The Hidden Marketplace Accelerant: How the Tokenization of a Future Sales Discount Could Reshape Every Public Company Balance Sheet in America And Send the S&P 500 and Dow Jones to Unimaginable Heights

A convergence of FASB accounting reform, SEC-CFTC regulatory clarity, maturing blockchain infrastructure, and one patent-pending invention from a micro-cap OTC company may be about to unlock the largest balance sheet transformation in the history of public markets, with the S&P 500 and Dow Jones Industrial Average as perhaps the biggest beneficiaries of all.

For decades, a corporate discount on a future sale, "buy our product, get 10% off," was a cost center. A marketing expense. A line item that reduced revenue and disappeared into the ether. It appeared nowhere on a balance sheet. It created no asset. It built no equity.

BCII Enterprises Inc. (OTCID: BCII), led by CEO Joseph M. Salvani and Co-Founder Daniel Walsh, recognized something hiding in plain sight: a future sales discount is economically identical to a prepaid asset, a contractual right with measurable value that simply lacked the technology to be packaged, priced, and traded. Until now.

BCII's patent-pending Coupon Token architecture takes that hidden prepaid asset, wraps it in a blockchain-based token with a capped value tied to a specific product discount, deploys it on Coinbase's Base Layer-2 Ethereum infrastructure via technology partner Horizon Globex GmbH, and makes it tradeable, stakeable, and critically, recognizable as a current asset at fair market value on a public company's balance sheet.

The implications extend far beyond individual companies. Consider: the S&P 500 is a market-capitalization-weighted index of the 500 largest U.S. public companies. The Dow Jones Industrial Average tracks 30 blue-chip giants. If even a fraction of these constituents adopt the Coupon Token architecture and report hundreds-of-percent increases in total shareholder equity and total assets, the indices themselves don't just rise, they are structurally re-rated upward in a way that no earnings cycle, no Fed rate cut, and no fiscal stimulus has ever achieved. Every index fund, every ETF, every pension fund benchmarked to the S&P 500 or Dow rides that wave automatically. This is not a stock picker's market, it is a tide that lifts every indexed boat in America.

The result is not theoretical. The accounting opinion has been rendered. The regulatory framework has been clarified. The technology partner is signed. The patent is filed. The only thing missing is the first major corporation to pull the trigger and when it does, every other public company will have no choice but to follow.

The Four Pillars That Made This Moment Possible

This could not have happened five years ago, or even two years ago. Four separate developments had to converge simultaneously.

Pillar 1: FASB ASU 2023-08 The Accounting Revolution

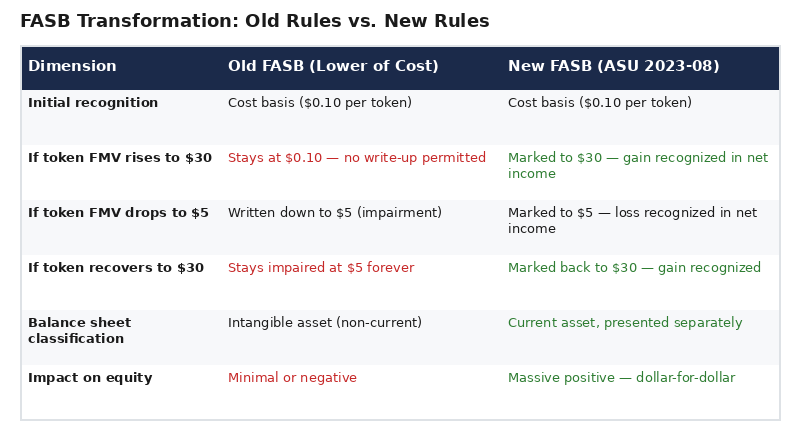

Before January 2025, public companies holding crypto tokens were trapped under "lower of cost or market" accounting, tokens could be written down on impairment but never written up, even if their market value soared. This made holding any token economically irrational for a CFO. The new FASB guidance flipped the paradigm entirely: qualifying crypto assets are now measured at fair market value, with changes recognized in net income and classified as current assets on the balance sheet. CFO Squad Inc., specialists in SEC financial reporting, confirmed in February 2026 that BCII's Coupon Token qualifies under this framework.

