Eli Lilly's Centessa Purchase at Nearly $8 Billion Makes VVOS the Most Undervalued Nasdaq Company

Executive Summary

On March 31, 2026, Eli Lilly announced a definitive agreement to acquire Centessa Pharmaceuticals (NASDAQ: CNTA) for up to $7.8 billion ($6.3B upfront + $1.5B in CVRs), representing a 70% premium to the prior close. The acquisition targets Centessa's orexin receptor 2 (OX2R) agonist pipeline for sleep-wake disorders — experimental drugs that won't reach patients for 4–6 years, have no FDA clearance, treat zero patients today, and generate zero revenue.

Meanwhile, Vivos Therapeutics (NASDAQ: VVOS), trading at a market capitalization of approximately $11 million, already operates the largest sleep center network in Nevada, holds multiple FDA 510(k) clearances for oral devices treating mild-to-severe obstructive sleep apnea in adults and children, has treated over 60,000 patients worldwide, just achieved in-network status with commercial insurers and Medicare, receives 3,000 new patients per month, and has demand exceeding capacity by more than 2x.

Lilly paid approximately 709 times VVOS's entire market capitalization for a company that treats the downstream symptom of a disease cascade that VVOS addresses at its structural origin. This report examines why the Centessa acquisition exposes VVOS as potentially the most undervalued company on the Nasdaq.

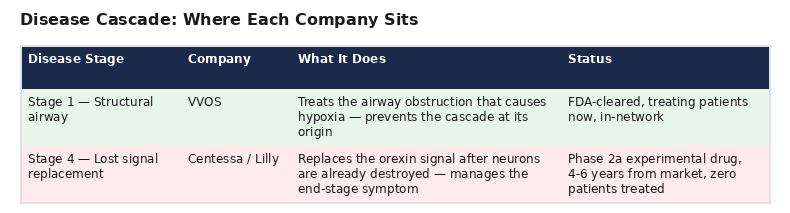

The Disease Cascade: Where Each Company Sits

The published medical literature establishes a clear causal chain in sleep-disordered breathing:

- Airway obstruction → causes repeated breathing stoppages during sleep

- Chronic intermittent hypoxia → repeated oxygen deprivation generates massive free radical (ROS) production in the brain

- Oxidative destruction of wake-promoting neurons → ferroptosis and apoptosis destroy the orexin neurons in the lateral hypothalamus that maintain wakefulness

- Permanent wakefulness impairment → narcolepsy, excessive daytime sleepiness, cognitive decline

Each company addresses a different stage:

Lilly paid $7.8 billion for the end of the cascade. VVOS trades at $11 million and treats the beginning.

VVOS: What They've Built

Sleep Center Network — Nevada

Vivos completed the acquisition of The Sleep Center of Nevada (SCN), the largest sleep center operator in the state, in June 2025 for $7.5 million ($6M cash + $1.5M stock). SCN operates multiple locations across the Las Vegas metropolitan area:

- Charleston (Central Las Vegas)

- Henderson/Southeast

- North Las Vegas

- Summerlin

- Pahrump

- Additional locations across the greater Las Vegas area with seventeen total beds

SCN handles approximately 3,000 new patients monthly for sleep testing, consultations, and treatments. After integration with Vivos, Q3 2025 generated $2.2 million in sleep testing revenue plus $300K in treatment center revenue from SCN operations alone.

Insurance and Medicare Milestone

On March 26, 2026, Vivos announced that its Nevada-supported practices achieved in-network status with multiple commercial insurers and participating status with Medicare, a critical inflection point that:

- Removes the primary barrier to patient conversion (out-of-pocket cost)

- Opens the Medicare population (the largest sleep apnea demographic)

- Positions every SCN location for accelerated patient volume growth

- Was accompanied by approximately $4 million in annualized expense reductions

National Expansion

Beyond Nevada, Vivos opened an affiliated sleep center near Detroit (Auburn Hills, Michigan) in December 2025 through a capital-efficient affiliation model with MISleep Solutions. The company has stated it is actively pursuing additional partnerships and acquisitions nationwide, using a model that minimizes capital outlay while expanding its geographic footprint.

FDA-Cleared Treatment Products

Vivos holds what Centessa won't have for years — FDA 510(k)-cleared medical devices already in clinical use:

- DNA (Daytime-Nighttime Appliance): Cleared for mild-to-severe OSA in adults and moderate-to-severe OSA in children, the first oral appliance ever cleared by FDA to treat severe OSA

- mRNA and mmRNA appliances: Additional cleared configurations for varying clinical presentations

- 80% of severe OSA patients showed improvement in the FDA submission data

- Landmark pediatric clinical trial results published September 2025, with FDA clearance for pediatric OSA achieved in 2024, the first oral device ever cleared for pediatric moderate-to-severe OSA

- Named one of Fast Company's World's Most Innovative Companies

- Over 60,000 patients treated worldwide to date

Demand Exceeds Supply

Vivos has disclosed that it is currently serving less than 40% of existing patient demand at its Nevada sleep centers, meaning more than 60% of patients seeking care cannot be accommodated with current capacity. This is the inverse of Centessa's situation, where there are zero patients and zero demand because the product doesn't exist yet.

