The Cannibalization Paradox: Salesforce (CRM) and the Goodyear Radial Precedent

Executive Summary

This thesis examines what may be the most consequential self-cannibalization event in enterprise software history through the lens of the most consequential self-cannibalization event in American industrial history. Salesforce, Inc. (NYSE: CRM), the dominant force in customer relationship management software, has launched Agentforce, an agentic AI platform that threatens to structurally undermine the per-seat licensing model responsible for virtually all of its $41.5 billion revenue base. The closest historical parallel is The Goodyear Tire & Rubber Company (NYSE: GT) during its wrenching transition from bias-ply to steel-belted radial tires in the 1970s.

Both companies sat atop dominant market positions. Both introduced a superior product that would inevitably destroy demand for the legacy cash cow. Both watched their stock prices crater roughly 50% as the market priced in the transition valley. And in both cases, the critical investment question was identical: Is the trough a buying opportunity or a value trap?

The Goodyear precedent initially suggests a 3–5 year compressed transition for Salesforce, with a potential breakout in the 2028–2029 timeframe. However, a critical structural difference undermines the optimistic timeline: Goodyear faced competitors of roughly equal size and financial capacity, while Salesforce faces Microsoft, a company with 16x its operating income and the ability to subsidize AI agent pricing indefinitely. When this competitive asymmetry is factored in, the more likely outcome is a prolonged transition extending into the 2029–2031 window, with Salesforce's reemergence as a growth company taking materially longer than the Goodyear analog alone would suggest.

Part I: Goodyear at Its Pinnacle (1969–1972)

The Dominant Franchise

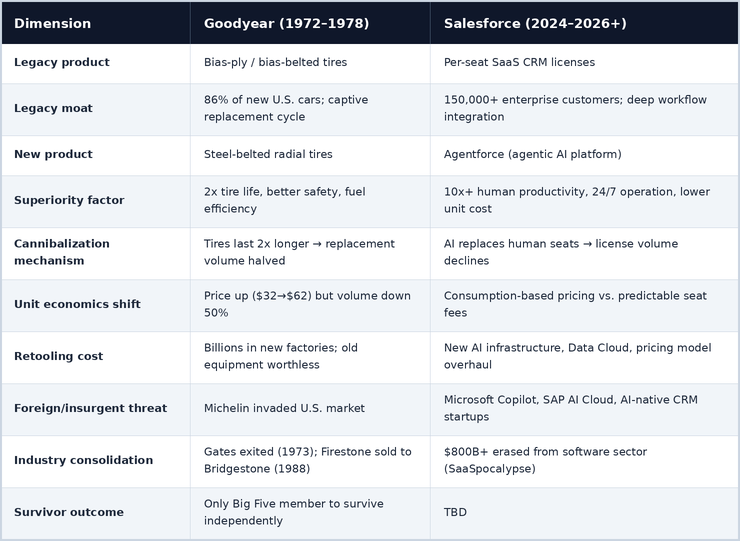

By the late 1960s, Goodyear was the undisputed colossus of the global tire industry. Sales reached $3 billion in 1969 and would hit $5 billion by 1974. The company was the largest tire manufacturer in the world, leading the "Big Five" U.S. producers, Goodyear, Firestone, Uniroyal, Goodrich, and Gates, that collectively controlled the vast majority of both the OEM and replacement tire markets.

Goodyear's dominance rested on a specific technology: bias-ply and bias-belted tires. By 1970, bias-belted designs equipped 86% of new American automobiles. The replacement market was even more lucrative bias-ply tires wore out relatively quickly, generating a steady, predictable replacement cycle that functioned almost like a recurring revenue stream. Goodyear's factories, workforce, supply chains, and capital expenditure plans were entirely optimized around this technology.

The company was not merely a market leader, it was the market. Its brand was synonymous with tires. It supplied all tires for the Indianapolis 500, was consistently ranked among the top companies in the Fortune 500, and carried the strongest balance sheet of the Big Five, with a leverage ratio of just 0.23, the lowest among its major peers.

The Gathering Storm

Michelin had introduced the radial tire in France in 1948, but it remained a European curiosity for decades. By 1972, radials equipped only 8% of U.S. automobiles. Goodyear's management had actively resisted the shift, promoting bias-belted tires as the superior American solution. This was not irrational, Goodyear's entire manufacturing base, representing billions in invested capital, was designed for bias-ply production.