What this means in practice: a corporation acquires the Coupon Token platform from BCII for approximately $6 million (60 million tokens at a de minimis $0.10 each, amortized over 5 years at $1.2M/year). It then holds hundreds of millions of tokens that the secondary market prices at, say, $30 each. Under the old rules, those tokens sit on the books at $0.10 forever. Under the new rules, they are marked to $30 — and the $29.90 per token spread flows directly through net income into retained earnings, massively expanding total shareholder equity.

Pillar 2: The SEC-CFTC Regulatory Clarity of March 2026

On March 17, 2026, just days ago, the SEC and CFTC issued their historic joint interpretation providing the first coherent token taxonomy in U.S. history. SEC Chairman Paul Atkins stated: "Most crypto assets are not themselves securities." The framework classifies digital commodities, digital collectibles, digital tools, stablecoins, and digital securities into distinct categories, with primary CFTC jurisdiction over commodity tokens. This followed the March 10 SEC-CFTC Memorandum of Understanding committing both agencies to harmonized regulation.

For BCII's Coupon Token, a consumptive-use, capped-value discount instrument, this regulatory clarity is the final barrier removed. The tokens are not securities under the Howey Test (confirmed by precedent from TurnKey Jet and Pocketful of Quarters no-action letters), and they now fall under a clear, workable regulatory framework that institutional legal departments can approve.

Pillar 3: Maturing Token Markets and Infrastructure

The infrastructure to issue, trade, and settle tokens at enterprise scale now exists. BCII's system runs on Coinbase's Base Layer-2 blockchain, an EVM-compatible scaling solution with low transaction costs and Ethereum-grade security. The architecture includes a smartphone app for shareholders to claim tokens via their transfer agent, a dollar-backed in-app stablecoin for instant settlement, and peer-to-peer secondary market trading. This is not a whitepaper. It is deployed infrastructure with a signed licensing agreement.

Pillar 4: The Desire for Real Value in Crypto Markets

The crypto market has spent years oscillating between speculation and collapse, driven by tokens with no intrinsic value. BCII's Coupon Token offers something the market has never had: a token with a mathematically verifiable floor value tied to a real product discount. A $50 coupon token on a $500 product can never exceed $50, and it has immediate consumptive use, it can be redeemed for a real discount on a real product from a real public company. For the millions of retail traders who want crypto exposure but are tired of losing money on vaporware, this is a fundamentally different asset class.

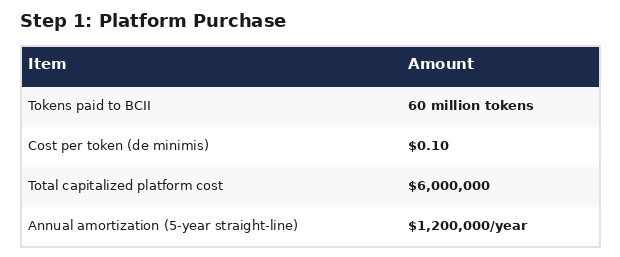

How a Corporation Acquires the Platform

The process is straightforward. A publicly traded company purchases BCII's customized, white-label Coupon Token platform. BCII's compensation is paid in tokens, not cash:

- The corporation pays BCII 60 million Coupon Tokens as the license fee

- Each token is acquired at a de minimis cost of $0.10 per token

- Total capitalized platform cost: 60,000,000 × $0.10 = $6,000,000

- This $6M is recorded as an intangible asset (platform license) and amortized straight-line over 5 years = $1,200,000/year amortization expense

- Both the corporation and BCII are limited by smart contract to a defined maximum number of tokens they can sell per trading day, preventing either party from flooding the market

This purchase, not self-minting, is what qualifies the entire token ecosystem to sit under the FASB ASU 2023-08 fair value framework. The tokens have an actual acquisition cost, a legitimate counterparty transaction, and are carried as current assets at fair market value going forward.

The 300 Million Token Allocation: The 50% Shareholder Supercharger

BCII's architecture allocates 300 million tokens per corporate client. The allocation structure is as follows:

- 50% (150 million tokens) — distributed directly to shareholders as rewards across 5 equal installments (30 million per distribution) over 55 months

- 20% (60 million tokens) — paid to BCII Enterprises as its platform/license fee

- 30% (90 million tokens) — retained by the issuing corporation for reserve pool, trading liquidity, staking pools, and operational needs

Each token is tradeable for 10 months, followed by a 1-month redemption window. If unredeemed, tokens expire and revert to the corporate reserve pool for recycling.

