The Hidden Bull Case: How Defanging Iran Locks In a Trillion-Dollar US Economic Advantage the Market Is Missing

By April 2026, the conventional narrative on the Iran war is dead wrong. Wall Street is pricing this conflict as a risk event — higher oil, inflation fears, consumer drag, recession odds ticking up. But beneath the headline anxiety, the United States is quietly assembling the most dominant structural economic advantage since the post-WWII Bretton Woods order. Every missile that degrades Iranian infrastructure, every day the Strait of Hormuz stays constricted, and every month Qatar's shattered LNG trains sit idle widens a competitive moat around the US economy that will persist for five years or more — across energy, petrochemicals, and the explosive growth category of AI-powered digital services.

The stock market hasn't figured this out yet. When it does, expect a violent repricing upward in US equities and a surge in the dollar.

The Oil Shock That Isn't (For America)

The traditional playbook says oil shocks are a tax on consumers. They are — for everyone except the United States. The US produces approximately 13.6 million barrels per day and became a net energy exporter in 2019. More critically, the fuel that powers the US electricity grid and its fastest-growing export industries, natural gas, trades at Henry Hub for roughly $2.89–$3.76/mcf. It has barely moved since the conflict began.

Compare that to Europe's TTF benchmark, which spiked 60% in March alone to approximately €50/MWh — the equivalent of $15–17/mcf. Asian JKM spot prices are even higher, with price-sensitive buyers in South and Southeast Asia effectively priced out of the market entirely. The ratio of European-to-American gas prices is now running at 5:1 to 6:1 — and it's locked in structurally, not cyclically.

Why? Because the supply destruction is physical, not financial.

Qatar: The Supply Shock No One Can Fix Quickly

Iran's retaliatory strikes on Qatar's Ras Laffan facility, the crown jewel of global LNG infrastructure, knocked out 12.8 million tonnes per year of capacity, roughly 17% of Qatar's total exports. QatarEnergy has declared force majeure on long-term contracts with Italy, Belgium, South Korea, and China for three to five years. Cryogenic LNG trains are among the most complex engineered systems on earth. You cannot fast-track their repair.

Qatar was the world's second-largest LNG exporter after the United States, responsible for approximately 20% of global LNG supply. That supply is now offline for the better part of this decade. Europe, which pivoted to LNG dependence after Russia cut pipeline gas during the Ukraine war, is now fighting with Japan, South Korea, and China over a structurally smaller global LNG pie. The only scalable replacement supplier on the planet is the United States.

Iran: A Regime Running Out of Days, Not Months

The systematic destruction of Iranian infrastructure is accelerating on multiple fronts simultaneously:

- Oil: Israel and US strikes have hit Kharg Island, Iran's primary crude export terminal.

- Petrochemicals and Steel: Israeli strikes have destroyed major industrial complexes that formed the backbone of Iran's non-oil economy.

- Electricity: US targeting of power generation infrastructure is collapsing Iran's ability to maintain water treatment, food refrigeration, hospitals, and basic civilian logistics.

- Food: Iran imports 60–70% of its grain. With Bandar Imam Khomeini effectively blockaded and over 20 grain vessels unable to discharge, staple food prices in Tehran have more than doubled.

Without electricity, without grain, without export revenue, and without the ability to manufacture steel or refine petrochemicals, Iran faces systemic societal collapse within weeks. The regime's options have narrowed to capitulation or chaos. Either outcome produces the same result for the US: a permanently defanged Iran and a Persian Gulf whose energy infrastructure will take half a decade to rebuild.

The Insight Wall Street Is Missing: AI as Embedded Energy Export

Here is where the analysis departs from anything the market is currently pricing.

The United States doesn't just export energy as molecules on tankers. Increasingly, it exports energy as intelligence — embedded in AI compute services sold globally by Microsoft, Google, Amazon, Meta, and the entire US cloud ecosystem. Every AI inference query, every enterprise AI deployment, every autonomous system trained in a US data center consumes cheap American natural gas converted to electricity at roughly $20–25/MWh.

A European hyperscaler attempting to compete runs on electricity generated from imported LNG at $80–120/MWh. An Asian competitor faces the same or worse. The NUS Singapore analysis confirms that the Iran war "could adversely impact AI infrastructure growth in India and across Asia by driving up energy costs for data center operations."

This creates a self-reinforcing flywheel:

- Middle East infrastructure destruction keeps global gas prices elevated while US domestic gas stays cheap.