Centessa: What Lilly Bought for $7.8 Billion

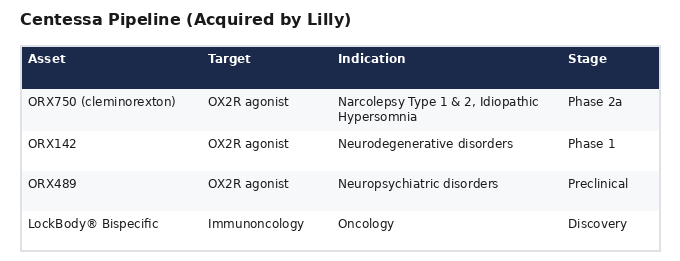

Pipeline

What Centessa Does Not Have

- No FDA-approved or cleared products

- No patients being treated

- No revenue

- No physical clinical infrastructure

- No insurance network relationships

- No companion diagnostic or patient stratification

- No mechanism to address the hypoxia that causes the neuron destruction its drugs attempt to compensate for

- CVR milestone deadlines expiring January 1, 2030 — suggesting even Lilly isn't fully confident in the regulatory timeline

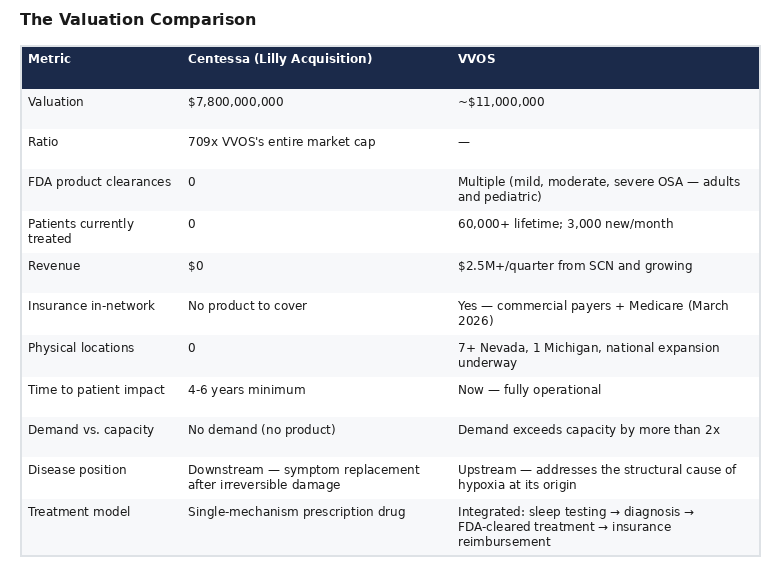

The Valuation Comparison

Why VVOS Treats the Actual Disease

Centessa's OX2R agonists address wakefulness impairment — the consequence of orexin neuron destruction. But published research establishes that chronic intermittent hypoxia from obstructive sleep apnea is what generates the oxidative stress, ferroptosis, and neuronal apoptosis that destroy those orexin neurons in the first place. The wakefulness deficit is not the disease — it is the downstream result of the structural airway problem.

VVOS's FDA-cleared DNA appliance treats the airway obstruction itself — the structural origin of the entire cascade. By restoring proper airway patency:

- Apnea events are reduced or eliminated

- Chronic intermittent hypoxia is reduced at its source

- The oxidative stress cascade that destroys orexin neurons is attenuated

- The need for an orexin-replacement drug like Centessa's may be reduced or eliminated entirely

Lilly's $7.8 billion buys a bandage for the wound. VVOS's $11 million market cap reflects a company that prevents the wound from occurring.

The Tirzepatide Redundancy Problem

Lilly's own tirzepatide (Mounjaro/Zepbound, $36.5B 2025 revenue) has been shown in preclinical studies to activate the SIRT3/NRF2 pathway, upregulating SOD2, GPX, GR, CAT, and NRF2 itself. Zepbound was recently approved for obstructive sleep apnea. If Lilly already owns a product that addresses sleep apnea and activates the same antioxidant defense pathways that Centessa's drugs indirectly engage, the incremental $7.8 billion for Centessa's narrower, later-stage, downstream mechanism becomes even harder to justify, particularly when a company like VVOS is treating the same patient population today, with FDA-cleared products, at a valuation that represents 0.14% of the Centessa deal.

