AmpliTech Group, Inc. (NASDAQ: AMPG): The Sole-Source AI-RAN Asset

Horizon: 24 Months (through May 2028) | Rating: Strategic Buy / Acquisition Candidate

Current Price: $5.23 | 24-Month Blended Target: $28.40 | Upside: +443%

Strategic Takeout Range: $13.00 – $32.00 | Standalone Discounted Range: $41 – $70

1. Executive Summary

AmpliTech Group is the only US supplier of a commercial-grade 64T64R O-RAN Massive MIMO radio validated in independent multi-lab interoperability testing — and, uniquely, the only AI-RAN platform certified by NVIDIA for integration into the Aerial/ARC reference architecture for 6G. Across a 24-month horizon, three reinforcing super-cycles converge on a single physical-layer dependency that AmpliTech alone resolves domestically: direct-to-cell satellite, AI-native 6G, and autonomous mobility/robotics.

Current market capitalization of approximately $110M is, in our view, mispriced by a factor of three to five against fundamental and strategic value.

We assign a probability-weighted 24-month price target of $28.40 per share (+443%) and identify a strategic takeout floor in the $13.00–$15.00 range, with contested-bid scenarios pricing the equity above $32.

2. The Thesis in One Paragraph

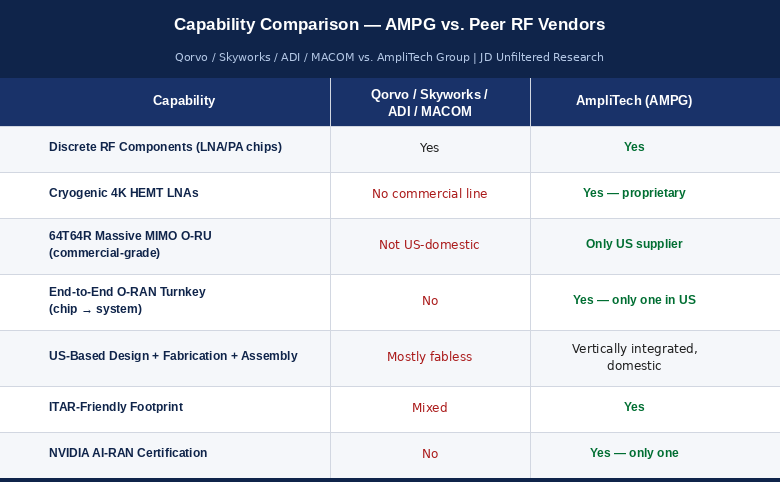

The infrastructure build-out for satellite-direct-to-cell, AI-native 6G, autonomous mobility, and agentic edge inference shares a single physical-layer dependency: the noise figure and linearity of the receive chain. AmpliTech is the only domestic vendor that delivers that capability across all four end markets in vertically integrated form — chip → MMIC → radio unit → managed network service. Its NVIDIA AI-RAN certification, sole-source 64T64R O-RAN status, and proprietary cryogenic HEMT LNA portfolio together constitute a moat that cannot be replicated organically inside three to five years and greater than $500M of capex.

3. Channel Summary — How AMPG Became Strategic

Across the analyses we have published, a consistent picture has emerged:

Q1 2026 financial inflection. Revenue +48.6% year-over-year to $5.35M; gross margin 48.0%, +1,500 basis points; cash and securities $18.4M post-recapitalization.

Backlog convertibility. $40M LOI with second-half 2026-weighted shipments; greater than $20M backlog disclosed.

Sole US 64T64R O-RAN supplier. Multi-lab interoperability validated in O-RAN Global PlugFest Fall 2025 — first and only commercial-grade US entry.

NVIDIA AI-RAN Certification. AmpliTech's True G Speed Services platform is the only US-origin radio stack formally certified by NVIDIA for the AI-RAN reference architecture, integrating GPU-accelerated DU/CU functions with AmpliTech's 64T64R radio front end.