But the physics were inescapable. Radial tires were objectively superior:

- Durability: Radials lasted approximately twice as long as bias-ply tires

- Fuel efficiency: Lower rolling resistance meant better gas mileage — critically important after the 1973 oil embargo

- Safety: Superior road grip, heat tolerance, and handling characteristics

- Higher unit price: Radials commanded $62 versus $32 for bias-ply, providing higher per-unit margins

The problem was existential: a tire that lasts twice as long cuts the replacement market in half. Higher unit prices could not offset the volume destruction. And the manufacturing transition required entirely new factory equipment, bias-ply machinery could not produce radial tires.

Part II: Salesforce at Its Pinnacle (2023–2024)

The Dominant Franchise

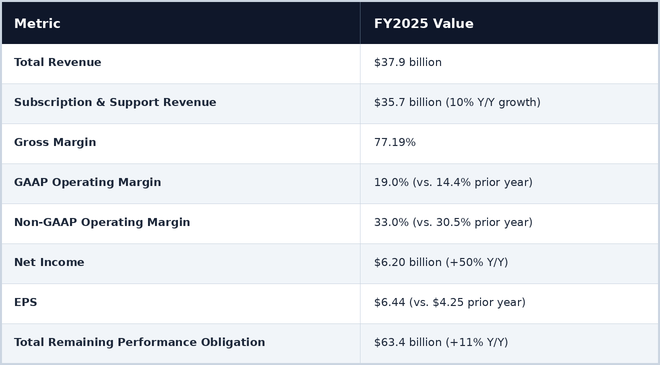

Salesforce entered 2024 as the undisputed leader in enterprise CRM and the broader cloud application ecosystem. Its fiscal year 2025 results reflected a business at peak operational strength:

Salesforce's dominance was built on a specific business model: per-seat SaaS licensing. Every human user of a Salesforce product, Sales Cloud, Service Cloud, Marketing Cloud, etc. required an individual license. Revenue grew as enterprises expanded headcount and as Salesforce cross-sold additional products to each seat. This created a deeply predictable, recurring revenue stream with industry-leading gross margins.

The stock peaked near $369 in February 2024, reflecting a market capitalization exceeding $350 billion. Over 21 consecutive years since going public, Salesforce had never experienced a fundamental threat to its core monetization model.

The Gathering Storm

Just as Michelin's radial had quietly existed in Europe for two decades before reaching critical mass in America, the concept of AI-augmented enterprise workflows had been building for years. But in late 2024, the shift went from incremental to existential with the rise of agentic AI, autonomous software agents capable of performing tasks previously requiring human workers.

Salesforce responded by launching Agentforce, an AI agent platform integrated across its product suite. On the surface, this was a proactive, innovative move, the market leader embracing the next technology wave. But the underlying economics contained the same fatal paradox that haunted Goodyear:

If an AI agent can do the work of a human, the enterprise no longer needs to buy that human a Salesforce seat.

Part III: The Cannibalization Mechanics — A Structural Comparison

The Goodyear-Salesforce parallel is structural. Both companies face the identical economic problem: their new product destroys demand for the old one faster than the new revenue can replace it.

The Pricing Dilemma

Goodyear's pricing challenge was relatively simple: charge more per tire, sell fewer tires. The math never fully worked because volume destruction outpaced price gains.

Salesforce's pricing challenge is far more complex. The company has cycled through three distinct pricing models in roughly 18 months:

- Per-conversation ($2/conversation) — The initial launch model, treating AI agents like chatbots

- Consumption credits (Flex Agreement) — Allowing enterprises to flexibly allocate budgets between seats and AI credits

- Seat-based AELA ($125+/month) — A return to familiar enterprise licensing, bundling "digital workforce" into seat contracts

This rapid cycling reveals deep uncertainty about the right monetization model, precisely mirroring Goodyear's struggle to price radials in a way that didn't destroy its own replacement market economics. As one analyst noted, Salesforce running three models simultaneously "is not confusion, it's a hedge."

Gartner has forecast that agentic AI could drive approximately 30% of enterprise application software revenue by 2035, representing over $450 billion, up from just 2% in 2025. This implies a massive revenue pool, but the transition path from here to there runs directly through the valley of seat-based destruction.