The Lilly Acquisition Context

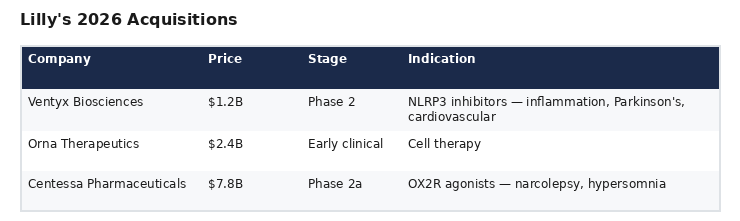

Centessa is Lilly's third acquisition in 2026:

Lilly paid 6.5x more for Centessa than for Ventyx, despite Ventyx addressing a substantially larger total market (NLRP3 inflammasome: >$5B → $100B+ in broader inflammation) with assets at a comparable clinical stage. Ventyx was acquired at distressed pricing (90% stock decline from IPO), while Centessa commanded a premium driven by competitive bidding. On a risk-adjusted, market-size-normalized basis, the Centessa premium appears elevated relative to both Ventyx and especially relative to VVOS.

VVOS Growth Catalysts

Several near-term catalysts could accelerate a revaluation:

- Insurance in-network status just achieved (March 2026) — patient conversion and revenue per patient should increase materially as out-of-pocket barriers are removed and Medicare patients gain access

- Demand exceeding capacity by >2x — any capacity expansion directly converts to revenue

- National expansion model proven — the Detroit/Auburn Hills affiliation model demonstrates capital-efficient replication of the Nevada blueprint

- Pediatric OSA market entry — first-ever FDA-cleared oral device for pediatric moderate-to-severe OSA opens an entirely new patient population

- Annualized $4M expense reduction already implemented — improving path to profitability

- Clinical trial data publication (June 2025, September 2025) — continued peer-reviewed validation strengthens payer and physician adoption

- Fast Company World's Most Innovative Companies recognition — brand awareness catalyst

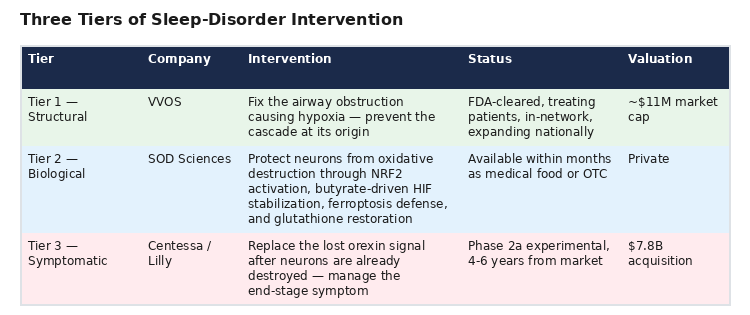

Three Tiers of Sleep-Disorder Intervention

A healthcare portfolio manager evaluating the sleep space should recognize three complementary tiers:

The market currently prices the Tier 3 downstream symptom-management play at 709x the Tier 1 upstream structural-correction play. VVOS has FDA clearances, 60,000+ patients treated, 3,000 new patients monthly, demand exceeding capacity, in-network insurance status, national expansion underway, and growing quarterly revenue, all in the exact disease space that Lilly just valued at nearly $8 billion.

Investment Thesis

Eli Lilly's $7.8 billion acquisition of Centessa Pharmaceuticals establishes a clear market signal: the sleep-disorder therapeutic space commands premium valuations. Yet Centessa has no approved products, no patients, no revenue, no infrastructure, and operates at the very end of the disease cascade, replacing a lost neurological signal after irreversible brain cell destruction has already occurred.

Vivos Therapeutics operates at the beginning of the same cascade, treating the structural airway obstruction that causes the chronic intermittent hypoxia that generates the oxidative stress that destroys the orexin neurons that Centessa's drugs attempt to pharmacologically replace. VVOS has FDA-cleared products, demonstrated clinical outcomes, physical sleep center infrastructure, newly achieved insurance network status, a national expansion model, demand that exceeds its current capacity by more than double, and growing revenue.

At approximately $11 million in market capitalization, 0.14% of the Centessa acquisition price, Vivos Therapeutics appears to be the most undervalued company on the Nasdaq relative to the market's own demonstrated willingness to pay for exposure to the sleep-disorder space.

The market just told you sleep is worth $7.8 billion. It hasn't noticed that the company treating the cause, not the symptom, trades for $11 million.

This analysis is based on publicly available clinical data, published preclinical research, SEC filings, corporate press releases, regulatory frameworks, and deal terms as of April 1, 2026. It does not constitute investment advice. The author may hold positions in securities discussed in this report and reserves the right to buy or sell shares at any time without notice. Forward-looking statements regarding timelines, market sizes, valuations, and biological mechanisms involve inherent uncertainty. Investors should conduct their own due diligence.