Cryogenic Quantum LNAs. Proprietary 4K HEMT amplifiers commercialized for qubit readout — one of a tiny domestic supplier set.

Direct-to-cell relevance. Receive-chain noise figure is the binding constraint on Starlink, Kuiper, and AST link budgets; AMPG sits at that bottleneck.

Autonomous and robotics tailwinds. Automotive AI growing from $4.81B (2025) to $33.3B (2034); each node a 24–80+ GHz RF socket.

Hyperscaler demand vector. SpaceX targeting summer 2026 IPO at greater than $1.75T; NVIDIA pushing AI-RAN as a 6G platform; Amazon Kuiper commercial launch underway.

4. Why 24 Months Re-Rates the Multiple

A 12-month framework prices the LOI conversion and one design-win cycle. A 24-month framework prices three independent step-functions:

SpaceX IPO and post-IPO capex unlock (2H 2026 → 2027). Pre-IPO disclosures already indicate vertical-integration intent extending to GPUs; cryogenic LNAs and 64T64R gateway radios are the natural next layer.

NVIDIA AI-RAN production deployments (2026–2028). The Aerial/ARC reference architecture moves from pilots to commercial deployment with US carriers, foreclosing non-certified radio vendors.

Kuiper commercial service (2026–2027). Each constellation bird is an LNA/PA bill of materials and AmpliTech is positioned in the domestic supplier set.

DoD/CHIPS reshoring procurement (2026–2028). 64T64R domestic supply is now a stated national-security priority.

6G standardization milestones (3GPP Release 20/21, 2027). Sub-THz amplifier requirements eliminate most legacy chip vendors.

Autonomous mobility and robotics scaling (2025–2034 at 24% CAGR). RF socket count per vehicle and per humanoid robot expands measurably inside the 24-month window.

Across that horizon, FY27 revenue plausibly reaches $60–95M and FY28 $110–160M as the O-RAN ramp compounds against AI-RAN design wins.

5. The NVIDIA AI-RAN Certification — The Decisive Catalyst

NVIDIA has framed AI-RAN as the architectural inflection that restores US leadership in 6G, with the NVIDIA Aerial and ARC platforms providing the GPU-accelerated baseband layer. That platform is, however, useless without a low-noise, high-linearity radio front end that is interoperable, software-definable, and ideally domestically sourced. AmpliTech is, to our knowledge, the only US-origin radio platform that has cleared NVIDIA's technical certification for that integration — a position that rests on three pillars:

Vertical integration. Chip-level innovation through AMPG's MMIC Design Center down to assembled radio units, controlled in one entity.

O-RAN compliance. Validated 64T64R interoperability across multiple independent labs, eliminating integration risk for hyperscaler procurement.

Domestic, ITAR-friendly supply chain. Aligned with CHIPS Act and DoD reshoring imperatives.

The strategic implication is direct: any hyperscaler or telco deploying NVIDIA AI-RAN in the United States must, by elimination, transact with AmpliTech for the radio layer. This structural dependency does not exist with Qorvo, MACOM, Skyworks, or Analog Devices — none of which deliver a certified AI-RAN-ready 64T64R O-RU.

6. Sole US Supplier Documentation

Three independently sourced statements establish this as a verified competitive position:

First, AmpliTech is the first and only US company to bring a 64T64R commercial-grade Massive MIMO radio into formal O-RAN lab testing. Second, AMPG is the only US-based, vertically integrated company offering complete end-to-end turnkey solutions for both private and commercial O-RAN deployments — design, chip-level innovation, packaging, assembly, and network-level integration in one entity. Third, independent buy-side research (Guardian Research, January 2026) concurs: AmpliTech is "the supplier of choice" by virtue of the combination of domestic manufacturing, O-RAN certification, and proven interoperability.

