float — Currently far below the $15M NASDAQ minimum at $1.00 share price; reaching this threshold is dependent on substantial share price appreciation

- Licensing Concentration — Near-term revenue dependent on UFlix.ai license until additional licensees sign

- AI Training Market Evolution — Demand dynamics could shift

- Small-Cap Volatility — OTC-listed stocks at $1.00 price levels exhibit elevated volatility

- Technology Evolution — Rapid AI advancement requires continued R&D

- Regulatory Environment — AI regulation could impact operations

- Capital Requirements — Growth may require additional financing

These risks are reflected in the current $1.00 undervalued positioning.

Price Targets & Rating

Current Rating: STRONG BUY at $1.00 Investment Thesis: Extremely Undervalued Pure-Play Agentic AI Current Price (May 20, 2026): $1.00

Position Sizing Recommendation

At a $1.00 entry price, even modest dollar allocations purchase meaningful share counts. Given the high-conviction nature of this opportunity combined with small-cap volatility:

- Aggressive Investors: 3–5% portfolio allocation

- Moderate Investors: 1–3% portfolio allocation

- Conservative Investors: 0.5–1% portfolio allocation

Scale positions into weakness. Maintain conviction through the 6–9 month uplist review period and beyond.

Conclusion — Why AERA at $1.00 Is a Generational Opportunity

As of May 20, 2026, with AERA trading at just $1.00 per share, AI ERA Corporation represents a rare convergence of factors creating an extremely undervalued pure-play agentic AI investment opportunity:

- Trading at $1.00 — implied $5.5M market cap, a fraction of FY2027 revenue

- Pure-play agentic AI business model — UFilm.ai operations + UFlix.ai technology license + additional licensees coming

- AI training data licensing opportunity — serving voracious, insatiable global AI training demand

- Global mobile-first platform — accessible to anyone with a cell phone, worldwide

- Virtually unlimited fresh content supply — exactly what AI training systems need

- Asset-light scalable licensing model — each new licensee drives high-margin revenue

- Validated H1 FY2026 momentum with 25% sequential Q3/Q4 growth

- $70M FY2027 revenue forecast (+70% YoY)

- $110M FY2028 revenue with $20M operating income

- NASDAQ uplist application upon $4.00 20-day bid price and $15M public float value thresholds (6–9 month completion)

- Tier 1 peer group multiple expansion opportunity

- Institutional discovery phase pre-uplist

The Call

At today's price of $1.00, AERA offers one of the most asymmetric risk/reward profiles in the public markets. A move just to the $4.00 uplist threshold represents a 4x return. A move to conservative 12-month targets represents a 15–25x return. A move to bull case post-uplist targets at Tier 1 peer multiples represents up to a 500x return opportunity over a multi-year horizon.

Investors who position at $1.00 — before the $4.00 threshold and $15M float value are crossed, and certainly before the uplist application is filed — will capture the full multi-stage re-rating: initial price discovery, threshold crossing, application filing, review period anticipation, and post-uplist institutional buying.

Rating: STRONG BUY | Current Price: $1.00 | Time Horizon: 12–36 months | Conviction Level: HIGH

Joseph M. Salvani JD Unfiltered | May 20, 2026

Disclosures

This research report is prepared by Joseph M. Salvani for publication on the JD Unfiltered Substack on May 20, 2026. This report is for informational purposes only and does not constitute investment advice. Readers should conduct their own due diligence and consult with qualified financial advisors before making investment decisions.

Author Disclosure / Conflicts of Interest: The author, Joseph M. Salvani, provides consulting services to a separate company (not AI ERA Corporation) in which the author owns no equity stake and holds no direct or beneficial ownership interest. That separate company, to which the author provides consulting services, has itself received restricted share-based compensation (i.e., that separate company holds restricted shares that were issued to it as compensation). The author personally holds no equity, options, warrants, or other beneficial ownership interests in that separate company, and the author has not received any share-based compensation personally from that separate company. That separate company is a distinct entity from AI ERA Corporation, but the author's consulting relationship with that separate company may involve business or strategic interests that intersect with the agentic AI, creator economy, or AI training content sectors discussed in this report. Readers should consider this relationship in evaluating the objectivity of this report. The author has not received compensation of any kind from AI ERA Corporation for the preparation of this research report. The author and/or JD Unfiltered may hold positions in AI ERA Corporation (AERA) securities.

Pricing Disclosure: Share price references in this report reflect AERA's market price of $1.00 as of the morning of May 20, 2026. Readers should verify current market pricing before transacting. Due to the small-cap, OTC-listed nature of AERA at sub-$2 share price levels, the bid-ask spread may be wide and trading volumes may be limited. Order limits are strongly recommended.

Forward-Looking Statements: Forward-looking statements contained in this report involve significant risks and uncertainties. Actual results may differ materially from projections. Past performance is not indicative of future results. Small-cap and OTC-listed securities carry elevated risk profiles. Price targets of $15 to $500+ per share represent extraordinary multi-year forecasts and there is no assurance that any such targets will be achieved.

NASDAQ Uplist Disclosure: The NASDAQ uplist discussed in this report requires a formal application process. The Company currently meets most NASDAQ Capital Market uplisting criteria, but the $4.00 minimum bid price (currently $1.00, requiring a 4x move) and the $15 million market value of public float criteria are both pending. Both are dependent on share price appreciation. Even when these thresholds are met and the application is filed, the uplisting process is subject to NASDAQ review and approval, which typically takes 6–9 months. There can be no assurance that the thresholds will be met, that the application will be filed, that it will be approved, or that any of these steps will occur on the expected timeline.

All analysis reflects the author's independent assessment based on publicly available information and reasonable assumptions regarding future performance.

Published on JD Unfiltered — May 20, 2026 © 2026 JD Unfiltered | Joseph M. Salvani