This 50% shareholder allocation does something no traditional dividend can do: it simultaneously rewards holding, incentivizes product purchases, creates a tradeable secondary market, and forces shareholders to verify ownership through the transfer agent five separate times, exposing phantom shares and making naked shorting structurally impossible.

The Brand Identification Winners: Why Nike, Apple, and Coca-Cola Tokens Are Worth More Than Anyone Else's

Not all Coupon Tokens are created equal. The architecture is universal, but the secondary-market value of each company's token is a direct function of the desirability of the brand behind it.

Consider three tokens, each offering a 10% discount:

- A Nike Coupon Token — 10% off any Nike product — carries the aspirational weight of one of the most recognized brands on Earth. Sneaker culture, athlete endorsements, global cachet. Secondary market demand would be enormous. The token trades near face value.

- An Apple Coupon Token — 10% off any Apple product — represents a discount on devices that consumers already line up overnight to purchase at full price. Apple has never offered meaningful discounts in its history. The scarcity premium on an Apple discount token would be extraordinary.

- A Coca-Cola Coupon Token — 10% off Coca-Cola products — taps into the single most recognized consumer brand in human history, distributed in over 200 countries.

Now contrast that with a coupon token from a generic regional retailer with no brand loyalty. Same mechanics, same architecture, but the token trades at 20% of face value instead of 90%.

This is why companies with exceedingly valuable brand identification are the other massive winners of the Coupon Token revolution. Their tokens will command the highest secondary-market premiums, which means the largest fair market value on their balance sheets, the biggest equity increases, and the most powerful shareholder engagement. A Nike or Apple Coupon Token isn't just a discount, it's a status symbol on the blockchain, a tradeable piece of brand equity that consumers and speculators will compete to own.

The brand hierarchy that already exists in the consumer economy will be replicated, and amplified, in the token economy. The strongest brands win twice: once in the product market, and again on the balance sheet.

Why This Is Not a Security: The Three-Pillar Howey Test Defense

BCII's regulatory framework rests on a three-pillar compliance structure directly reinforced by existing SEC no-action letters:

Pillar 1 — Consumptive Use: The SEC's Framework for Investment Contract Analysis states that "economic benefit that comes solely from the use of the application is not considered 'profits' under Howey." Coupon Tokens provide immediate product discounts with time-limited redemption, they are digital coupons, not investment instruments.

Pillar 2 — Capped Appreciation: The SEC guidance says "prospects for appreciation in the value of the digital asset are limited" weighs against security classification. BCII's tokens are mathematically capped at the discount amount (e.g., a $50 discount token can never exceed $50), and the 11-month expiration enforces consumption rather than speculation.

Pillar 3 — SEC No-Action Letter Precedent: Two critical SEC no-action letters directly support BCII's position:

- TurnKey Jet (2019): The SEC's first-ever crypto no-action letter confirmed that tokens with immediate consumptive use on a fully operational platform avoid securities classification.

- Pocketful of Quarters (2019): Confirmed that transferable utility tokens with consumptive use and capped value are not securities.

Additionally, the gift card resale market precedent (CardCash, Raise, Cardpool processing billions annually without SEC registration) and the Supreme Court's Kirtsaeng v. John Wiley & Sons (2013) first-sale doctrine further validate that discount instruments can be freely resold.

The FASB Transformation: Old Rules vs. New Rules

This is the single most important table in understanding the entire Coupon Token thesis:

The asymmetry under the old rules was why no rational public company would hold tokens, the accounting was structurally punitive. The new FASB framework removes that barrier entirely, making the Coupon Token architecture viable for the first time.

Hypothetical Mid-Sized Company: The Full Financial Impact

The following is entirely hypothetical and illustrative, based on BCII's stated framework applied to a fictional Nasdaq-listed mid-cap consumer products company.