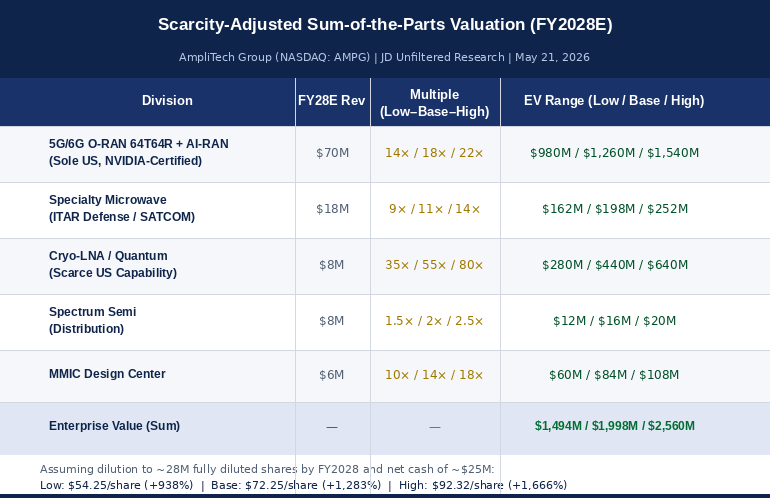

7. Scarcity-Adjusted Sum-of-the-Parts (FY2028E)

Multiples are elevated to reflect the AI-RAN sole-source dynamic, confirmed sole-supplier status in 64T64R, and full conversion of the cryo-LNA quantum business into recurring design-win revenue over 24 months.

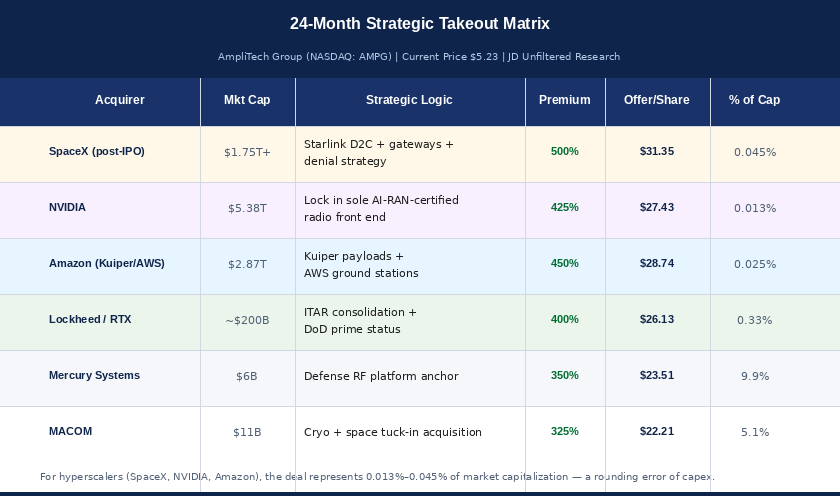

8. 24-Month Strategic Takeout Matrix

Over 24 months, the strategic logic for hyperscalers shifts from "could acquire" to "must acquire to deny competitors." Premiums rise accordingly. For all three hyperscalers — SpaceX, NVIDIA, Amazon — the deal is a rounding error of capital expenditure, representing between 0.013% and 0.045% of market capitalization.

9. Probability-Weighted 24-Month Target: $28.40 (+443%)

This is a meaningful upgrade from the 12-month $15.18 target, driven by three compounding factors: the O-RAN/AI-RAN revenue ramp, cryo-LNA scarcity multiples normalizing higher as quantum compute scales, and the increasing probability of a strategic buyout once the SpaceX IPO and Kuiper commercial launch crystallize.