- Cheap US gas means cheap US electricity means cheap US compute.

- Cheap US compute means the US dominates global AI services — the highest-value-added export category in the modern economy.

- Revenue flows back as digital services exports at software margins — no tankers, no Strait of Hormuz transit, no force majeure risk.

- Gulf data center projects are abandoned or redirected to US soil, further concentrating AI capacity domestically.

The hundreds of thousands of Nvidia Blackwell GPUs originally destined for Saudi and UAE data centers are being repatriated to American facilities. The chips still exist. The demand still exists. The only thing that's changed is where the compute happens — and that "where" is overwhelmingly the United States, running on $2.89 gas while the rest of the world pays $17.

This is not an energy trade. It is a knowledge trade. The US is running its cheapest, most abundant, most geopolitically insulated energy source through a "knowledge refinery" — the data center — and exporting the refined product at margins that would make OPEC weep. And unlike LNG contracts, AI services scale without new physical infrastructure at the point of delivery.

The Competitive Damage to China and Europe Is Compounding Daily

Every day the conflict persists, America's principal economic competitors absorb disproportionate damage:

- China receives approximately 50% of its crude oil through the Strait of Hormuz. Its manufacturing base, already under tariff pressure, now faces an energy cost shock that the US does not share.

- Europe is reliving its worst energy nightmare. Having barely survived the Russia gas cutoff, it now faces the loss of its second-largest LNG supplier for years. Industrial competitiveness in Germany, Italy, and France — already deteriorating — will erode further as energy-intensive manufacturing becomes untenable at current gas prices.

- India and Southeast Asia, the supposed next wave of global growth, are being priced out of LNG markets entirely, stalling data center buildouts and industrial expansion.

- South Korea and Japan, critical semiconductor manufacturing hubs, face soaring energy costs that raise the price of every chip fabricated on their soil.

UNCTAD projects global trade growth collapsing from 4.7% to 1.5–2.5%. But that pain is distributed asymmetrically — and the US sits on the right side of every asymmetry.

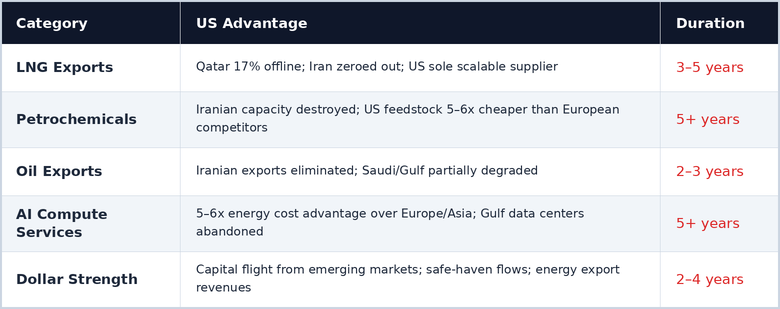

The Five-Year Advantage: Quantified

The Market Implications: A Repricing Is Coming

The S&P 500 is trading as if the Iran conflict is a net negative for the United States. It is not. When the market recalibrates to the structural reality — that the US has locked in a half-decade energy and AI compute advantage over every major economic rival — expect:

- A massive US equity rally, led by energy producers (Cheniere, EQT, Venture Global), petrochemical manufacturers (Dow, LyondellBasell), AI infrastructure plays (Nvidia, Microsoft, Google, Amazon), and US-based data center REITs.

- Significant dollar strengthening, driven by energy export revenues, safe-haven capital flows, and the realization that the US current account is improving structurally as digital services exports compound on top of physical energy exports.

- Relative underperformance in European, Chinese, and emerging market equities as the energy cost differential grinds down industrial competitiveness abroad.

The conventional wisdom says wars are bad for markets. This war is bad for other countries' markets. For the United States — a nation that is simultaneously the world's largest energy producer, the world's dominant AI platform, and the one major economy whose primary fuel source is completely insulated from Middle East disruption — this conflict is converting a temporary geopolitical crisis into a permanent structural economic advantage.

The market is looking at the smoke. It should be looking at what's underneath: the most favorable competitive realignment for the American economy in a generation. Time is on America's side. The repricing will not be gradual.

The views expressed in this article represent an independent economic analysis of US structural competitive positioning in the context of the ongoing Iran conflict. Investors should conduct their own due diligence and consider all risks, including the potential for financial contagion, supply chain disruptions, and escalatory scenarios that could alter the calculus described herein.