Baseline Company Profile:

- Shares outstanding: 100 million

- Stock price: $25.00

- Market capitalization: $2.5 billion

- Average product selling price: $500

- Token discount: 10% = $50 face value per token

Step 1: Platform Purchase

Step 2: Balance Sheet Impact (Year 1, 250 Million Tokens Held)

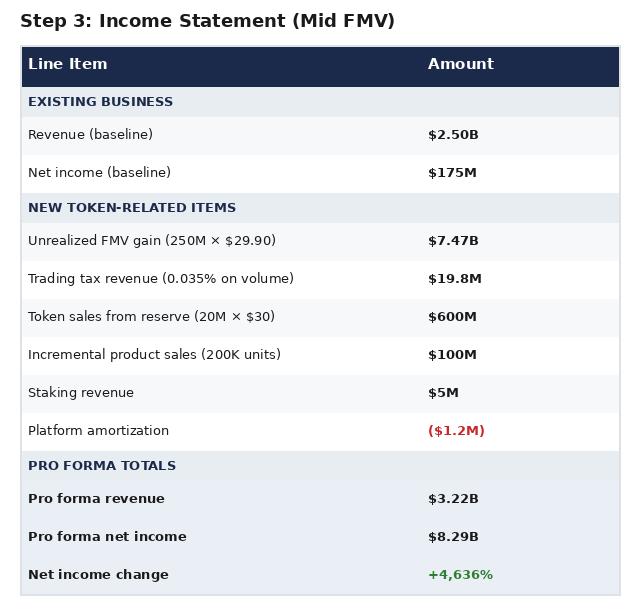

The key mechanic: tokens were acquired at a $0.10 cost basis but are marked to fair market value under FASB ASU 2023-08. The spread between $0.10 and $30 FMV — a 300x markup — flows entirely through net income into retained earnings, increasing shareholders' equity dollar-for-dollar because no offsetting liability is created. Tokens are discount instruments, not debt.

Step 3: Income Statement Impact (Year 1, Mid FMV Scenario)

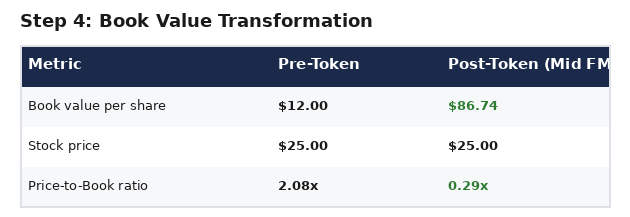

Step 4: Book Value Per Share Transformation

A stock trading at 0.29x book value after tokenization would appear massively undervalued by every fundamental metric. This creates immediate upward pressure on the stock price to re-rate toward historical P/B norms — which is precisely the equity revaluation thesis that drives the broader market impact.

The S&P 500 and Dow Jones: The Biggest Winners of All

Individual companies win by adopting the Coupon Token. Strong brands win disproportionately because their tokens trade at premium valuations. But the single biggest winners may be the market indices themselves, the S&P 500 and the Dow Jones Industrial Average.

Here's why.

The Index Math

The S&P 500 is weighted by market capitalization. The Dow Jones Industrial Average is weighted by share price. Both are driven by the aggregate financial performance and valuation of their constituent companies. When those constituents report dramatically higher total assets, total shareholder equity, net income, and book value per share, the index-level impact is not additive, it is multiplicative.

Consider a scenario where just 50 of the S&P 500's constituents adopt the Coupon Token architecture, major consumer brands like Apple, Nike, Amazon, Tesla, Walmart, Coca-Cola, McDonald's, Starbucks, Home Depot, and Procter & Gamble. Each reports balance sheet equity increases of 400% to 800% on their next quarterly filing. Book value per share explodes. Price-to-book ratios collapse below 1.0x, signaling extreme undervaluation. Institutional algorithms, value screens, and fundamental models all flash BUY simultaneously.

The stocks re-rate. Market caps expand. And because the S&P 500 is cap-weighted, those expanding market caps mechanically push the index higher, potentially by thousands of points in a compressed timeframe.

The Passive Investment Amplifier

Over 50% of all U.S. equity assets are now indexed, held in S&P 500 ETFs, Dow Jones trackers, total market funds, and target-date retirement portfolios. These funds don't choose which stocks to buy. They buy the index. When the index rises, they buy more. When they buy more, the index rises further.

The Coupon Token creates a reflexive loop: corporate adoption increases book value → stock prices re-rate upward → index levels rise → passive inflows increase → stock prices rise further → more companies adopt to capture the same effect → the cycle accelerates.