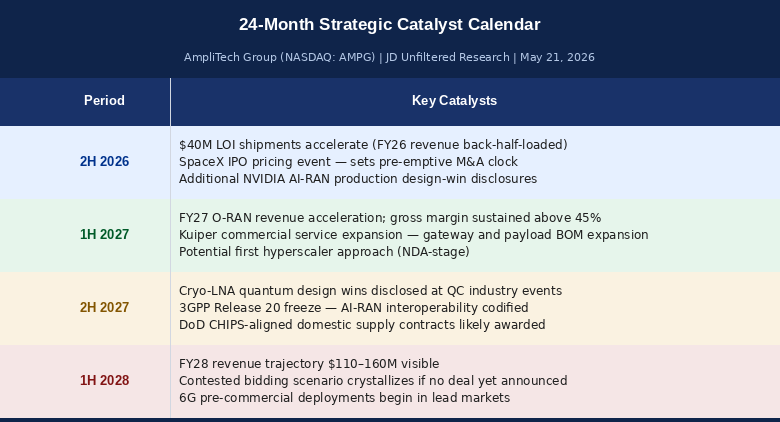

10. 24-Month Catalyst Calendar

11. Corp-Dev Acquisition Memo (Hyperscaler Audience)

Recommendation. Initiate a confidential approach to AmpliTech Group's board with an all-cash offer in the $13.00–$15.00 per share range (approximately $330M–$380M), structured for closure inside 90 days. The strategic window is closing as the SpaceX IPO and 6G AI-RAN procurement cycles converge in 2H 2026.

Strategic Rationale.

Sole US Supplier of Commercial-Grade 64T64R O-RAN Massive MIMO. Vertically Integrated, ITAR-Compliant. Scarce Cryogenic LNA Capability. Triple Convergence — D2C satellite, AI-RAN 6G, autonomous mobility.

Cost vs. Strategic Cap. At $300–400M, the deal represents 0.013%–0.045% of any hyperscaler's market cap — less than one quarter of typical RF/SATCOM capex — and locks up the only domestic supply chain element capable of supporting D2D and AI-RAN roadmaps without third-party dependency.

Risk to Not Acting. A competing hyperscaler executes first, foreclosing domestic RF supply for D2C/6G. Foreign acquisition triggers CFIUS review but distorts pricing if a US strategic must counter-bid. Organic build-out of equivalent capability requires 3–5 years and greater than $500M of patient capex — far above the takeout cost at current prices.

12. Risk Factors

ICFR material weaknesses disclosed Q1 2026; remediation in process and standard for sub-$100M market cap companies.

Customer concentration. The $40M LOI represents the dominant near-term revenue driver; concentration risk is real until additional design wins materialize.

Dilution path. Recent rights offering and registered direct placement netted approximately $16.4M; further raises are possible if capex accelerates.

Hyperscaler self-supply. SpaceX has signaled vertical-integration intent; however, the organic timeline of 3–5 years argues strongly against build-vs-buy at the $300–400M takeout price.

Micro-cap liquidity volatility. A float of 21.7M shares amplifies news-driven price moves in both directions.

13. Conclusion

Over 24 months, AmpliTech Group is positioned to convert from a misunderstood micro-cap into a publicly recognized sole-source US strategic asset sitting at the only chokepoint that simultaneously matters to SpaceX, NVIDIA, Amazon, Lockheed/RTX, and the DoD. The probability-weighted blended target of $28.40 (+443%) reflects a realistic distribution of standalone and strategic outcomes; the upside skew is substantial because the standalone fair value (discounted to today) overlaps the contested-bid scenario, meaning multiple paths converge on the same destination.

We reiterate Strategic Buy / Acquisition Candidate with a 24-month price target of $28.40, contested-bid ceiling of $32+, and standalone discounted ceiling of $70+ in the high-multiple scenario.

14. Disclosures

This research is for informational purposes only and does not constitute investment advice. The authors may hold positions in securities discussed. Forward-looking statements are estimates based on publicly available information as of May 21, 2026 and are subject to material change. Past performance is not indicative of future results.

"I own shares of the Company and may buy or sell shares at any time without prior notice. This statement is not a recommendation to buy or sell securities and reflects my personal investment decision."

Walsh & Salvani | Strategic Equity Research | JD Unfiltered | May 21, 2026