Part IV: The Stock Price Parallel — Anatomy of a Transition Crash

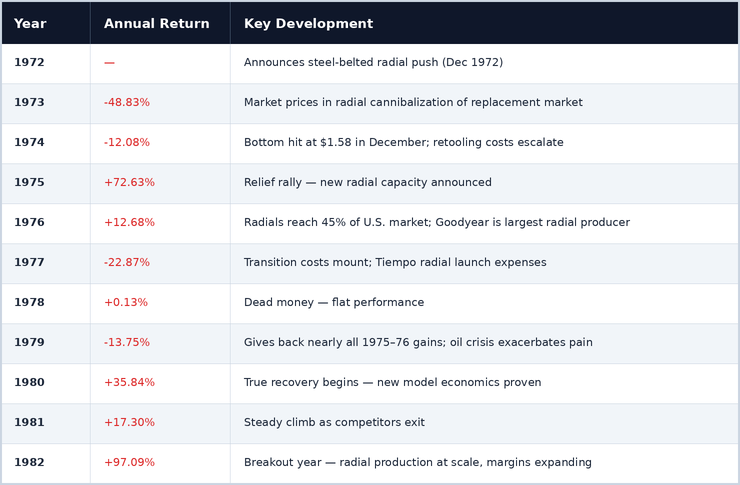

Goodyear's Decline and Recovery (1972–1982)

Goodyear's stock chart during the radial transition is a textbook case of how markets price technological cannibalization:

Peak-to-trough decline: ~51% (early 1973 to December 1974) Time from crash to sustained recovery: ~7 years (1973 to 1980) Time from crash to new highs: ~9 years (1973 to 1982)

The critical lesson: the 1975 bounce of +73% was a relief rally, not a sustainable recovery. Investors who bought the first bottom and held through 1979 endured three more years of drawdowns that erased most of those gains. The true, sustained breakout did not arrive until 1980–1982, after Goodyear's radial factories were operating at scale, competitors had exited or been acquired, the new product's margins were proven at volume, and market consolidation handed Goodyear pricing power.

Salesforce's Decline (2024–Present)

Salesforce's stock price trajectory mirrors Goodyear's almost precisely in both magnitude and pattern:

The symmetry is striking. Both companies experienced nearly identical percentage declines from their peaks, and both declines occurred over roughly the same 18–24 month timeframe following the new product announcement.

Part V: Where Are We in the Cycle?

The Case That Salesforce Is at Goodyear's 1975 (Relief Rally Phase)

Several indicators suggest Salesforce is in the early stages of a relief rally that may not represent the ultimate bottom:

- Agentforce is still sub-scale. At $800 million ARR growing 169% YoY, Agentforce represents less than 2% of Salesforce's $41.5 billion revenue base. In Goodyear terms, the radial factories have been announced but are not yet producing at volume.

- The pricing model remains unresolved. Three concurrent pricing models in 18 months signals deep uncertainty about how to monetize without destroying seat-based revenue.

- Revenue deceleration has not bottomed. Growth has slowed from 20%+ to 10%, and FY27 guidance of $45.8–$46.2 billion implies continued deceleration. The full impact of seat compression has likely not yet manifested.

- The competitive threat is intensifying. Microsoft Copilot, with its own seat-based AI model bundled into M365, represents the Michelin of this cycle — a well-capitalized competitor with an established enterprise footprint and a potentially superior distribution model.

- Goodyear's 1975 rally (+73%) was followed by three years of negative-to-flat returns (1977–1979) before the true breakout. If Salesforce follows the same pattern, a relief bounce from $179 could be followed by 2–3 more years of sideways-to-down performance.

The Case That This Time Is Different (Accelerated Recovery)

Counterarguments suggest the transition could compress versus the Goodyear timeline:

- Software transitions are faster than manufacturing transitions. Goodyear needed to physically build new factories. Salesforce's retooling is software-based, with AI capabilities deployed iteratively through cloud updates.

- Agentforce adoption metrics are accelerating. 29,000+ deals with 50% quarter-over-quarter growth suggests enterprise demand is real and pulling forward.

- The $50 billion buyback provides a floor. Salesforce has committed massive capital return to support the stock through the transition valley. Goodyear had no such tool available in the 1970s.

- FY26 results were strong. Revenue of $41.5 billion represented 10% growth, and Q4 specifically showed 12% growth with $399 million from Agentforce — evidence of re-acceleration.