This is not a sector rotation or a momentum trade. It is a structural re-rating of the fundamental accounting basis of American public companies. Every 401(k), every pension fund, every sovereign wealth fund benchmarked to the S&P 500 or Dow Jones participates automatically. The retiree in Kansas with a Vanguard target-date fund benefits just as much as the hedge fund manager in Greenwich.

The Historical Comparison

No single accounting or regulatory change has ever simultaneously increased the reported equity of every consumer-facing public company by hundreds of percent. The closest analog might be the introduction of mark-to-market accounting for financial instruments in the 1990s, which contributed to the financial sector's explosive growth. But that applied to one sector. The Coupon Token applies to every company that sells a product or service — which is, effectively, every company in the S&P 500 and every company in the Dow.

If the average S&P 500 constituent sees even a 200% increase in reported book value, and the market re-rates those stocks to historical P/B averages, the index implications are staggering.

The Naked Short Killer: Why the Reddit Crowd Will Come Running

The Overstock/tZERO precedent proved the concept. When Overstock announced a blockchain-based digital dividend in 2020, short sellers were contractually obligated to deliver both the stock and the digital token, but because the token could only be traded on Overstock's own platform, shorts literally could not obtain it. Overstock's stock nearly doubled as shorts scrambled to cover.

BCII's Coupon Token takes this further. It isn't a one-time event, it's five distributions over 55 months, each requiring shareholders to present verified shares to the transfer agent. Every distribution cycle is a new reckoning for short sellers. If naked shorts have created synthetic shares that outnumber the actual float, those phantom shares cannot produce corresponding tokens, forcing sequential short squeezes across the entire distribution schedule.

For the Reddit retail army, the same community that turned GameStop, AMC, and Bed Bath & Beyond into cultural phenomena, this is catnip. It's not just a meme play. It's a structurally engineered, repeating, blockchain-verified short squeeze mechanism embedded in the corporate action calendar of every company that adopts it. The Reddit crowd doesn't just want to beat the shorts, they want a system that makes beating the shorts inevitable. The Coupon Token is that system.

Strategy vs. Coupon Token: The Balance Sheet Comparison That Changes Everything

The market has already seen what happens when a public company weaponizes its balance sheet around a digital asset. Strategy (formerly MicroStrategy) spent $21 billion across seven securities offerings to accumulate approximately 641,000 Bitcoin, transforming itself from a business intelligence company into a leveraged Bitcoin vehicle.

The results have been mixed. Strategy's stock trades approximately 68% below its highs, exhibits 2–3x Bitcoin's volatility, and faces structural challenges including massive dilution and a narrative that has stretched to breaking. The core problem: Strategy had to spend real money, billions of dollars raised by diluting shareholders, to buy an external asset (BTC) that it does not control, cannot cap, and generates no revenue.

BCII's Coupon Token model inverts every element of that equation:

The contrast is stark. Strategy paid billions for an uncontrollable external asset. Coupon Token unlocks an asset that was always there, the future discount value of a company's own products, and places it on the balance sheet at fair market value for a de minimis cost, without issuing a single share of dilutive equity.

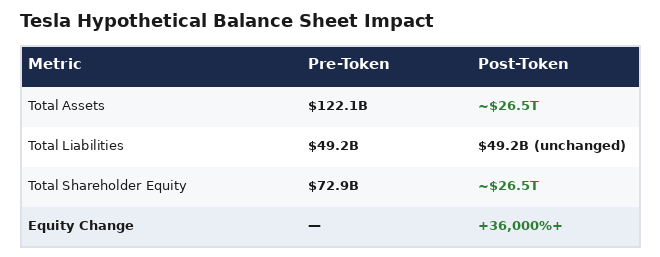

The Hypothetical Tesla Coupon Token: What the Numbers Look Like at Scale

Tesla Baseline (FY2024):

- Total assets: $122.1B

- Total shareholder equity: $72.9B

- Shares outstanding: 3.217 billion

- Average vehicle selling price: ~$66,000

- Token face value (10% discount): $6,600

Platform Purchase:

- 60 million tokens paid to BCII at $0.10 = $6,000,000 capitalized cost

- Amortized over 5 years at $1,200,000/year

Hypothetical Balance Sheet Impact (Moderate Scenario: 8B tokens held at $3,300 FMV):

As the JD Unfiltered article states: "For Tesla, 15 billion tokens at $6,600 each equate to a $99 trillion balance-sheet asset. That kind of scale is theoretical, but the rules now permit tokens to be treated as cash-like holdings that strengthen equity and liquidity."