- The AELA pricing model may solve the cannibalization problem. By wrapping AI agents into higher-priced seat licenses ($125+/month), Salesforce may be able to raise price-per-seat faster than customers reduce seat counts.

Part VI: The Competitive Asymmetry and Where the Goodyear Analogy Breaks Down

Goodyear Fought Equals

During the radial transition, Goodyear competed against companies of roughly comparable size and financial capacity. The Big Five U.S. tire makers operated at similar scale. Even Michelin — the French insurgent that pioneered the radial — was roughly in the same weight class. By 1991, after the transition had fully played out, the top three global producers were Michelin ($10.4B), Bridgestone/Firestone ($9.8B), and Goodyear ($8.5B) — revenue ratios of approximately 1:1 to 1.2:1.

Crucially, Goodyear had the strongest balance sheet of the Big Five. This financial superiority allowed Goodyear to outspend competitors through the transition, invest in new radial factories, and absorb losses that weaker players could not survive. Gates exited tire manufacturing entirely in 1973. Firestone was eventually sold to Bridgestone in 1988. The transition eliminated Goodyear's competitors, handing it consolidated market share and pricing power on the back end.

Salesforce Faces a Colossus

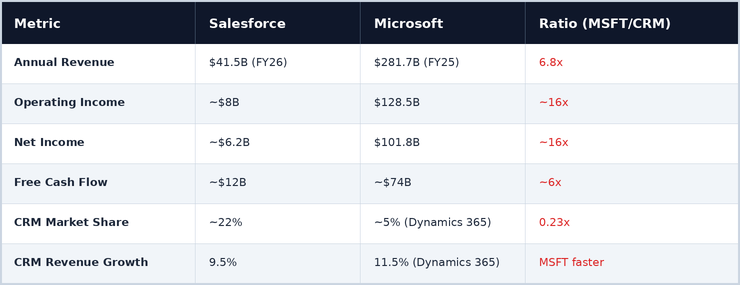

Salesforce enjoys no such competitive advantage. Its primary adversary, Microsoft, operates at an entirely different scale:

Microsoft's quarterly operating income (~$32B) is roughly four times Salesforce's annual operating income. Its total operating income ($128.5B) exceeds Salesforce's entire revenue by more than three times. This is not a fight among peers — it is a category mismatch of historic proportions.

The Bundling Weapon Michelin Never Had

Michelin had one product: tires. When it entered the U.S. market, it competed against Goodyear head-to-head on product quality and price. It could not bundle radial tires with other products enterprises were already purchasing.

Microsoft possesses a weapon Michelin could never have conceived: the horizontal enterprise stack bundle. Copilot and AI agents are being woven directly into Microsoft 365, which already sits on virtually every enterprise desktop globally. Dynamics 365 CRM connects natively to Teams, Outlook, Excel, Power BI, and Azure. An enterprise CTO evaluating agentic AI does not need to buy a standalone product from Salesforce — AI agent capabilities are increasingly included in what the enterprise already pays Microsoft for.

Salesforce's Agentforce, by contrast, is CRM-native and requires enterprises to have their data in the Salesforce ecosystem. It excels at customer engagement workflows but has narrower applicability outside that domain. Microsoft's approach is horizontal across the entire enterprise; Salesforce's is vertical within CRM. In a budget environment where enterprises are consolidating vendors and rationalizing spend, the bundled horizontal platform holds a structural advantage.

The SAP Flanking Attack

The competitive problem compounds further when SAP is added to the picture. SAP's cloud revenue is growing at approximately 27% — roughly triple Salesforce's growth rate — and the company projects €25.8–26.2 billion in cloud revenue for 2026. SAP is the dominant enterprise ERP provider globally, and its AI-powered cloud migration is pulling customers deeper into an SAP-centric stack that competes directly with Salesforce for enterprise budget share.

In Goodyear terms, this is equivalent to Michelin attacking from Europe while Toyota simultaneously entered the tire business with unlimited capital and an existing relationship with every automaker. Goodyear never faced a two-front war against adversaries of this magnitude.

Three Ways the Competitive Asymmetry Extends Salesforce's Transition

1. Goodyear could outspend its peers through the transition. Salesforce cannot outspend Microsoft.

Goodyear's financial superiority over the other Big Five members was the enabling condition of its survival. Salesforce operates in the inverse position, it is the financially weaker party relative to its primary competitor. Microsoft can invest more in AI R&D, offer more aggressive pricing, and sustain losses in CRM indefinitely because CRM is a rounding error within its overall business.

2. Goodyear's competitors died during the transition. Salesforce's competitors will get stronger.

The Goodyear recovery was powered by competitive attrition. In Salesforce's case, Microsoft is not going to exit CRM during the AI transition, it is going to accelerate investment. Every quarter that Salesforce spends navigating the cannibalization valley is a quarter Microsoft uses to close the CRM market share gap with Dynamics 365, which is already growing faster than Salesforce's CRM segment.

3. Goodyear owned its distribution channel. Microsoft's distribution is broader.

Goodyear maintained its own retail stores and deep dealer relationships that gave it a defensible distribution moat. Salesforce has its installed base of 150,000+ enterprise customers, but Microsoft has broader enterprise distribution through M365, reaching departments, teams, and users that Salesforce has never touched. The agentic AI opportunity extends beyond CRM into every enterprise workflow, and Microsoft's horizontal presence means it can capture adjacent use cases that Salesforce's CRM-focused architecture cannot easily reach.

The One Advantage Salesforce Retains: Depth Over Breadth

The sole dimension where the Goodyear analogy still favors Salesforce is domain specialization. Salesforce Agentforce is purpose-built for CRM workflows, sales, service, marketing, with the Data Cloud unifying customer data in real time. Microsoft Copilot is a horizontal tool that does many things adequately but lacks Salesforce's CRM-specific depth.

Goodyear survived the radial revolution not because it was the biggest company, it was not, but because it was the best at making tires. Salesforce's equivalent moat is its 22% CRM market share, deep workflow integration, massive ecosystem of ISV partners, and the switching costs embedded in 150,000 customer deployments.

There are historical precedents for specialists surviving against generalists with vastly larger resources, Bloomberg Terminal has coexisted with Microsoft for decades; Workday competes with Oracle despite being a fraction of its size. But these survivals require the specialist to be dramatically better in its domain, not merely incrementally better. Whether Salesforce's CRM depth constitutes that level of differentiation remains the central open question.

Part VII: The Survivor Question

The most important lesson from the Goodyear case is not about stock prices — it is about survival. Of the Big Five U.S. tire manufacturers entering the 1970s:

Goodyear survived because it made the painful choice to cannibalize itself before competitors did it for them. The companies that hesitated, particularly Firestone, which "wasn't pushed out of tires, it jumped" and lost their independence.

Salesforce faces an analogous competitive landscape, but with a critical difference: the enterprise software peers it must outlast include a company with 16x its operating income. The enterprise software "Big Five" of the current era, Salesforce, Microsoft, SAP, Oracle, ServiceNow, will not all navigate the agentic AI transition successfully. The winners will be those who complete the pricing and product pivot fastest, even at the cost of near-term growth compression.

Marc Benioff has explicitly framed this as a war of attrition, mocking the "SaaSpocalypse" narrative while pointing to Agentforce's growth metrics. Whether this proves to be visionary leadership or overconfidence will determine whether Salesforce becomes the Goodyear (sole survivor) or the Firestone (eventually acquired) of the AI transition.

Part VIII: Revised Investment Implications

Goodyear Timeline Applied to Salesforce and Adjusted for Competitive Asymmetry

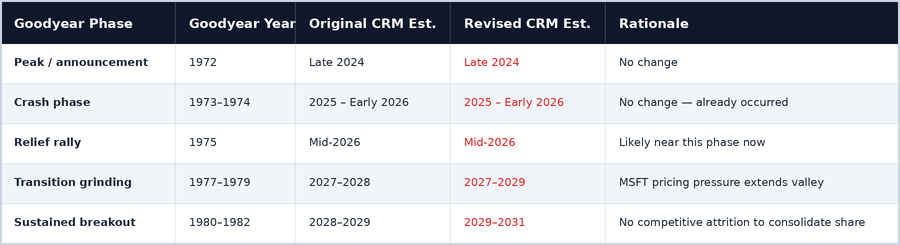

The initial application of the Goodyear precedent suggested a compressed 3–5 year transition, with a Salesforce breakout in the 2028–2029 timeframe. This estimate assumed the competitive dynamics would mirror the tire industry's, a level playing field where the strongest pure-play eventually prevails through attrition.