The token also creates multiple new revenue streams for Tesla: a 2.5% in-kind trade tax on every secondary-market TCT transaction, token sales from reserve, FSD subscription uplift from token-incentivized buyers ($8,000/year), and staking revenue, all of which are pure incremental cash and income.

Now multiply the Tesla example across the Dow's 30 constituents, or the S&P 500's top 50 consumer brands. The aggregate index impact becomes the defining financial story of the decade.

BCII Enterprises: The Pro Forma Winner

At the center of this convergence sits BCII Enterprises Inc., the micro-cap OTC company that filed the patent on the invention. Every corporation that tokenizes its future sales discounts will need to license BCII's architecture or risk infringement.

BCII receives 60 million tokens (20%) per corporate implementation, carried on its own balance sheet at fair market value under the same FASB rules. With a pro forma model projecting 9 corporate clients in Year 1:

- 540 million tokens held (60M × 9 clients)

- Fair market value of token holdings at scale: $50M–$150M+

- Recurring revenue from SaaS fees, implementation charges, and token trading

- Pro forma net income: ~$41.7M in Year 1

BCII doesn't just license the technology it becomes a direct, leveraged beneficiary of every single corporate adoption. Each new client adds 60 million tokens to BCII's balance sheet at fair market value, creating a compounding flywheel where BCII's own equity grows with every deal signed.

The Domino Theory: Why One Company Forces All Companies

Once a single major Nasdaq or NYSE company adopts the Coupon Token architecture and reports its next quarterly earnings, the financial world will see something unprecedented: a hundreds-of-percent increase in total shareholder equity and total assets originating from a $6 million platform purchase.

Analysts will re-rate the stock. The price-to-book ratio will collapse to a fraction, signaling massive undervaluation. Shareholders of competing companies will immediately demand: "Why aren't we doing this?"

And the answer will be: there is no reason not to. The FASB rules are in place. The SEC-CFTC framework is published. The no-action letter precedents exist. The technology partner is signed. The accounting opinion is rendered. The patent is filed. The only cost is $6 million and a 5-year amortization.

Every consumer-facing public company, retailers, automakers, airlines, subscription services, consumer electronics, pharmaceutical companies, food and beverage conglomerates, possesses the same hidden prepaid asset: the future discount value of their own products and services. The Coupon Token simply gives that asset a blockchain wrapper, a secondary market, and FASB-compliant fair value recognition.

When the first domino falls, the cascade will be rapid. Boards of directors will face fiduciary pressure. Institutional investors will demand adoption. Retail shareholders, armed with Reddit, social media, and the promise of 50% token distributions plus naked short destruction, will make it a governance issue at every annual meeting.

The companies with the strongest brands, the Apples, the Nikes, the Coca-Colas, the Teslas, will move first, because their tokens are worth the most. Their competitors will follow within quarters. And as adoption spreads across the S&P 500 and the Dow Jones, the indices themselves will undergo a structural re-rating that makes every prior bull market look like a warmup act.

The tokenization of a future sales discount is not a theory. It is a patent-pending, FASB-compliant, SEC-clarified, technology-deployed, accounting-opined invention waiting for its first Fortune 500 adopter. When that happens, the hidden marketplace accelerant ignites, and every public company balance sheet in America, every major stock index, and every retirement account benchmarked to those indices will never look the same.

The winners: BCII Enterprises Inc., the company that saw the hidden asset, built the architecture, filed the patent, and positioned itself to collect 60 million tokens from every corporation that follows. The iconic American brands whose name recognition makes their tokens the most valuable on earth. And the S&P 500 and Dow Jones Industrial Average, the indices that will channel the aggregate force of corporate tokenization into the greatest equity re-rating in market history.

DISCLAIMER: This article is for informational and analytical purposes only. All financial projections involving specific companies (including Tesla) are entirely hypothetical illustrations of the Coupon Token framework mechanics and do not constitute investment advice, earnings forecasts, or recommendations to buy or sell any security. BCII Enterprises Inc. trades on the OTC Markets (OTCID: BCII). Investors should conduct their own due diligence and consult qualified financial advisors before making investment decisions.