The Microsoft and SAP competitive asymmetry invalidates this assumption. Rather than compressing versus Goodyear's timeline, the transition is more likely to match or extend Goodyear's full nine-year cycle. Goodyear's competitors exited, handing it market share; Salesforce's competitors will intensify, taking market share. Goodyear could outspend the transition; Salesforce will be outspent during the transition.

The Extended Valley Scenario

In the most likely scenario, Salesforce spends 3–5 years in the transition grinding phase (Goodyear's 1977–1979 equivalent), during which revenue growth remains compressed at 8–12% as seat-based erosion offsets Agentforce ramp, Microsoft Dynamics 365 continues gaining CRM share, Agentforce ARR grows rapidly in percentage terms but remains too small in absolute terms to move the needle, and the stock trades sideways in a wide range, generating negative real returns after inflation.

The breakout, when it arrives, requires one of the following catalysts:

- Agentforce reaches critical mass ($8–10B+ in revenue, representing 15–20% of total), proving the new model can sustain overall growth reacceleration to 15%+

- A major competitor exits or retreats from CRM (the Firestone/Gates scenario) — though Microsoft and SAP are unlikely candidates

- Salesforce's CRM-specific AI proves so dramatically superior that enterprises pay a clear premium over bundled alternatives, establishing category-defining margins

- An acquisition — either by Salesforce (to broaden its moat) or of Salesforce (by a larger enterprise player seeking CRM dominance)

Key Metrics to Monitor

- Agentforce ARR trajectory: Needs to reach $5B+ to credibly offset seat compression; $8–10B+ for sustainable growth reacceleration

- Net revenue retention rate: The single most important metric — will reveal whether AI upsells offset seat reductions within existing accounts

- Pricing model convergence: The current three-model approach must consolidate; watch for which model wins

- Microsoft Dynamics 365 growth rate: If Dynamics decelerates, Salesforce's moat is holding; if it accelerates, the competitive threat is materializing

- Seat count trends: If seat counts decline while revenue grows, the new model is working; if both decline, the thesis is broken

- Enterprise consolidation patterns: Whether customers are consolidating onto Microsoft stacks or maintaining best-of-breed Salesforce deployments

Risk Factors

- Microsoft bundling advantage: Copilot embedded in M365 may prove a more natural distribution path than standalone Agentforce, particularly for mid-market and SMB customers

- SAP flanking risk: SAP's 27% cloud growth rate and AI-powered ERP migrations may capture enterprise budgets that previously went to Salesforce expansion

- Execution risk: Three pricing models suggest internal disagreement; a misstep could accelerate customer churn to competitors who have already consolidated on a single model

- Multiple compression: If growth remains at 10% for 3–5 years, the stock's valuation multiple may compress further, creating extended dead money even without further absolute declines

- The Firestone scenario: Goodyear survived; four peers did not. There is no guarantee Salesforce will be the survivor, particularly against a competitor with 16x its financial resources

- Acquisition risk/opportunity: A prolonged transition period at depressed valuations could attract acquisition interest — this could be a floor on valuation but would represent a failure of the independent growth thesis

Conclusion: A Longer Road Than the Headline Suggests

The Goodyear radial tire transition remains the most instructive precedent for understanding Salesforce's self-cannibalization mechanics. The structural parallel, dominant company introduces superior product that destroys demand for legacy cash cow, maps with remarkable precision. The ~51% peak-to-trough stock declines are nearly identical. The market psychology, fear of the transition valley, uncertainty about the new model's economics, oscillation between hope and despair, is the same.

But the analogy flatters Salesforce in one critical respect: it assumes a competitive environment that does not exist.

Goodyear survived and ultimately thrived because it was the strongest player in a field of equals. It could outspend the transition, and its competitors obligingly died or were acquired, handing Goodyear the consolidated market share and pricing power that fueled the 1980–1982 breakout. Salesforce faces the inverse dynamic. Its primary competitor, Microsoft, has 16x its operating income, broader enterprise distribution, a native AI infrastructure advantage through Azure and OpenAI, and the ability to bundle CRM AI agents into an existing platform that touches virtually every enterprise worker.

The trough is real. The parallel is instructive. But the road back is longer than the Goodyear headline suggests.

The views expressed in this thesis represent independent investment research and analysis. This is not investment advice. Investors should conduct their own due diligence and consider all material risks before making investment decisions.